Foreword

Citizens for Responsible Energy Solutions (CRES) Forum has long supported an all-of-the-above strategy to reducing greenhouse gas (GHG) emissions in the power sector. As we explore climate change mitigation policies in transportation and in other sectors across the economy, we should extend the same all-of-the-above approach.

The current discussion related to addressing GHG pollution from transportation is heavily concentrated on electrification with little attention given to hybrid vehicles, biofuels, hydrogen, carbon capture, or more efficient fossil fuels or combustion engines. CRES Forum believes this singular focus is misguided. As a conservative organization, we believe a technology neutral approach is most effective at cutting emissions. Moreover, a successful effort will harness the power of the market and innovation to reduce or avoid global emissions – and it will not be applied solely to America.

This paper finds there are many problems with current federal and state policies that suggest electric vehicles (EVs) are the “silver bullet” to addressing global transportation emissions. While we recognize the importance of electrification, we do not share the optimism expressed by the Biden Administration and its proponents on how effective an EV-focused strategy can be. There are many hurdles to increased EV penetration in America and other developed economies, which this paper points out – not to mention the challenges that electrification faces in the developing world.

Importantly, CRES Forum understands there may be other important strategic aims – outside of reducing global emissions – why the federal government might push EVs as the preferred option, such as a manufacturing or industrial policy that is designed to promote the global competitiveness of the U.S. automobile sector. This paper does not examine those goals, but CRES Forum is open to considering them in the future.

– George David Banks, Senior Fellow, CRES Forum

Executive Summary

Transportation emissions represent 14% of global carbon dioxide (CO2) emissions, 45% of which come from ground transportation systems.1 Existing policy focus, as well as analysis, predominantly deem electrification as the primary means of reducing light duty vehicle (LDV) carbon pollution, which has in effect diminished attention to alternative viable emissions reduction pathways. Subsidies, mandates for electric vehicle (EV) adoption, and bans on the sale of new internal combustion engine (ICE) vehicles – all fixtures of the current policy discourse – imply an overly simplistic picture of LDV emission mitigation opportunities that may understate potential barriers to EV adoption at the scale projected in net-zero emission pathways.

In this paper, we note that much of the existing literature on emission mitigation that is used to inform policymakers presumes vehicle electrification is an easy and low-cost abatement opportunity. However, analysis of these studies shows that they do not adequately consider potential constraints to EV adoption, including, but not limited to:

- Mineral scarcity. Multiple studies estimate greater than 100% of global reserves are needed for both lithium and cobalt to meet global EV adoption targets outlined in zero-emission pathways.2

- Rising costs of material inputs. Prominent projections of future EV adoption presume that battery costs will fall, even though recent data as well as conventional economic analysis suggests that lithium prices – without significant technological breakthroughs – will increase and may delay EV cost-parity with internal combustion engine vehicles (ICEVs).3

- Overly optimistic mobility demand expectations. Net-zero emission pathway analyses assume that developing nations will achieve vehicle saturation and satisfy mobility needs with far fewer vehicles per capita than developed nations.4 The Energy Information Administration (EIA) expects that developing nations will only reach one third of the vehicles per capita of developed nations by 2050.5 If projections of future vehicle needs are even 10% too low, an additional 198 million EVs would be needed to reach net-zero emissions.

- Battery replacement needs are not always considered. Prominent net-zero emission pathway analyses assume EVs as equal substitutes to ICEVs in practicality and cost.6 But typically these analyses do not account for battery replacement, which can significantly affect the total cost of vehicle ownership, decisions to retire EVs prematurely, total mineral needs, and the cost of EVs in second-hand markets.

- Heterogeneity of vehicle consumers. Currently, satisfied EV owners in the United States are predominantly wealthy homeowners in developed areas with access to at-home charging and often an ICEV as an alternative or even primary vehicle. However, charging inconvenience has resulted in 18-20% of EV owners reverting to ICEVs,7 and global EV adoption would require that the large number of global households living in communal housing have convenient access to public charging. It is not yet clear to what extent charging inconvenience may deter EV uptake.

In general, these studies implicitly assume technological breakthroughs required for EV battery cost reductions and charging convenience will occur, even though this is uncertain. While we are optimistic that innovation in EV design and batteries will improve efficiency, as well as result in substitutes for strategic minerals and inputs, we are more skeptical that hurdles to achieving the envisioned scale of EV global market penetration can be easily addressed.

Given the array of variables that may stymie or outright prevent EV adoption to the extent that net-zero emission pathway analyses typically prescribe, this paper notes that policymakers should focus on emission mitigation policies more broadly, rather than restrictive policies that overly focus on EV purchases.

