Introduction

Hydrogen has been dubbed the “Swiss army knife” of clean energy, given its potential to become a tool to cut emissions in key sectors, as well as to assert U.S. global energy leadership and increase our nation’s competitive edge. Given its unique attributes, it has the potential to greatly reduce emissions in hard-to-decarbonize industrial applications such as steelmaking, cement manufacturing, trucking and aviation. It may also be appropriate in certain cases as a means to promote grid balance via power generation and energy storage. According to the U.S. Department of Energy (DOE), switching to low-emissions or clean hydrogen in hard-to-abate[1] sectors could reduce global energy-related CO2 emissions by 10 to 25 percent, and U.S. CO2 emissions by up to 10 percent from 2005 levels by 2050.[2] Many countries across the world have recognized hydrogen’s potential, and at least 39 countries have adopted explicit national hydrogen strategies.[3]

By 2050, the global demand for clean hydrogen is projected to account for somewhere between 73 and 100 percent of total hydrogen demand, from less than 1 percent today.[4] The United States has a natural advantage for hydrogen production because of the ample availability of feedstocks, storage and adaptable natural gas supply infrastructure. As such, the U.S. has the potential to become a global leader in the space.[5] Currently, however, penetration of clean hydrogen in industrial, transportation and power generation sectors faces obstacles such as high costs, transportation challenges and lack of infrastructure. Recent legislation has provided substantial incentives for the development of hydrogen technologies and infrastructure, but challenges to successful scaling remain. One avenue being explored is to address these challenges is to increase demand-side policy support to ensure the uptake of clean hydrogen.

As other countries rapidly ramp up investment in hydrogen, ensuring an effective implementation of recently approved incentives and filling in any remaining policy gaps will be crucial in capitalizing on the opportunity hydrogen presents for our nation’s global competitiveness and decarbonization objectives.

Applications and opportunities

Background

Hydrogen has the potential to unlock an abundance of clean energy solutions. It is considered a clean-burning fuel because when consumed in a fuel cell, it emits only water and not other emissions generally associated with industrial activities, including greenhouse gases. Because hydrogen is generally not found free-floating in nature, it needs to be separated from other elements to be used as a fuel source.

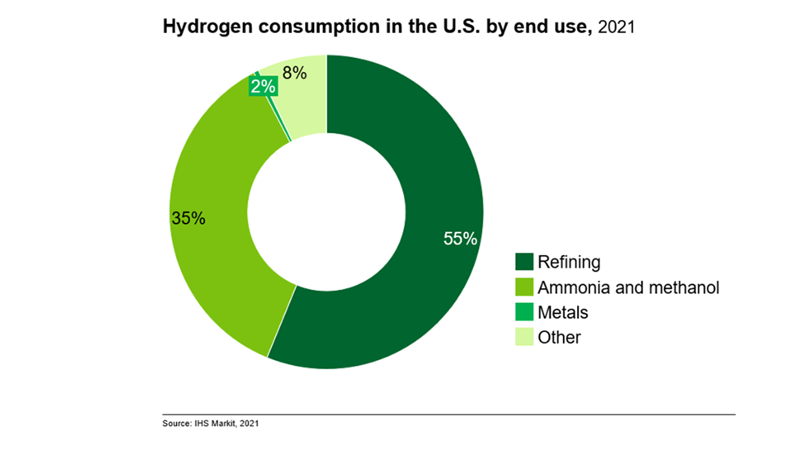

Currently, hydrogen consumption in the U.S. is driven by heavy industry – primarily the production of ammonia (the main building block for agricultural fertilizers), methanol and oil refining (see Figure 1).[6] Switching to the use of clean hydrogen in these sectors – which can be defined as hydrogen produced through a method with zero- to low- emissions – can greatly reduce their emissions. Methods of production for clean hydrogen can involve electrolysis from low-emissions electricity, fossil fuels paired with carbon capture, utilization and storage (CCUS), methane pyrolysis, or it can be extracted from natural deposits of hydrogen in the subsurface of the earth, known as geologic hydrogen.

Figure 1. Consumption of hydrogen in the U.S. by end-use, 2021.

Source: IHS Markit, 2021, cited in Department of Energy (DOE), DOE National clean hydrogen strategy and roadmap, p. 14, https://www.hydrogen.energy.gov/docs/hydrogenprogramlibraries/pdfs/us-national-clean-hydrogen-strategy-roadmap.pdf?sfvrsn=c425b44f_5.

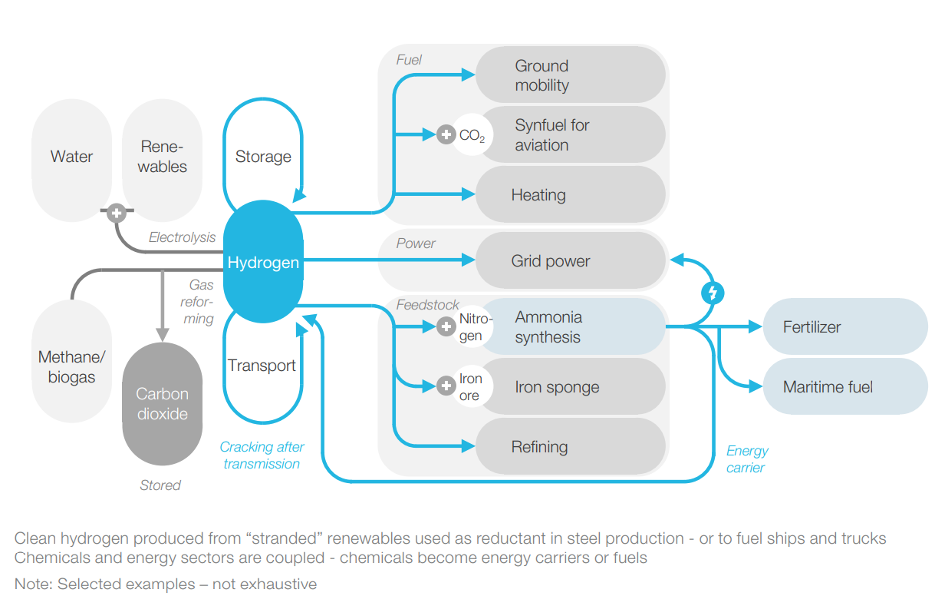

Hydrogen holds promise for reducing emissions in a variety of other sectors as well, with possible applications for transportation (fuel cell cars, trucks and aircraft), homes and buildings (heating), long-duration storage and electricity generation. It also has the potential to decarbonize high-emitting sectors of industry such as steel, aluminum and cement production (see Figure 2).

Figure 2. Hydrogen pathways in the energy system. Iron sponge, also called Direct Reduced Iron (DRI), can be used as a substitute for metal scrap in Electric Arc Furnaces for steel manufacturing.

Source: Hydrogen Council and McKinsey & Company, Hydrogen for Neto-Zero: A critical cost-competitive energy sector, November 2021, p. 15, https://hydrogencouncil.com/wp-content/uploads/2021/11/Hydrogen-for-Net-Zero.pdf.

Expanding the use of clean hydrogen in industry and energy production can serve energy security and economic development. This is because the United States possesses abundant and diverse domestic feedstocks for the production of clean hydrogen – wind, solar, geothermal, nuclear, hydropower and natural gas – as well as storage formations and adaptable energy infrastructure. As a resource that is not dependent on a single technology and has the potential to be stored in large amounts for long periods of time, hydrogen may also eventually be a useful fuel for grid reliability and general flexibility in the energy sector.

It is worth nothing that hydrogen as a decarbonization tool enjoys substantial public support. A 2022 Breakthrough Energy poll found that 75 percent of voters were in favor of the use of clean hydrogen to reduce carbon pollution in industry.[7]

Emissions reductions potential for hard-to-decarbonize sectors

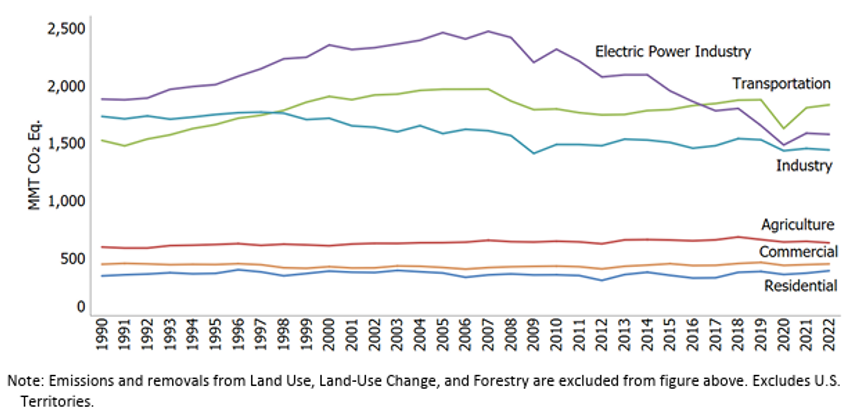

Industry was the third largest source of emissions in the U.S. in 2022, after transportation and power generation (see Figure 3), with over half of industrial emissions coming from the direct combustion of fossil fuels to produce heat.[8] When electricity-related emissions are distributed to economic sectors, however, industry has ranked first and is now essentially tied with transportation.[9]

Figure 3. U.S. Greenhouse gas emissions by economic sector.

Source: U.S. Environmental Protection Agency (EPA), Draft inventory of U.S. greenhouse gas emissions and sinks (1990-2022), p. 124, https://www.epa.gov/system/files/documents/2024-02/us-ghg-inventory-2024-main-text.pdf.

According to DOE, if clean hydrogen becomes widely adopted in sectors where there are few other avenues to decarbonize, such as iron and steel, long-haul trucking, chemicals, refining and maritime and aviation fuels, it could help reduce global energy-related emissions by 10 to 25 percent.[10] If adopted in sectors such as heating for buildings, cement, buses and short-haul trucks, and other industries such as construction, agriculture, forestry, fishing, manufacturing and mining, where hydrogen is one of the avenues for decarbonization, DOE states that hydrogen could help reduce global emissions by up to 25 to 40 percent.[11] In the U.S., switching to clean hydrogen could reduce domestic CO2 emissions by up to 10 percent from 2005 levels by 2050.[12] The combustion of a 30 percent blend of hydrogen by volume for the production of high-temperature heat in industrial processes, for example, can reduce GHG emissions in combustion turbines by around 10 percent.[13] However, adoption of clean hydrogen in these sectors will depend largely on the development of a stable and affordable supply.

The more immediate emissions reductions from switching to clean hydrogen would likely occur in heavy-duty transportation and industrial sectors, where hydrogen is already a primary feedstock and there are no alternatives, such as ammonia, methanol, oil refining and fuels.[14] In fact, according to recent DOE scenario analyses, transportation, industrial and chemical sectors will likely make up over 90 percent of demand for hydrogen by 2050, with transportation being a key inflection point to drive up national demand.[15] The deeper emissions reductions opportunities can come from sectors in which hydrogen is not already a primary feedstock, and in which few alternatives exist – including as a direct transportation fuel in heavy-duty trucking or aviation, as a feedstock for the production of drop-in Sustainable Aviation Fuel (SAF), or as fuel in industrial processes such as cement, steel and aluminum production.[16]

Steel and aluminum

The U.S. steel sector is the most energy-efficient in the world among steel-producing nations,[17] largely because 70 percent of U.S. steel is made via an Electric Arc Furnace (EAF) process, which recycles scrap steel and direct-reduced iron (DRI).[18] The rest is produced via a Blast Furnace – Basic Oxygen Furnace (BF-BOF), which requires a lot of coal and coke,[19] and is also the predominant production method in most other countries. In China, for example, more than 90 percent of steel is produced via BF-BOF.[20] Steel and aluminum production involve processes that require high temperatures of around 1,800° F,[21] typically achieved by burning fossil fuels. Natural gas is the largest source of energy in U.S. steelmaking, at 37 percent; while coal is the dominant fuel used in many other nations.[22]

Steelmaking is responsible for around 2.1 percent of U.S. CO2 emissions,[23] but the global steelmaking industry accounts for over 7 percent of global greenhouse gas emissions.[24] More than half of the world’s steel is made in China,[25] where coal accounts for 63 percent of electricity generation.[26] China exports 6.6 percent of its steel, mostly to Asian markets – predominantly South Korea, Vietnam, Philippines, and Thailand.[27] It imports only 1.8 percent of the steel it consumes, mostly from Japan, Indonesia, and South Korea.[28] The U.S. exports 10.1 percent of the steel it produces – mostly to Canada, Mexico and the Dominican Republic[29] – and imports around 26.2 percent of the steel it consumes.[30] In 2022, U.S. steel imports mainly originated from Canada, Mexico, South Korea, Brazil and Japan.[31]

In steelmaking, hydrogen can be used both for heat and as a chemical catalyst.[32] According to DOE, using clean hydrogen as a reductant to refine iron ore, to replace coke or natural gas, could reduce the lifecycle emissions of primary steelmaking by 40-70 percent.[33]

Hydrogen can also be used to generate high heat for the production of aluminum, which is responsible for 2 percent of global greenhouse gas emissions.[34] Global demand for aluminum is expected to increase by up to 80 percent by 2050.[35] The smelting of recycled scrap metal accounted for 78 percent of U.S. aluminum production in 2021, with the rest coming from primary smelting.[36] Secondary production is 95 percent less energy-intensive than primary production.[37] According to the World Economic Forum (WEF), increasing the use of low-carbon power – from sources such as hydrogen – in electric furnaces could eliminate up to 62 percent of emissions from global aluminum production.[38]

While currently, most projects involving low-emissions steel or DRI production with hydrogen are based outside the U.S.,[39] some American iron and steel facilities are being designed to be hydrogen-ready once hydrogen is available on a commercial scale.[40] In January 2024, for example, Cleveland Cliffs successfully completed a test to use hydrogen as a reductant and fuel source at its Indiana Harbor #7 facility, the largest blast furnace in North America.[41] If the U.S. is to demonstrate leadership in lower emissions steel and aluminum production, shepherding a healthy hydrogen economy will be a key piece of the puzzle.

Chemicals: ammonia and methanol

Large-scale deployment of clean hydrogen is expected to start with sectors such as ammonia, methanol and petrochemicals, which enjoy established supply chains and economies of scale.[42] Ammonia and methanol are two of the most-produced commodity chemicals in the world and account for most of the greenhouse gas emissions from chemicals.[43] Ammonia alone is responsible for 1.3 percent of global greenhouse gas emissions.[44] They both rely on natural gas or coal, and according to DOE, could be decarbonized by over 90 percent if they switch over to hydrogen.[45]

China is the world’s leading ammonia producer, accounting for 30 percent of global production, with 85 percent of this relying on coal.[46] Around 70 percent of ammonia is used to produce fertilizers, with the remainder utilized in industrial applications such as plastics, explosives, and synthetic fibers.[47]

Transportation

Hydrogen offers high promise for emissions reductions in transportation, which is one of the most difficult-to-decarbonize sectors and is now the largest source of greenhouse gas emissions in the United States. It offers the possibility of long driving ranges, fast fueling, and high payload capacities.[48] For these reasons, the greatest decarbonization potential for hydrogen lies with long-haul trucking, as opposed to passenger vehicles, where other technologies are becoming more established. Hydrogen can also be a feedstock for the production of liquid fuels that can help decarbonize aviation, rail and marine transportation.[49] While transportation is one of the most promising avenues for the use of hydrogen in decarbonization efforts, it still faces challenges such as a very incipient refueling and distribution infrastructure network.

Cement

According to DOE, in cement production, if carbon capture and sequestration is used to capture process-related emissions and clean hydrogen were used as fuel for the kiln, emissions of clinker production could be brought down nearly to zero,[50] although some technical challenges related to hydrogen combustion would need to be resolved.

Power generation

There is potential for hydrogen to be used, either blended with natural gas or in its pure form, in gas turbines. This would probably occur on a longer time horizon – most likely after 2040, according to DOE (at least for efforts at scale, see Figure 10 below in “Challenges” section), largely due to necessary retrofits to pipelines and other infrastructure, and cost.[51] There are current R&D efforts to address technical barriers to hydrogen blending, such as HyBlend at DOE,[52] led by the National Renewable Energy Laboratory (NREL).

Energy stored as hydrogen

Hydrogen also enjoys the advantage of its ability to be stored and processed in similar ways to oil and natural gas, which will be key for production at scale.[53] It can be stored in tanks as a compressed gas or as a liquid, or at large-scale volumes in geologic formations such as salt caverns. In addition to salt caverns, other geologies such as hard rock caverns or depleted oil and gas reservoirs and aquifers could serve as hydrogen storage sites.[54]

There are currently four underground hydrogen storage caverns in development or in use in the United States – three of them on the Gulf Coast.[55] This includes the world’s largest hydrogen storage cavern in Beaumont, Texas, with an estimated storage capacity equivalent to 278 GWh if the hydrogen were used to generate electricity.[56] In Delta, Utah, the Advanced Clean Energy Storage Project (ACES Delta), which has secured a $500 million loan guarantee from DOE’s Loan Programs Office (LPO),[57] is slated to be the country’s largest hydrogen storage hub with an initial estimated capacity of 300 GWh in two salt caverns.[58]

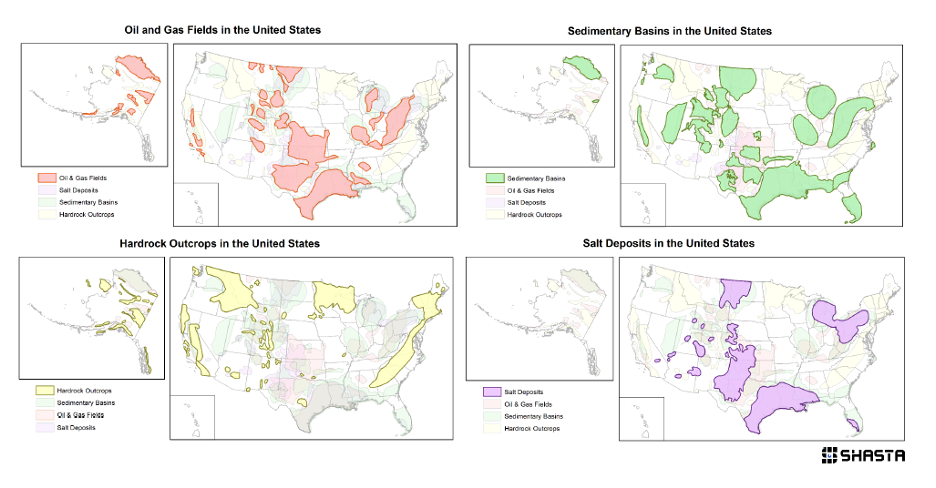

U.S. geology offers the potential to greatly expand underground storage capacity (see Figure 4). According to a 2023 study, the already existing underground gas storage facilities in the U.S. could store up to 327 TWh of pure hydrogen.[59] Another 2023 study of hundreds of salt domes in Texas, Louisiana, Mississippi and the Gulf of Mexico found these domes could have a total energy storage potential of 368 TWh.[60] For scale, the state of New York consumed approximately 226 TWh of electricity in 2021.[61]

Figure 4. Underground storage opportunities in the U.S.

Source: “Clean Hydrogen Hubs and Geologic Storage Images,” Subsurface Hydrogen Assessment, Storage and Technology Acceleration (SHASTA), Images – SHASTA (doe.gov), cited in DOE, DOE National clean hydrogen strategy and roadmap, p. 53.

Refining

Hydrogen is already a crucial input for petroleum refining, primarily to crack heavy crude and desulfurize product streams. According to DOE, introducing clean hydrogen at existing refineries can reduce the lifecycle emissions of the refining process by up to 12 percent.[62]

Jobs

According to DOE, hydrogen production has the potential to create around 100,000 new direct and indirect jobs by 2030.[63] Direct jobs include fields such as engineering and construction, while indirect jobs would be in manufacturing and the supply of raw materials. An additional 120,000 jobs could derive from the operation and maintenance of hydrogen assets.[64]

Many skills from the fossil fuels sector, whose workforce has ample experience in safely transporting gases over long distances, are highly transferable to the hydrogen sector, although facilitating this transition will require training programs.[65] Many professions employed in various sectors of the energy economy today, such as civil and electrical engineers or legal and regulatory roles, will indeed be key to supporting the growth of a hydrogen industry.[66]

The hydrogen and fuel-cell vehicles sector, though small, has already seen one of the fastest employment growth rates among clean energy subsectors, providing employment for nearly 18,000 Americans in 2022 – a 25 percent increase from 2021.[67] For comparison, clean energy jobs grew by 3.9 percent nation-wide, and overall U.S. employment grew by 3.1 percent in the same time period.[68]

Hydrogen production

While there are known geologic reservoirs of hydrogen – often called “white hydrogen,” which has garnered much interest in the past year,[69] no geologic extraction is currently occurring. Hydrogen is rarely found naturally on Earth in its elemental form, so it usually must be produced by separating hydrogen (H2) from other molecules such as water (H2O) or methane (CH4).