In this paper, we note several non-EV opportunities to reduce LDV transportation emissions. These include:

- Reforming subsidies to focus on substitution of ICEV mileage with tech-neutral lower carbon transportation, which could come from EVs, hybrids (HEVs), or other vehicle types. Current policy frameworks presuppose EVs are the least carbon-intensive option.

- A focus on innovation policy for advanced liquid fuels such as advanced biofuels, e-fuels, and solar fuels which can operate with existing infrastructure, and may be more practical for developing nations for whom EV charging infrastructure may be impractical.

- Expanded usage of carbon capture, either for enhanced oil recovery (EOR) or other forms of sequestration, which could reduce the life-cycle emissions of currently used petroleum fuels and allow for emission mitigation from consumers without requiring new vehicle purchases or fueling infrastructure.

Overall, we note that the life-cycle emissions of LDVs are highly sensitive to fuel type and method of fuel production. EVs have emission advantages compared to ICEVs using conventional fuels today8 at 53% lower emissions, but when comparing future low-emission electricity-powered EVs to hydrogen fuel cell vehicles and hybrids utilizing low-carbon fuels, we find that the emission advantage of EVs narrows considerably, with only a 4% advantage over a hybrid powered by advanced biofuels.

Given the array of competing LDV emission abatement opportunities, policymakers should ensure that their policies do not obstruct effective emission mitigation opportunities from the market.

Additionally, an overemphasis on EV adoption as a sole solution to reducing LDV emissions could create national security challenges. Recent analysis noted that EVs are exceptionally dependent on mineral supply chains that are controlled by China, and international security scholars expect Beijing to exploit this advantage to achieve its strategic objectives.9 As we have seen with the Russia-Ukraine War, U.S. and Western climate policymakers should acknowledge the risk posed by a future conflict of interest with China, which could drive a stark shift away from Chinese-controlled EV supply chains. The lesson is that an approach to reducing transportation emissions that emphasizes multiple technology pathways and platforms is in the national interest.

Broadly, we lay out three policy recommendations to reduce LDV emissions that do not rely exclusively on vehicle electrification. They are:

- Replace current EV mandates and subsidies with policies that reward emission abatement instead of EV purchases. This would end subsidizing EVs that are underutilized and/or fail to replace any ICEV emissions, providing certainty that only vehicles that reliably replace polluting travel—pursuant to a lifecycle analysis—are rewarded. The best emission outcomes are achieved when all emission abatement is evaluated agnostically and rewarded equally, but current subsidy structures ignore emission outcomes, instead simply rewarding EV purchases.

- Broaden the potential emission mitigation opportunities that are considered in the transportation sector. California’s Low-Carbon Fuel Standard (LCFS) allows for biofuels produced in other states to count towards compliance, which incentivizes pollution reductions beyond the borders of the policy and on a life-cycle basis. Similarly, any new policies aimed at reducing emissions should allow for the consideration of less costly mitigation measures adopted by fuel producers and passed down to consumers, such as steps to offset emissions through carbon dioxide removal or sequestration.

- Ensure that any environmental provisions of international trade deals focus on life-cycle emissions, rather than vague undefined political priorities. Many EV policies currently incentivize vehicle production in China, which has substantially more emission-intensive manufacturing than in the United States.10 Given the growing interest in merging climate and trade policy, Washington should acknowledge the heterogeneity of emission intensity of producers of vehicles and fuel and develop trade policies that encourage innovation that reward the cleanest producer, which is likely to be American.

This analysis does not assess aspects of U.S. public policy and investments that are focused on producing a stronger domestic auto industry (including its current focus on EVs) for national interest reasons, but only the emissions benefits of such policies. Overall, this paper finds that conventional discourse on mitigating transportation emissions frequently fails to consider challenges to vehicle electrification and highlights that alternative vehicle and fuel mix outcomes in the future can yield comparable, if not greater, emission benefits, particularly if they can compete on a lifecycle emission basis and are deployed as part of a global strategy. Policymakers must accept that there are constraints to their preferred political outcomes, and instead pursue policies that reward emission mitigation in an agnostic manner.