In 2022, global hydrogen production reached nearly 95 million metric tons (MMT) – up 3 percent from 2021. Natural gas-based production is currently responsible for 62 percent of global hydrogen production, and coal gasification for 21 percent, with most of the latter located in China.[70] Low-emissions hydrogen accounts for less than 1 percent of global production.[71] In 2021, the U.S. produced 11.4 MMT of hydrogen, or just over 15 percent of global production, mostly via SMR.[72] As of 2021, there were 257 hydrogen production facilities nationwide, and 25 hydrogen pipelines spanning around 1,600 miles.[73] Our nation’s hydrogen-producing capacity, however, is exponentially higher. According to the National Renewable Energy Laboratory (NREL), the U.S. could produce up to 1B metric tons of clean hydrogen annually, just from renewable resources such as wind, solar, and biomass.[74] Given this potential, and the fact that it is a resource that pairs well with our existing industrial infrastructure and workforce capabilities, hydrogen is one of the most promising pathways towards boosting America’s competitiveness on the global stage.

While the current amount of clean hydrogen produced in the U.S. is small and limited mostly to small-scale pilot projects,[75] the Biden Administration’s National Clean Hydrogen Strategy and Roadmap sets a target of increasing U.S. clean hydrogen production to 10 MMT by 2030 and 50 MMT by 2050 to achieve a 10 percent reduction in domestic greenhouse gas emissions.[76]

Hydrogen gas can be produced in a number of ways, including:

- Steam methane reforming (SMR), whereby methane (CH4) is put under high-pressure conditions with a catalyst to produce hydrogen (H2), carbon monoxide (CO) and carbon dioxide (CO2).[77] It is currently the most established technology for hydrogen production. It is often called “gray hydrogen” and can be accompanied by carbon capture to reduce emissions from the process (“blue hydrogen”; see annex for a more complete list of methods of production and categorization by “colors”). It is less energy-intensive than electrolysis. Only around 0.6 percent of global fossil-based production is coupled with carbon capture and storage -CCS- (“blue hydrogen”).[78] In the U.S., 95 percent of hydrogen is produced via SMR.[79]

- Methane pyrolysis, also called “turquoise hydrogen,” is a process through which methane (CH4) is heated until it breaks into solid carbon (C) and hydrogen (H2). It is less energy-intensive than electrolysis and SMR,[80] and it has the advantage of producing no CO2 emissions. Its solid carbon by-product may be a commercial commodity.[81] Pyrolysis technologies are less mature than SMR ones, however, and production costs are slightly higher.[82]

- Electrolysis is a process through which water is split into hydrogen and oxygen using electricity.[83] The amount of emissions associated with this method of production will depend on the source of energy utilized, which could be wind, solar, nuclear or fossil fuels. Any method that uses renewable sources or waste streams is termed “green hydrogen,” while nuclear-powered production is often called “pink hydrogen.” Only about 1 percent of global hydrogen production[84] and less than 1 percent of domestic production is via electrolysis.[85] Different electrolyzer technologies are at different degrees of maturity. Some, such as Alkaline Water Hydrolysis (AWH, the most established) and Proton Exchange Membranes (also called Polymer Electrolyte Membranes, PEM), have reached the commercial stage, while others such as Solid Oxide Electrolysis Cells (SOEC) are still in laboratory stages.[86]

- Gasification of coal is referred to as “brown/black hydrogen.” Currently, around 21 percent of global hydrogen production uses this method.[87] It can also be accompanied by carbon capture to reduce its associated emissions.

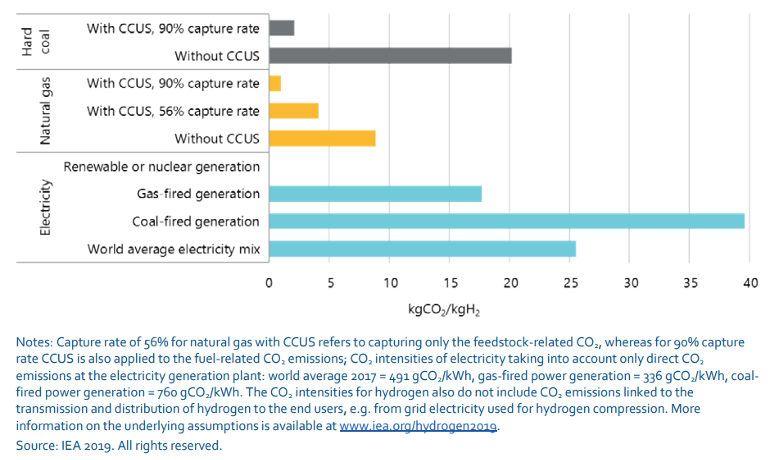

These processes all require energy created by the consumption of a fuel or a renewable resource of electricity. Each resource results in hydrogen with a different carbon footprint. The carbon intensity of hydrogen produced directly from natural gas is roughly half of that produced from coal (see Figure 5). Applying CCS to either method, however, reduces emissions significantly. The emissions of hydrogen production through electrolysis depends on the emissions associated with the type of electricity generation used. Depending on the regional electricity mix, the carbon footprint of electrolysis production can vary widely.

Figure 5. CO2 emissions by method of hydrogen production.

Source: International Energy Agency (IEA), The future of hydrogen: Seizing today’s opportunities, June 2019, p. 53, https://iea.blob.core.windows.net/assets/9e3a3493-b9a6-4b7d-b499-7ca48e357561/The_Future_of_Hydrogen.pdf.

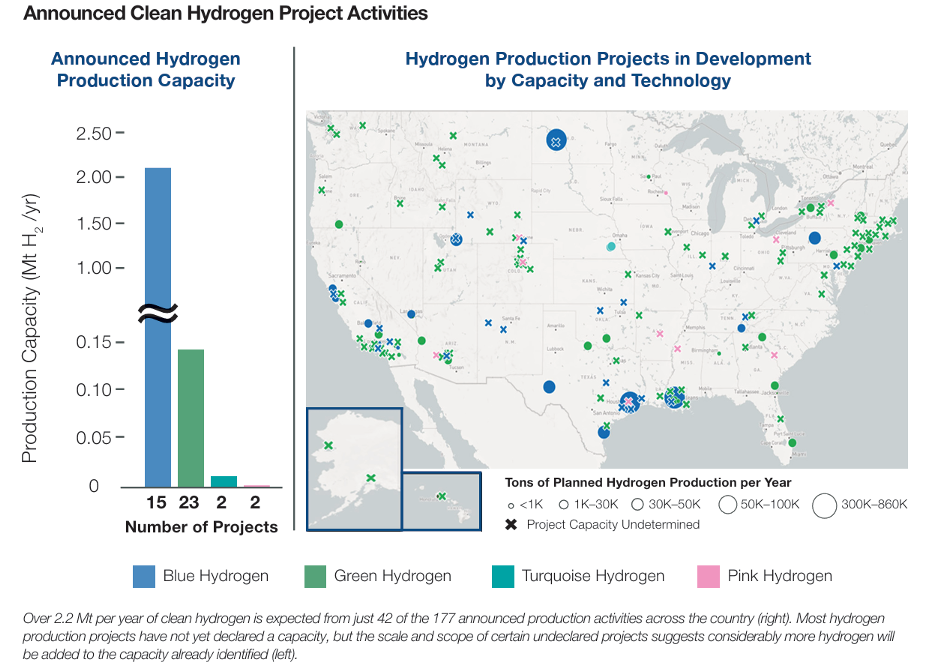

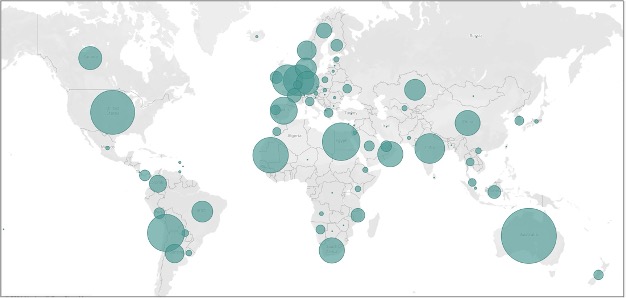

Of recent clean hydrogen project announcements in the U.S., around 70 percent are relatively small-scale renewable-energy based electrolysis projects, and around 20 percent are fossil-based with CCS, although the latter account for nearly 95% of the announced production capacity (see Figure 6).[88] The International Energy Agency’s (IEA) hydrogen projects database lists nearly 1,500 clean hydrogen projects under development globally; 118 of them in the United States (see Figure 7 for global distribution of hydrogen production projects by capacity).[89] DOE expects SMR production with CCS to account for 50 to 80 percent of total hydrogen production in the U.S. by 2050, although the precise share of production for each method will depend on the prices of their corresponding feedstocks and possible technological innovation.[90] If affordable clean electricity is available, the production share for both electrolysis and SMR with CCS will likely be closer to 50 percent; whereas if the expansion of clean electricity generation is limited, the share for SMR with CCS will be larger.[91]

Figure 6. Announced clean hydrogen project activities

Source: The U.S. Hydrogen Demand Action Plan, Energy Futures Initiative (EFI), February 2023,https://energyfuturesinitiative.org/reports/the-u-s-hydrogen-demand-action-plan-2/, p. 30.[92]

Figure 7. Global distribution of clean hydrogen production projects by capacity (kt H2/year).

Source: International Energy Agency (IEA), “Hydrogen Production and Infrastructure Projects Database,” updated to October 2023, https://www.iea.org/data-and-statistics/data-product/hydrogen-production-and-infrastructure-projects-database. Projects included in dataset are in various stages: concept, feasibility study, demonstration, FID/construction, and operational.