Background

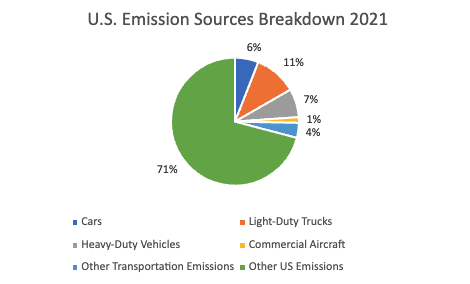

Transportation is a commodity of global importance. The ubiquitous need to move people and goods from one location to another is an essential facilitator of economic activity and growth. The competitive nature of the global economy and relatively low modern-day cost of many commodities is made possible by cost-effective transportation, which enables consumers to purchase goods produced far away. Consequently, transportation as an economic activity offers very high utility and is always in demand. This is evidenced by a steady rise in global vehicle ownership and utilization. The transportation sector contributes a significant portion of global greenhouse gas (GHG) emissions.11 Emissions from planes, trains, automobiles, and other transportation sources account for approximately 7.2 gigatons of carbon dioxide (CO2) annually, 12 comprising nearly 14% of global emissions. 13 In the United States, transportation is the largest economy-wide source of emissions at 27%.14

In general, transportation takes many forms. Motorcycles, cars, SUVs, trucks both heavy and light, aircraft, ships, and all others require energy and are used in some form or another to satisfy mobility demands. Generally, this paper focuses on LDVs, which account for most vehicular demand globally, and are typically defined as passenger vehicles (cars, SUVs, pickup trucks, etc.). For many individuals, LDV use is a part of their daily life, and one of the largest parts of their carbon footprint.15

The majority of the over 1.32 billion cars distributed globally are powered by petroleum fuel-reliant internal combustion engines (ICEs).16 The widespread global adoption and use of LDVs would not have been possible without the availability of relatively low-cost energy dense petroleum fuel sources; a gallon of gasoline has roughly 33 times the energy density of a 1-kilowatt hour (kWh) battery.17 However, the operational efficiency of an internal combustion engine (ICE) lags in comparison to an electric motor at 12-30% compared to 77%, respectively.18 Despite the inefficiencies of ICEs, a conventional car has roughly double the range from a single tank of gasoline as an EV has for a single charge.19 Additionally, the high energy content of petroleum fuels means that even relatively simple and inefficient ICEs can function cost-efficiently. In 2018, mechanized land transportation modes ranging from two-wheel passenger vehicles to buses comprised the largest share of global transportation CO2 emissions at 45.1%.20

Petroleum fuels are also abundant globally with a relatively large number of producers, which helps create a competitive market. It should be caveated, however, that a large share of global crude oil production, an estimated 75% in 2010, is controlled by state-owned enterprises, which may be directed to adjust production or prices for political purposes.21 A prominent recent example is OPEC cooperating with Russia and other oil producers (OPEC+) to limit production as a means of artificially inflating oil prices through market manipulation.22 Generally, however, petroleum fuels are considered to be affordable and abundant globally, as evidenced by their widespread use.

Petroleum fuel consumption, though, levies externalities. Air pollution produced by using petroleum products increase societal morbidity and mortality risk.23 In this paper, we focus on the production and release of GHGs associated with petroleum use. A gallon of petroleum-derived gasoline, when combusted, will emit 0.009 metric tons of carbon dioxide,24 thus an average LDV with an annual mileage of 11,500 miles would produce 4.6 metric tons of CO2.25 In addition to carbon dioxide, other GHGs produced in the transportation sector—owing to the use of petroleum fuel—are methane and nitrous oxide.26

Efforts to reduce transportation GHG emissions have seen only limited success so far. This reflects the lack of “cleaner” mechanized substitutes relative to conventional passenger vehicles, coupled with relatively easy access to energy-dense liquid petroleum fuels. Although the cost of petroleum fuels has increased markedly since 2021, even at relatively high prices they remain in demand due to the inelastic nature of transportation needs. Moreover, significant shares of transportation activity have high utility to consumers and cannot be easily forgone. Consequently, petroleum fuel consumption is anticipated to remain high, and policymakers should not expect a near-term end to the use of petroleum fuels.28

Outside the United States, some countries are adopting policies that prohibit the sale of vehicles that rely on gasoline. In Europe, for example, there is a requirement that prohibits the sale of combustion engine vehicles by 2035, implemented via the European Union.29 The rule, though, does allow for combustion engines that utilize carbon-neutral fuels.30 Norway, the United Kingdom, France, Spain, and other countries already have similar prohibitions on future combustion engine vehicle sales.31

Within the United States, the Biden administration has proposed similar regulation to what is being taken up in Europe. In April of 2023, the Biden administration proposed new zero emission vehicle regulation that it is expected would require two thirds of passenger car sales to be electric and one quarter of heavy truck sales to be electric by 2032.32