Challenges

Transportation

Like any energy source, hydrogen is not without its challenges. Although the most abundant element in the universe, hydrogen is difficult to store and transport. It is highly flammable,[93] has a low-density by volume (albeit a high energy density by mass) and is lighter than air, which means it dissipates rapidly when released.[94] Hydrogen molecules are also the smallest molecules, which makes them more prone than methane to leakage through joints and microscopic cracks in existing natural gas pipelines and compressor stations.[95] Because of these characteristics, hydrogen gas is currently used mostly in close proximity to where it is produced.[96] Transportation contributes to the relatively high cost when compared to traditional fuel sources.

For more widespread use of hydrogen, infrastructure is needed for distribution. Currently, hydrogen is transported either through pipeline, compressed in high-pressure tube trailers, liquefied in hydrogen tankers,[97] or via chemical carriers such as ammonia. Cost-wise, compressed gas trucks make the most sense for smaller volumes and distances, while liquified hydrogen trucking becomes competitive at greater distances.[98]

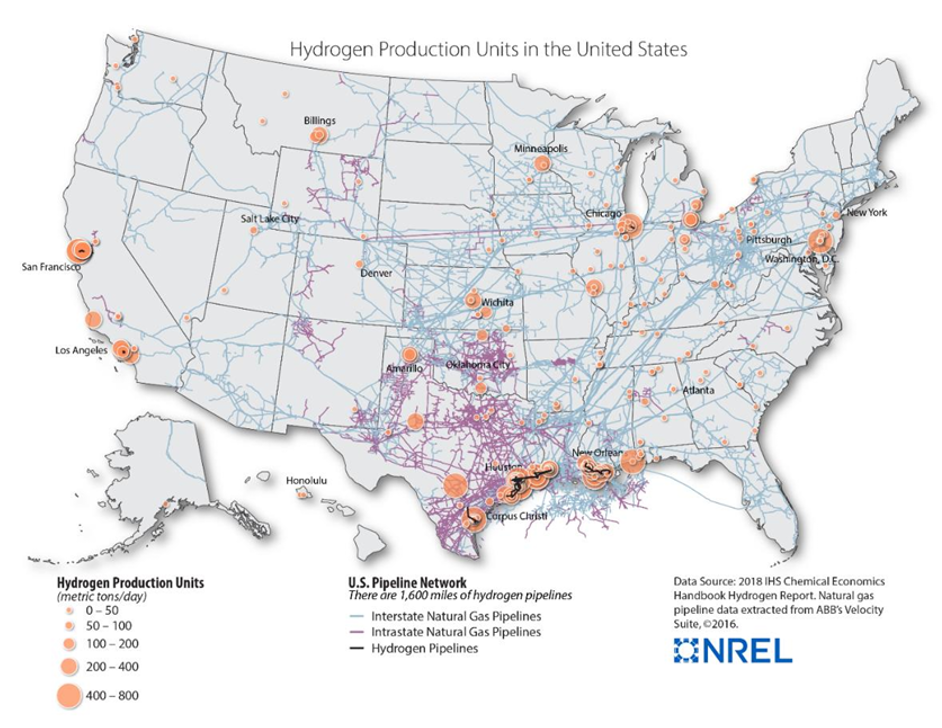

Pipelines may be the most cost-efficient method for transporting large volumes, but there is a limited amount of dedicated hydrogen pipelines in the country. Most of the 1,600 miles of hydrogen-dedicated pipelines that exist today in the U.S. are located near large hydrogen-consuming facilities such as refineries and chemical plants on the Gulf coast (see Figure 8).

Figure 8. Hydrogen production and transportation infrastructure in the United States, 2018.

Source: DOE, DOE National clean hydrogen strategy and roadmap, p. 43. Originally from NREL.

Building new pipelines involves high capital costs, necessitates large-scale offtake certainty and presents permitting challenges. It is possible to adapt existing natural gas pipelines to transport hydrogen, but this requires some reconfiguration, as hydrogen is corrosive to some metals, which can cause embrittlement of steel pipelines.[99] Potential solutions to this issue include measures such as applying coating barriers, lowering pipeline pressure and blending hydrogen with natural gas.[100] There are current initiatives exploring hydrogen blending into existing pipeline networks, and states like Hawaii already use a blend of up to 15 percent hydrogen in their grid. However, there is currently no industry consensus on blending limits for hydrogen in natural gas pipelines.[101] In addition, increased fossil fuel use for hydrogen production may require additional pipelines to transport carbon dioxide to authorized sequestration sites if the CO2 is not reused for enhanced oil or gas recovery or in the production of higher value chemicals or products.

If the use of hydrogen fuel cells in the transportation sector is to become widespread, there is also a need for the development of a network of fueling stations. There are currently around 81 public and private hydrogen fueling stations in the U.S. – most of them in California.[102]

Siting and permitting

Issues with the transportation of hydrogen are exacerbated by potential roadblocks related to siting and permitting of hydrogen infrastructure. Currently, the operation of a hydrogen pipeline involves oversight by various federal agencies and a patchwork of federal statutes and regulations.[103] As with oil pipelines, there is no single lead agency with centralized federal siting authority over hydrogen pipelines. To construct new interstate pipelines, developers require siting approvals from each implicated state.[104] Codes and standards will also have to be developed for hydrogen pipelines to transport hydrogen safely, accounting for embrittlement and the fact that it is highly flammable.

It is possible the Federal Energy Regulatory Commission (FERC) could take on the role of lead agency in the regulation of dedicated hydrogen transportation pipelines in the U.S., although this could require action from Congress, such as an amendment to the Natural Gas Act. Interstate pipelines that transport hydrogen blended with natural gas are likely to fall under FERC’s authority, but the precise percentage of hydrogen that can be blended into these pipelines is unclear. Typically, pipeline-quality natural gas is 95 to 98 percent methane,[105] although as mentioned above, Hawaii’s pipeline infrastructure already accommodates a blend of up to 15 percent hydrogen.[106] Most blending projects across the globe are located in Europe, Australia, Canada and the United States, with blends of up to 20 percent hydrogen.[107]

Emissions

Hydrogen is essentially a clean fuel, emitting only water when consumed in a fuel cell.[108] The combustion of hydrogen at high temperatures in the presence of air, however, can generate nitrogen oxide (NOx), a harmful pollutant that can contribute to the formation of ozone and particulate matter. Hydrogen combustion processes must be optimized and monitored to minimize any air quality impacts.[109]

The emissions associated with hydrogen production vary widely. Electrolysis-produced hydrogen can have a widely different carbon footprint depending on how the electricity used is generated. When using grid electricity – given the fuel mix that powers the grid today – its carbon intensity can be higher than SMR without CCS (see Figure 5 above).

It is also more prone than other gases to leaking into the atmosphere through microscopic cracks in pipelines,[110] and act as an indirect greenhouse gas by reacting with greenhouse gases such as methane, ozone and water vapor, and increasing their concentrations in the atmosphere.[111] Thus, care must be taken to use existing tools and technologies to mitigate leaks.

Cost

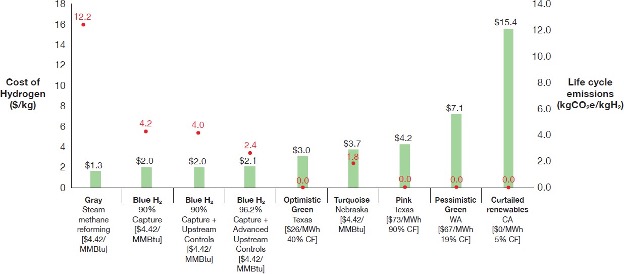

The cost of producing hydrogen may vary widely by feedstock, region and electricity generation mix, depending on resources and infrastructure available.[112] Cost parity between the various sources and production methods is a key factor in the development of a hydrogen marketplace. Without incentives, hydrogen production with natural gas is typically cheaper than via electrolysis with renewable energy, even if it includes carbon capture and storage (CCS).[113] See Figure 9 for an estimate of production costs for different production pathways.

Figure 9. Cost comparison of clean hydrogen production pathways, based on costs measured at specific projects (red dots correspond to lifecycle emissions, and green bars to cost of hydrogen per kg).

Source: Appendices to The U.S. hydrogen demand action plan, Energy Futures Initiative (EFI), p. 13.

Incentives from the Infrastructure, Investment and Jobs Act (IIJA) of 2021 and clean energy tax credits approved in 2022 as part of the Inflation Reduction Act (IRA) will reduce costs for all clean hydrogen production pathways (in a scenario where they all qualify), but there is uncertainty around how much these costs might decrease for each technology and whether cost reductions will be sufficient. Reducing the cost of production is a critical component of enabling demand, as otherwise, stakeholders might not have incentive to risk switching to clean hydrogen.

According to DOE’s Liftoff report, the hydrogen Production Tax Credit (PTC) approved in 2022 makes clean hydrogen production via electrolysis cost-competitive or comes close to cost-parity, with fossil-based production within 3 to 5 years, for sectors such as refining, ammonia, steel (new build DRI) and heavy-duty trucking in states with a low-carbon fuel standard.[114] However, a recent study by Energy Futures Initiative (EFI) suggests that clean energy tax credits approved in 2022 won’t be sufficient to make production costs competitive enough for some sectors to switch to clean hydrogen.[115] EFI underlines the importance of leveraging regional hydrogen hubs, which help market players scale up while jointly managing risk, as a key pathway to help create this demand and construct a national hydrogen network.[116] Importantly, global adoption of clean hydrogen will eventually require costs to be competitive without subsidies as most countries, developing nations in particular, will not have the economic or social tolerance to pay for a green premium. Widespread adoption internationally is paramount if hydrogen is to become a key driver of emissions reductions in hard-to-abate sectors globally.

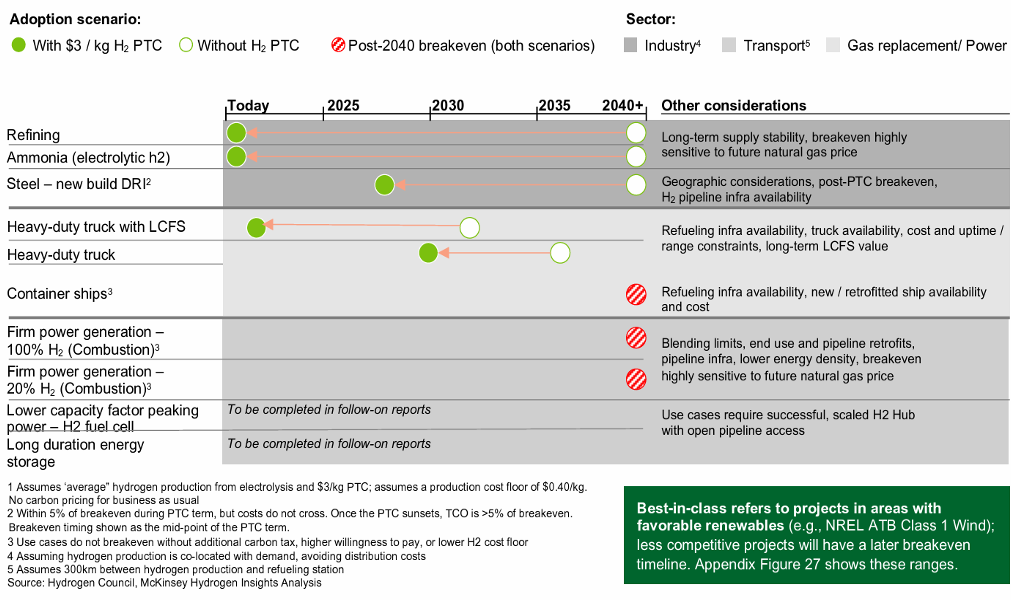

Cost-competitiveness of different clean hydrogen production methods will depend on a variety of factors, including willingness to pay in end-use sectors (especially after tax credits expire), natural gas prices, clean electricity prices, electrolyzer costs and transportation and storage costs, among other potential policy and technological drivers.[117] DOE expects that by 2030, all end-uses will at least be profitable for producers co-located with offtakers or in proximity to storage caverns and pipelines.[118] After the PTC sunsets, it expects most industrial offtakers to have sufficient willingness to pay, but this might prove more difficult for the heat and power sector.[119] See Figure 10 below for DOE estimates on when hydrogen might achieve a breakeven price in different sectors.

Figure 10. Projections for timing of hydrogen achieving cost-parity in different sectors.

Source: DOE, Pathways to commercial liftoff: Clean hydrogen, p. 39.

Scaling

Three of the dominant technologies that are needed for the clean hydrogen sector to grow are electrolyzers, fuel cells and carbon capture systems. Currently, Europe is the leading manufacturer of electrolyzers, with China and Japan also having a substantial head start, but the market for this technology is currently fragmented and small.[120] China is able to produce electrolyzers at a much lower cost than the U.S. or Europe and has more established supply chains for electrolyzer components and raw materials.[121] China accounts for around 40 percent of global electrolyzer manufacturing capacity today.[122] It has invested heavily in alkaline electrolyzers, however, which are cheaper but cannot ramp up as quickly as PEM models, which are more adequate to operate with variable renewable electricity sources[123] According to the IEA, capital expenditure (CAPEX) requirements for alkaline electrolyzers range from $500 to $1,400, whereas for PEM these are between $1,100 to $1,800, and $2,800 to $5,600 for SOEC.[124]

There are some potential mineral and raw materials supply chain constraints that might affect the U.S.’ ability to ramp up electrolyzer production. Iridium, for example, is needed for the manufacturing of PEM electrolyzers, and 80 percent of the U.S. supply comes from South Africa, with scarce opportunity for domestic production.[125] Some electrolyzer technologies don’t require minerals such as iridium, but may have other drawbacks such as being in early commercial or laboratory stages. Regardless of the technology employed, it is a key moment to avoid reliance on geopolitical rivals for electrolyzer components as the U.S. ramps up manufacturing of them.

While electrolyzers use water and electricity to make hydrogen, fuel cells directly convert hydrogen into electricity, emitting water vapor as a biproduct. They have various mobile and stationary applications: They can power vehicles, serve as backup power, provide power in remote locations, act as portable generators and can be used for most of the same purposes as batteries.[126] Between 2008 and 2020, the cost of fuel cells for vehicles declined by 70 percent internationally,[127] and the cost will continue to decrease as more research and development into this technology is conducted. Scaling up the use of hydrogen fuel cells in the transportation sector, however, will depend not only on advancements in fuel cell technologies but of the build-out of refueling, storage and other supporting infrastructure, certainty in hydrogen supply and the cost of alternatives.[128]

Scaling carbon capture technologies will also be critical for the development of a hydrogen economy, as SMR production with CCS is likely to be the predominant method of production of clean hydrogen in the near-term. Although IIJA funding and recent enhancements to the 45Q tax credit have provided substantial support for building out our nation’s capacity to capture and store carbon, carbon capture technologies have not yet achieved the level of maturity and cost reduction needed for widespread adoption.[129] The situation is further complicated by the limited capacity of the Environmental Protection Agency (EPA) to process permit applications for carbon storage wells, known as Class VI wells, which are used to inject CO2 into deep rock formations for geologic sequestration.[130] Following a flood of applications between 2022 and 2023, as of March 2024 there were 130 Class VI well permits under review at EPA.[131] This could have repercussions for the speed at which blue hydrogen production can expand.

Demand-side considerations

Part of the challenge in creating a robust hydrogen economy is the existence of corresponding demand to absorb the increase in production that DOE programs hope to spur. Growth in demand, in turn, is partially dependent on offtaker confidence in a long-term, affordable supply of clean hydrogen – meaning a reasonable expectation that hydrogen is likely to become cost-competitive on its own after the hydrogen PTC tax credit sunsets.

In some sectors that already use hydrogen and have established markets and distribution infrastructure, such as ammonia and oil refining, the existing demand will facilitate the adoption of clean hydrogen.[132] According to DOE, for these two end-uses, the hydrogen PTC makes clean hydrogen production from both electrolysis and SMR with CCS immediately cost-competitive when hydrogen production is co-located with offtakers.[133]

In steelmaking, the adoption of hydrogen in DRI-EAF will require very high volumes, and if co-location is not possible, transportation infrastructure with the capacity to supply large quantities will need to be retrofitted or built.[134]

After refining and ammonia, hydrogen fuel cells in heavy-duty trucking will likely be the next end-use to become cost effective, according to DOE.[135] Although electric medium and heavy-duty vehicles might have advantages over fuel cell vehicles for smaller ranges, hydrogen fuel cells will be especially attractive for long-haul trucking, where electric vehicles face the disadvantage of lower ranges and longer charging times.[136] Hydrogen is also attractive for some short-range uses, such as forklifts, with over 50,000 hydrogen forklifts already in operation across the country.[137] The main challenge to hydrogen fuel cell vehicle adoption is scaling up the production of the vehicles themselves, as well as the development of the refueling infrastructure they would require. [138]

Hydrogen production has a higher technology readiness level than other clean energy technologies, and existing market pull from established industrial usage. However, according to DOE, uncertainty over long-term offtake has somewhat held back project finance and widespread commercial debt.[139] Only around 10 percent of the approximately 12 MMT/year of clean hydrogen production capacity announced in the U.S. as of June 2023 had reached final investment decision (FID), which DOE attributes mainly to the lack of long-term offtake.[140] DOE’s “H2 Matchmaker” program, for example, saw a significant mismatch between the high number of suppliers to a low number of customers.[141] One reason for this is that, broadly speaking, hydrogen producers tend to prefer long-term contracts that provide them with certainty, whereas buyers tend to prefer short-term contracts to avoid being locked into a set price for an extended period, and thus be able to take advantage of decreasing prices as the hydrogen industry scales up.[142]

In October of 2023, the Biden Administration announced that $1 billion of IIJA hydrogen hub funds would be used for a one-time DOE demand-side support program.[143] The program will be run in partnership with DOE by a consortium that includes the EFI Foundation, S&P Global, the financial exchange operator Intercontinental Exchange, Massachusetts Institute of Technology Energy Initiative and law firm Dentons.[144] As of May 2024, it has yet to be defined what demand-stimulating tools the program will make use of.[145] Some of the policies being discussed for example are a “market maker” tool, a price floor with procurement, and pay-for-difference contracts. These examples are by no means exhaustive, but provide a snapshot of some of the policy tools under consideration.[146]

- A market-maker mechanism involves an intermediary that would purchase a product – in this case, hydrogen – and resell it to customers, absorbing the cost difference between both transactions. If the product sells for less than what it was purchased at, the intermediary takes the loss; but if it sells at a higher price, the intermediary profits.[147]

- A price floor with procurement involves a price floor being set that companies can expect to receive for their product, regardless of market fluctuations. If the market price is above the price floor, the third party is under no obligation to procure the product, but steps in if the market price dips below the price floor.[148]

- A pay-for-difference contract is a mechanism whereby a third party would enter into an agreement with a hydrogen company to set a reference price that would act as a price floor. If the price of hydrogen in the market falls below that reference price, then the third party would reimburse the producer for the difference. If the market price is above the reference price, then the producer keeps the profit. It is a way of subsidizing a private transaction, whereas a price floor with procurement commits the third party (often a governmental entity) to procure the product.[149]

A global market for hydrogen

Private sector initiatives

By 2050, there could be a global market for clean hydrogen worth $1.4 trillion.[150] Many companies are already moving towards hydrogen to both meet their net zero goals and become competitive in this burgeoning market:

- Microsoft, for instance, is investing in hydrogen-powered generators to provide a backup system to data centers, replacing generators that previously relied on diesel fuel.[151] These systems are crucial to keeping servers running in the case of a blackout. After a successful pilot program, the company plans on training its employees on hydrogen fuel cells and deploying the technology at one of its new data centers.

- Mitsubishi Power’s Takasago Hydrogen Park in Japan is manufacturing gas turbines for power generation that can utilize up to 30 percent hydrogen and will be used at the Intermountain Power Project (IPP) in Utah when it reaches full operation in 2025.[152] The project will obtain hydrogen fuel from the Advanced Clean Energy Storage project (ACES Delta hub), which is also being developed by Mitsubishi in partnership with Magnum Development.[153]

- Shell is investing heavily in hydrogen as a way to decarbonize industry and transportation. It has partnered with several projects aiming to produce hydrogen at a large scale, including investing in a renewable hydrogen plant in the Netherlands. Once operational in 2025, this plant will provide 60,000 kg of hydrogen per day. [154]

- ExxonMobil is planning to build a hydrogen production plant outfitted with carbon capture technology at one of its sites to create fuel for one of their refineries.[155]

- 3M is investing in the research and development of hydrogen technology, particularly green hydrogen, in order to lower carbon emissions and make hydrogen technology more cost-effective.[156]

- Companies such as Bloom Energy or Nikola have developed efficient and competitive fuel cell technologies and applications.

- A burgeoning ecosystem of innovative startups focusing on hydrogen and electrolyzer manufacturing is also taking shape. Some companies are developing innovative methane pyrolysis solutions, while others are focusing on electrolyzer manufacturing – established PEM and alkaline technologies, as well as SOEC.

Global movers

While China is the single biggest hydrogen producer internationally, mostly from coal facilities,[157] the vast majority of hydrogen produced here in the U.S. (and across the globe) is from natural gas.[158] Paired with carbon capture and sequestration technology, producing hydrogen from methane will be an important piece of scaling up a clean hydrogen economy. As the world’s top producer of natural gas,[159] the United States is well-positioned to capitalize on the opportunity that hydrogen presents to assert global leadership in clean energy technologies utilizing an abundant domestic resource. As more countries look to create low-carbon economies, the U.S. can be a leader in clean hydrogen production for both domestic consumption and exports as well. Many countries with a different resource mix may find that it is more cost effective to import hydrogen rather than produce it themselves,[160] which the U.S. stands to benefit from.

However, the U.S. may need to move quickly if it is to capitalize on advantages such as low-cost natural gas and our ample potential for low-cost scaled (geological) storage.[161] The development of an international hydrogen economy is speeding up, with various agreements for the import and export of clean hydrogen taking shape. Stakeholders in the Netherlands, for example, have signed Memorandums of Understanding (MoUs) for the import of clean hydrogen with Chile and the United Arab Emirates (UAE).[162]

China is currently the leading producer and consumer of hydrogen globally, and is leading in electrolyzer deployment as well, with currently over 200MW of installed capacity, around 30 percent of the global total.[163] The Chinese government has also signed MoUs with countries such as Serbia[164] and Saudi Arabia,[165] and Chinese companies have signed MoUs with various energy companies abroad to develop China’s hydrogen industry.[166]

Japan, which imports nearly 90 percent of the energy it uses, is betting heavily on hydrogen and aims to become a leader in the global hydrogen economy.[167] Its revised 2023 Hydrogen Strategy has set a goal of increasing the supply of hydrogen and ammonia in Japan to 12 MMT by 2040 and 20 MMT by 2050.[168] The country has made significant investments in hydrogen research and development, including fuel cell technology and using ammonia to overcome storage and transportation issues. It has signed MoUs with Chile, the EU, the UAE and Saudi Arabia, among others, in its quest to establish a reliable supply of clean hydrogen and ammonia.[169] It also signed an agreement with Australia in January of 2022, and that same month, Japan received from Australia the world’s first shipment of liquefied hydrogen.[170]

Many American companies are also taking initiative and signing agreement,[171] but global competitors and allies alike are quickly proliferating and expanding their reach. Any substantial delay in developing the U.S. hydrogen sector will make it more difficult for American companies to compete internationally.

Federal support for hydrogen technology

The IIJA granted $9.5 billion dollars to jumpstart investment in hydrogen production and infrastructure.[172] It contained significant funding for hydrogen technologies, with $8 billion for the Regional Clean Hydrogen Hubs Program,[173] $1 billion for a Clean Hydrogen Electrolysis Program and $500 million for clean hydrogen manufacturing and recycling initiatives.[174] It also provided over $12 billion in federal funding for the demonstration and deployment of carbon management technologies, which are crucial in the production of blue hydrogen.[175]

DOE also launched Hydrogen Shot,[176] the first Energy Earthshot, in June 2021, with the goal of reducing the cost of clean hydrogen by 80 percent to $1 per kilogram in one decade. It is managed by DOE’s Hydrogen and Fuel Cell Technologies Office (HFTO) and is another key axis of the administration’s hydrogen strategy.

In 2022, the IRA included a number of tax incentives to accelerate deployment of clean energy technologies, several of which are focused on or at least applicable to hydrogen production.

Hydrogen hubs

DOE’s Regional Clean Hydrogen Hubs program, H2Hubs, is managed by the Office of Clean Energy Demonstrations (OCED). It seeks to stimulate technological and market development and create economies of scale for hydrogen production, pooling risk and resources in a way that would be difficult for a single investor or developer to do on a stand-alone basis.[177] The seven awardees (see Figure 11) were announced in October 2023:[178]

- Appalachian Hydrogen Hub (Appalachian Regional Clean Hydrogen Hub, ARCH2)

- Location: West Virginia, Ohio and Pennsylvania

- Hub will leverage the region’s ample low-cost natural gas resources to produce clean hydrogen and permanently store the associated CO2 emissions. It will also employ renewable generation. Intended end uses include power generation, industrial processes, transportation, and residential and commercial heating. The hub anticipates creating over 21,000 direct jobs.

- California Hydrogen Hub (Alliance for Renewable Clean Hydrogen Energy Systems, ARCHES)

- Location: California

- Hub will produce hydrogen from renewable energy and biomass, aiming for end uses such as public transportation, heavy duty trucking and port operations. The hub anticipates creating 220,000 direct jobs.

- Gulf Coast Hydrogen Hub (HyVelocity Hub)

- Location: Texas (centered in Houston)

- Hub will produce hydrogen using natural gas with CCS, as well as renewables-powered electrolysis. It will also leverage the region’s geology and develop salt cavern hydrogen storage, a large open access hydrogen pipeline and hydrogen fueling stations. End uses targeted include fuel cell electric trucks, industrial processes, ammonia, refineries and petrochemicals, and marine fuel (e-methanol). The hub anticipates creating around 45,000 direct jobs.

- Heartland Hydrogen Hub (Heartland Hub, HH2H)

- Location: Minnesota, North Dakota and South Dakota

- Hub will use nuclear, renewable and fossil with CCS hydrogen production pathways.[179] Targeted end uses include power generation and the production of fertilizer to benefit farmers and help reduce regional agricultural emissions. It anticipates the creation of over 3,880 direct jobs.

- Mid-Atlantic Hydrogen Hub (Mid-Atlantic Clean Hydrogen Hub, MACH2)

- Location: Pennsylvania, Delaware and New Jersey

- Hub will use renewable, nuclear and fossil fuel-based pathways to produce clean hydrogen. It will repurpose historic oil infrastructure and existing rights-of-way, using renewables and nuclear electricity to power both established and cutting-edge electrolyzer technologies. Targeted end uses include heavy transportation, manufacturing and industrial processes, combined heat and power, and expanding hydrogen distribution infrastructure such as bus depots and fueling stations. It anticipates creating 20,800 direct jobs.

- Midwest Hydrogen Hub (Midwest Alliance for Clean Hydrogen, MachH2)

- Location: Illinois, Indiana and Michigan

- Hub will leverage renewable, nuclear and fossil fuel-based pathways to produce clean hydrogen. Targeted end uses include steel and glass production, power generation, refining, heavy-duty transportation and sustainable aviation fuel. It anticipates creating 13,600 direct jobs.

- Pacific Northwest Hydrogen Hub (PNWH2 Hub)

- Location: Washington, Oregon and Montana

- Hub aims to produce hydrogen exclusively via electrolysis using renewable energy including hydropower. Targeted end-use sectors include heavy duty transportation, agricultural fertilizer production, industry (generators, peak power, data centers, refineries) and seaports. It anticipates creating over 10,000 direct jobs.

Figure 11. Selected DOE hydrogen hubs.

Source: Office of Clean Energy Demonstrations (OCED), DOE, https://www.energy.gov/oced/regional-clean-hydrogen-hubs-selections-award-negotiations.

The hydrogen hubs have been hailed as a linchpin of the path towards scaling and reducing costs, as well as developing a successful hydrogen industry. They are a necessary condition of incorporating hydrogen as a fuel source in our economy – yet not a sufficient one. Tax incentives from the IRA – particularly the 45V hydrogen production tax credit (PTC) – were designed by the administration to work in tandem with the hydrogen hubs to jumpstart the industry and set it on a path to affordable production at scale. The implementation of 45V, however, has been fraught with delays and disagreements. Of particular concern is guidance on 45V released by the U.S. Treasury Department and the Internal Revenue Service (IRS) in December of 2023, which we discuss in the following section.

Tax incentives for hydrogen

The IRA established a new PTC for the production of clean hydrogen, under section 45V of the tax code, which was envisioned as a complement to DOE’s H2Hubs program.[180] The value of the 10-year 45V hydrogen PTC is tiered based on lifecycle emissions (calculated from well-to-gate using the Greenhouse Gases, Regulated Emissions, and Energy Use in Transportation (GREET) method), ranging from a credit of $0.60/kg for hydrogen produced with an emissions intensity of 2.5-4 kg CO2eq/kg of hydrogen, to a maximum of $3/kg of hydrogen produced with an emission intensity of 0-0.45 kg CO2eq/kg of hydrogen (see Figure 12). For taxpayers to qualify for the full value of the credit, they must meet the IRA’s prevailing wage and registered apprenticeship requirements. Alternately, under section 48(a), producers can opt for an Investment Tax Credit (ITC) equal to a percentage of their capital expenses, also based on lifecycle emissions.

| Lifecycle GHG emissions (kg CO2e/kg H2) | PTC value ($/kg H2) | ITC percentage |

| 2.5-4 | $0.60 | 6% |

| 1.5-2.5 | $0.75 | 7.5% |

| 0.45-1.5 | $1.00 | 10% |

| 0-0.45 | $3.00 | 30% |

Figure 12. Values of the 45V Production Tax Credit and the 48(a) Investment Tax Credit.

Source: based on Incentives for Clean Hydrogen Production in the Inflation Reduction Act (rff.org).

Additionally, the IRA increased the value of the 12-year tax credit for carbon sequestration (45Q), which can be claimed for hydrogen production that uses carbon capture. It increased the value of 45Q for geologic storage from $50 to $85 and extended the deadline for eligible projects to commence construction from 2023 to 2032.[181]

The developer of a project to produce hydrogen with fossil fuels using CCS could opt for the 45Q credit. They might also qualify for the 45V credit, but only if the emissions profile of their hydrogen production is lower than 4 kg CO2e/kg H2. The 45V and 45Q credits are not stackable, however, meaning that a producer cannot claim both the 45V and 45Q credits. As for the choice between the PTC or the ITC, generally speaking (with variation depending on location and company in question), in theory the ITC would make more sense for projects with higher capital costs, and the PTC would better serve projects with a higher capacity factor,[182] which points to the amount of hydrogen produced relative to capacity.[183] To date, however, few producers have been interested in claiming the ITC. There are various reasons for this, including the fact that it cannot be claimed if a facility was already under development before 2023, and because it is subject to recapture (when part of the credit would have to be repaid to the Treasury) if lifecycle emissions increase above the level of that first year, if the producer fails to submit an emissions verification report by the deadline, or if they fail to comply with wage and apprentice requirements. [184]

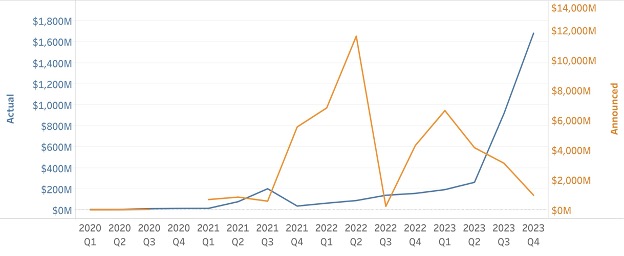

The hydrogen PTC has been credited with helping jumpstart significant investments in hydrogen production.[185] According to the Clean Investment Monitor (CIM),[186] a tool developed by the Rhodium Group and MIT to track public and private clean energy investments, the value of hydrogen investments announced in 2023 totaled around $14.9 billion, and the amount of investments made that same year amounted to just over $3 billion.[187] The amount of announced investments has fluctuated year by year, with the largest surges seen in Q2 of 2022 and Q1 of 2023, but actual investments in hydrogen have steadily grown in the past three years, with a record $1.68 billion in Q4 of 2023 – a 4,471 percent increase from Q4 of 2021 when the IIJA was signed into law and a 1,105 percent increase since Q3 of 2022, when the IRA was passed (see Figure 13). According to the Clean Economy Tracker (CET), another clean energy investment tracking tool, the amount of private-led investment that went to just electrolyzer manufacturing in 2023 amounted to $522 million.[188] See also Figure 14 for a breakdown of hydrogen investments by state.

Figure 13. Investments in hydrogen projects since 2020, announced and actual. Announced investments are tracked in orange (Y-axis on the right) and actual investments in blue (Y-axis on the left).

Source: Clean Investment Monitor (CIM), Database (cleaninvestmentmonitor.org)

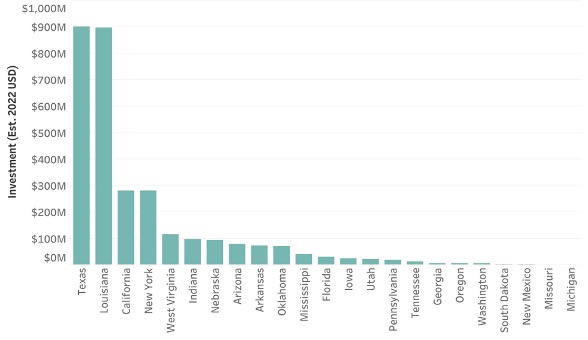

Figure 14. Actual investments in hydrogen projects by state in 2023 (est. 2022 USD).

Source: Clean Investment Monitor (CIM), https://www.cleaninvestmentmonitor.org/database.

On Friday December 22, 2023, Treasury released a draft of the much-anticipated guidance with a Notice of Proposed Rulemaking (NPRM),[189] in which the Treasury requested technical assistance and public comment on numerous design options. Some segments of industry received the proposed guidance positively and expressed support for a strict approach to emissions accounting, while others manifested concern that this level of rigor might come at the expense of a swift deployment of clean hydrogen technologies. The comment period for the rule ended on February 26, 2024, and a public hearing regarding the guidance was held on March 25, 2024. The extended delay in finalizing regulations for this new credit will likely limit near-term investor interest.

Uncertainty surrounding 45V

Supply chain delays, lack of long-term offtake, increased interest rates, higher labor and material costs, and a slow policy rollout, including of the 45V rule, have hampered clean hydrogen deployment, particularly of the more novel electrolyzer-derived variety.[190] Uncertainty about eligibility and what credit tier level a developer may qualify for has also resulted in some companies delaying final investment and construction plans. For example, the proposed regulations do not clearly provide electrolytic hydrogen produced with existing clean power (such a nuclear or hydropower) a pathway for eligibility, although they also do not explicitly exclude it.184 It is likely that projects that don’t already explicitly meet the strictest approach to carbon accounting will elect to pause plans until the final rule is released.

The “three pillars”[191]

Much of the guidance, as well as the regulatory debate surrounding it, has centered around three elements that are meant to ensure that produced hydrogen is indeed low-emissions on a lifecycle emissions basis: incrementality (also called additionality), deliverability and time-matching – often termed the “three pillars.”

Incrementality

Incrementality, or additionality, refers to a requirement that would ensure electricity used for hydrogen production comes from (a) new zero-emissions energy sources, (b) increasing the generation rate of existing renewable sources or (c) using curtailed clean electricity generation that would have otherwise not have been produced.[192] The intention is to prevent electrolyzers from drawing on renewable sources that would otherwise feed the grid – in other words, to ensure the use of renewables to power hydrogen production without reducing the share of zero-emissions electricity generation on the grid.

The proposed guidance stipulates that in order to be considered “incremental” or “additional,” the facility generating electricity for hydrogen production cannot begin commercial operation more than 36 months before the hydrogen production facility is placed in service. Under certain circumstances, existing electricity generation may also satisfy the incrementality requirement, such as:

- Facilities that make certain upgrades, such as fossil fuel-based electricity generating facilities that add CCS capabilities, provided this was done within the 36-month period.

- Facilities that are “uprated” (meaning an increase in nameplate capacity) within those 36 months.

- Existing power generation plants that make other improvements, provided they meet the “80/20 test” – meaning that the value of the used property does not exceed 20 percent of the facility’s total value.

It is worth noting that this requirement as it currently stands is more stringent than that adopted by the European Union, which allows a phase-in period with incrementality not kicking in until 2028.[193] Various stakeholders have suggested that the U.S. adopt a similar phase-in period for incrementality or allow some level of grandfathering for this requirement, or some degree of recognition of existing state-level grid decarbonization policies.[194]

The additionality requirement, as written, would also bar any producers using existing hydropower or nuclear assets to produce hydrogen to qualify for the credit, as these types of facilities take years –sometimes more than a decade– to permit and construct.[195] The nuclear and hydropower industries have voiced their concern over incrementality,[196] given that if it impedes any existing low- or zero-carbon assets from being used to meet the definition of clean hydrogen, companies would miss the opportunity to utilize two of the largest source of zero-emissions electricity in the U.S. to kickstart the hydrogen economy, as well as help revitalize the U.S. nuclear industry,[197] which will need to be leveraged if the U.S. is to meet its decarbonization goals. In 2023, nuclear facilities were responsible for 18.6 percent of electricity generation, and hydropower for 5.7 percent.[198] In terms of their share of total low- and zero-emissions generation, nuclear and hydropower were responsible for 46.4 and 14.4 percent, respectively.[199]

Comments on the proposed rule have elicited strong reactions – both positive and negative – and have impacted the plans of various stakeholders that hope to participate in the hydrogen economy. Some energy companies have put their nuclear-powered hydrogen projects on hold as they await the final IRS guidance. Constellation Energy, for example, has paused their nuclear-powered clean hydrogen production facility, which they have been working on for the Midwest Alliance for Clean Hydrogen (“MachH2”) hydrogen hub, given the uncertainty surrounding 45V. In their 45V comments to Treasury, they state that if the guidance is not revised, they could be forced to cancel their participation in the hub project.[200] It is also worth noting that leaders of all seven DOE hydrogen hubs expressed concern over the proposed rule in a letter to Treasury in February 2024.[201] The letter states that if the guidance is not significantly revised, many hub-related projects might no longer be economically viable. It exhorts Treasury to finalize a rule that would “not disadvantage any type of clean hydrogen production by limiting it exclusively to new sources, and ensure the credit remains flexible and technology neutral.”[202]

Other industry stakeholders, on the other hand, have voiced strong support for a strict three pillars approach. Air Products, for example, which is part of the ARCHES hydrogen hub in California, opposes any exceptions to the additionality requirement, arguing that it would unfairly disadvantage projects that are already compliant with the strictest three pillars requirements, and would disincentivize compliant projects in the future because of their cost disadvantage.[203]

Treasury sought comment on other pathways that might satisfy the incrementality requirement, and which would allow the use of existing power plants, such as:

- Electricity generation facilities that avoid retirement because of their association with a hydrogen production plant. Stakeholders such as the Nuclear Energy Institute (NEI) cautioned that if adopting this criterion, Treasury should avoid imposing complicated, burdensome tests to demonstrate that a nuclear unit is at risk of retiring.[204]

- Electricity generators that demonstrate zero or minimal induced grid emissions through modeling. Generators might prove, for example, that the renewable electricity used would otherwise be curtailed, or that generation in the region is from minimally emitting sources and that an increased load would not affect emissions. Some stakeholders have voiced concern over the complexity involved in this approach.

- A formulaic approach, whereby 5 percent of hourly generation from low-emitting generators placed in service before January 1, 2023, could be used. This would avoid the complications involved in modeling, but some have raised concerns that emissions and costs from this pathway could prove too high depending on the time that this 5 percent is used.[205] Stakeholders such as the National Hydropower Association (NHA), on the other hand, have argued that a 5 percent carveout is too small, as it would disadvantage smaller existing hydropower facilities, which constitute around 89 percent of existing waterpower.[206] Since smaller hydropower facilities have a smaller capacity, they would naturally provide a higher percentage of the electricity an electrolyzer would use.

Deliverability

Deliverability seeks to ensure that electricity-based production obtains clean energy from local sources to circumvent potential congestion issues.[207]

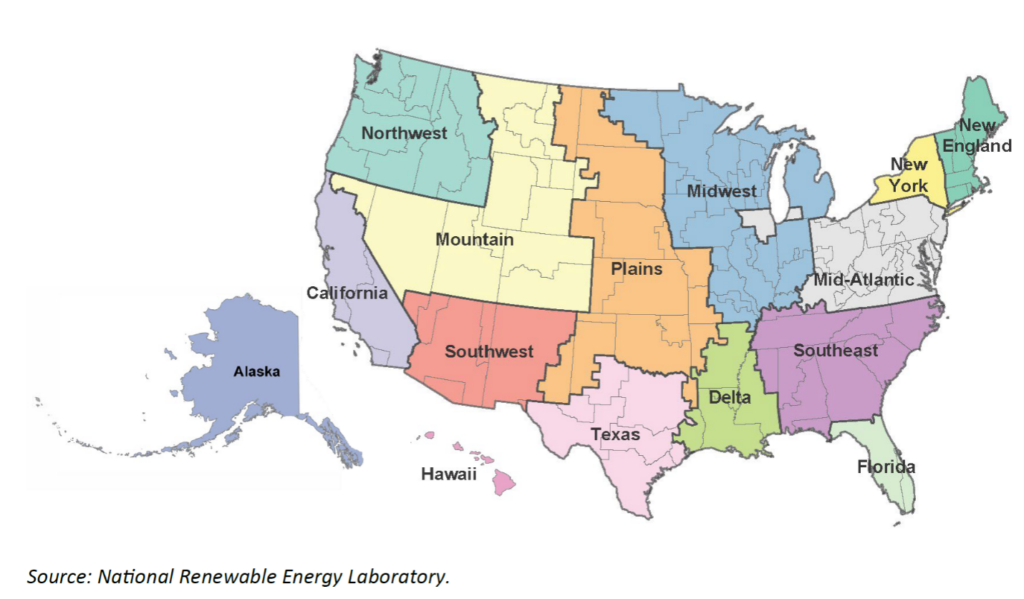

There was not much controversy over this pillar, and the draft guidance did not include anything unexpected. It specifies that electricity used should be obtained from the same region (as defined in DOE’s 2023 National Transmission Needs Study – see Figure 15) as the hydrogen production facility.[208]

Figure 15. Regions considered for the deliverability requirement.

Source: National_Transmission_Needs_Study_2023.pdf (energy.gov)

Temporal matching

Temporal matching seeks to ensure that the amount of renewable power put on the grid “matches” the amount of power consumed by hydrogen production so that said production does not increase emissions. Electrolytic production of hydrogen using grid electricity has been rated by various agencies as one of the highest-emitting pathways, and this requirement seeks to address that.

The draft guidance proposes a transitional period for phasing in hourly matching, whereby annual matching would be allowed for electricity generated before January 1, 2028. The guidance landed on a requirement that avoids the strictest option of requiring hourly matching on day one, although more stringent than the most flexible approach of limiting requirements to annual matching. It is worth noting that the proposed phase-in period is shorter than the guidelines adopted by the European Union, which will not implement hourly matching until 2030, with monthly matching in place until then.[209]

Some industry stakeholders have raised concerns that the timeline to phase in hourly matching is too accelerated, and that there are increased costs and technical challenges associated with standing up hourly tracking systems.[210] Some suggestions to address this include proposals for first movers to remain on annual matching for the life of the credit (also called “grandfathering”),[211] or a compromise whereby a certain percentage – some have proposed 15 or 20 percent – of a facility’s generation is exempted from hourly requirements for the life of the credit.[212]

Others, such as Hy Stor Energy, fully support hourly matching and argue that allowing grandfathering or relaxing requirements to annual matching would significantly drive up emissions from hydrogen production, as Hy Stor lays out in a letter to the Treasury, also signed by Air Products, and six other hydrogen project developers.[213]

While some electrolyzer manufacturers believe that hourly matching will actually drive the market towards U.S.-produced electrolyzers,[214] others theorize that it will drive investment away from the United States. Speaking at the Hydrogen Transition Summit held during COP28 on December 7, 2023, for example, Jorgo Chatzimarkakis, CEO of Hydrogen Europe, counseled the United States to not adopt hourly correlation, which he equated with an unrealistic “electrolyzer-only” strategy with costs that would prove far too high.[215] He predicted that under this regime, hydrogen investments would divert to Europe, Australia or other regions.

One thing that all stakeholders can agree on, however, is that the industry needs certainty. During the March 25th hearing on 45V, many participants urged Treasury to release the final guidance as soon as possible.

On the 45VH2-GREET model

The Greenhouse Gases, Regulated Emissions and Energy use in Technologies (GREET) model was developed by DOE’s Argonne National Laboratory to evaluate lifecycle emissions to inform RD&D directions and performance goals. 45VH2-GREET is the model that has been adopted by Treasury to determine emissions rates for purposes of the hydrogen PTC.[216] It is to be updated yearly.

One concern, raised particularly by companies intending to produce hydrogen with natural gas coupled with CCS, is that 45VH2-GREET model locks in certain emissions data related to the carbon intensity of natural gas production as “background data” and uses a national average that those inputting their data in the model cannot modify. These companies argue that even though they are doing a lot to reduce upstream methane leakage and generally to reduce emissions in their supply chain, under the current 45VH2-GREET model, they won’t be able to get credit for it, even when the lifecycle emissions of their natural gas production are lower than the national average. Many of these companies have requested that Treasury allow some of the “background data” to be converted to “foreground data” and allow companies to input their own information.[217]

So what does the future hold for 45V guidance?

Treasury and the IRS are now sorting through the nearly 30,000 comments received during the comment period for 45V – a testimony to the high stakes involved.[218] Many environmentalist groups praised the draft rule, as it focused heavily on ensuring that only new zero-carbon electricity is used to produce hydrogen, and they expressed concern that adopting more flexible guidelines could lead to higher emissions. The broader call from the power sector and a majority of hydrogen producers, however, is that the rule needs more flexibility if producers are to scale-up clean hydrogen production sufficiently for it to become cost-effective without a subsidy. It is still unclear when Treasury might finalize the 45V guidance, but industry is eager for the rules of the hydrogen game to be defined so they can decide what projects to move forward with and how.

CRES Forum Policy Recommendations

Scaling up a robust and competitive hydrogen industry in the United States will require pulling a variety of policy levers to strike a balance between the right amount of incentives, ensuring the cleanest production possible and allowing developers enough leeway to get their projects off the ground. In order to reduce costs quickly enough for the sector to become competitive on its own and to shape the United States into a world leader in clean hydrogen technologies and exports, we outline the following recommendations:

1. Continued investment in research and innovation

DOE’s Hydrogen Program[219] promotes research on the use of hydrogen across multiple applications and sectors. Continuing to support federal hydrogen programs will be instrumental in ensuring America is competitive in a global hydrogen market. Initial government action will catalyze innovation in the private sector down the road.

- Continued and sufficient funding for the Hydrogen Fuel Cell and Technologies Office (HFTO) within DOE’s Office of Energy Efficiency and Renewable Energy (EERE), which supports the lion’s share of RD&D on clean hydrogen technologies. Of particular importance is research to improve and scale up electrolyzer technologies, which will be key for reducing the cost of clean hydrogen production. Other key priority areas for hydrogen RD&D moving forward also include solving problems related to supportive infrastructure, such as hydrogen transportation and storage,[220] and hydrogen-based processes for the production of steel, aluminum and cement.[221]

- Continued and sufficient funding for the Office of Clean Energy Demonstrations (OCED) at DOE. As the office currently tasked with managing the Regional Clean Hydrogen Hubs program, and given that the hubs will be crucial kick-starters for the clean hydrogen economy, ensuring continued funding for this office is crucial. Hubs projects are long-term investments that will require continued program management to ensure they are running successfully.

- Maintain federal support for hydrogen in the Loan Programs Office (LPO), which can provide key support for scaling up innovative hydrogen technologies that may have difficulty obtaining funding to reach widespread commercialization. For example, the office is providing crucial financing for projects such as the Advanced Clean Energy storage hub in Delta, Utah (ACES Delta), set to become the largest clean hydrogen storage facility in the world.[222] And naturally, like any large federal program, proper oversight ensuring responsible stewardship of taxpayer dollars is important.

2. Articulate an explicit export strategy

Other nations and supra-national blocs, such as the EU, have clearly incorporated the international dimension into their hydrogen strategies.[223] The United States has the potential and resource advantage to become a leading exporter in the global clean hydrogen market, and any updates to existing federal hydrogen strategies should articulate clear goals to this end.

3. Reduce barriers and provide regulatory certainty

There is currently uncertainty surrounding two regulatory issues in the development of the clean hydrogen sector: the implementation of clean energy tax credits (addressed in section V), and the jurisdiction over pipelines that would transport hydrogen (addressed in section III).

- Implementation of 45V hydrogen PTC. Until the guidance is finalized, uncertainty in the sector will persist and projects will continue to stall. As things stand now, the clean hydrogen economy is at a virtual standstill. A lot is riding on the shape that the guidance will take, with some developers warning that they might be forced to pull out of projects if the guidance is not revised.

- A more flexible, phased-in approachto the three pillars would boost investor confidence for a burgeoning industry and help accelerate its development. The final 45V guidance should strike the right balance between ensuring that the hydrogen industry develops as cleanly as possible, while allowing the sector to get off the ground. The economics need to work. There is a risk that additional flexibility could mean a higher emissions profile of the nascent hydrogen industry in the short term. At the same time, the clean hydrogen industry is just getting off the ground, and additional flexibility is warranted to achieve economies of scale, speed up learning rates, and drive down costs in the coming decades. As discussed above, lack of flexibility in the three pillars could potentially delay some projects or even render them financially inviable, which would run counter to these goals.

- With regards to incrementality, additional flexibility could look like establishing a phase-in period for the requirement, or allowing an alternative pathway for existing low- or zero-carbon generation resources to play a role in clean hydrogen production. Not permitting hydrogen production with two of the largest sources of baseload, zero-emissions electricity generation that can power electrolyzers around the clock – nuclear and hydropower – to qualify for the credit will substantially impact the amount of clean hydrogen that can be produced, and slow the growth of the industry.

- As for temporal matching, increased flexibility could involve extending the phase-in period until 2030, which is a similar timeline to what the EU has established. It could also mean allowing a certain percentage of a facility’s generation to be exempted from hourly requirements.

- A more flexible, phased-in approachto the three pillars would boost investor confidence for a burgeoning industry and help accelerate its development. The final 45V guidance should strike the right balance between ensuring that the hydrogen industry develops as cleanly as possible, while allowing the sector to get off the ground. The economics need to work. There is a risk that additional flexibility could mean a higher emissions profile of the nascent hydrogen industry in the short term. At the same time, the clean hydrogen industry is just getting off the ground, and additional flexibility is warranted to achieve economies of scale, speed up learning rates, and drive down costs in the coming decades. As discussed above, lack of flexibility in the three pillars could potentially delay some projects or even render them financially inviable, which would run counter to these goals.