Electric vehicles present notable advantages over their fossil fuel-powered counterparts: improved fuel economy, absence of fossil fuel dependence, and most relevant to climate-change related discourse, zero tailpipe emissions.33 Consequently, policymakers in many parts of the world have increasingly favored programs that incentivize EV adoption. Global sales of electric cars in 2020 grew 43% compared to 2019, to reach 3.2 million units, accounting for 4.2% of global new car sales.34

The International Energy Agency’s (IEA) Net-Zero Emission scenario (NZE) estimated that by 2050, 86% of cars, 79% of buses, 84% of vans, and 59% of heavy trucks would have to be electric to reach net-zero emissions globally.35 Similarly, the International Renewable Energy Agency (IRENA) estimated in their net-zero by 2050 report that 88% of light-duty vehicles (LDVs) and 70% of heavy-duty vehicles (HDVs) would have to be electric by 2050.36 A meta-analysis of 177 net-zero emission scenarios noted that, “In addition to renewable and net-zero targets, ‘electrify everything’ has become an explicit policy goal in a growing number of places, particularly regarding heating and cooking in the residential and commercial sectors and light-duty transportation.”37

Despite EVs’ apparent advantages in mitigating pollution over ICEVs, as well as policy support for greater EV adoption, ICEVs still retain key advantages that inhibit market transition. ICEVs have few range constraints due to the combination of energy dense liquid fuels and the commonality of refueling stations. EVs can substitute for many typical uses of an ICEV, but long recharging times can create range constraints that hold back consumers.38 Alternative fuel vehicles, like fuel cell electric vehicles (FCEVs), are also limited by fuel access currently, though FCEVs hold promise for some companies, like Toyota, which expect that their advantages of convenience will appeal to consumers more than EVs.39 Public transportation works well in densely populated areas but struggles in more rural areas where limited ridership can only support a small number of routes. Conventional biofuels require significant amounts of arable land, creating a constraint to widespread conventional biofuel substitution of petroleum fuels.40 More efficient hybrid electric vehicles (HEVs) can reduce overall petroleum use, but still rely on petroleum fuels and are less politically favored since they may not be able to lower LDV emissions to the same degree as EVs.

For policy analysts, transportation emissions represent a significant challenge. Analysts attempting to plan “transition scenarios” or “net zero emission scenarios” are tasked with envisioning pathways that eliminate LDV emissions. With few alternatives to ICEVs in usage today, analysts must rely on known solutions. Due to the technological maturity of EVs, they are frequently favored in such analysis. Prominent transition scenarios like those prepared by IRENA and the IEA assume significant, rapid, global replacement of ICEVs with EVs as a pathway to decarbonization. However, these analyses, while timely, do not consider potential constraints to global EV adoption, and as a result may give a false impression that there is minimal policy need for developing non-EV transportation abatement opportunities.

This analysis highlights the current state of global LDV emissions, factors that influence those emissions, and policy alternatives that may produce environmental benefits that are more economically efficient than existing policies.

Potential Constraints to Global EV Adoption Not Considered in Existing Policy Analysis

Mineral Scarcity

EVs are minerally more intensive than ICEVs. A typical ICEV requires 34 kilograms of select minerals (excluding steel and aluminum), whereas an EV requires 207 kilograms.41 Additionally, EV battery composition typically requires significant amounts of lithium and cobalt. A report from Citizens for Responsible Energy Solutions Forum noted that the global demand for lithium and cobalt needed to reach the EV targets outlined by the IEA’s NZE and other scenarios may exceed global reserves.42 Three separate studies estimated that the amount of lithium needed, relative to global reserves, would be 214%, 128%, and 124%.43 For cobalt, the requisite amounts were 423%, 190%, and 129% of global reserves.44 Even nickel, which can sometimes substitute for other battery materials, faced similar constraints with two of the three studies estimating over 100% of global reserves needed.45

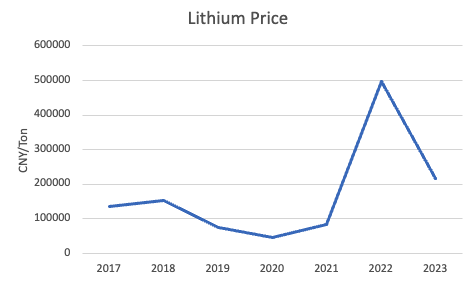

This suggests that to meet EV demand outlined in net-zero emission scenarios, either new sources of both lithium and cobalt that are economically viable are found or breakthrough innovation develops substitutes for those minerals or significantly reduces their intensity in use. Forecasts for high mineral demand, combined with constrained supply, suggest an upward pressure on prices. Current estimates suggest that by 2030, 95% of lithium demand will be for batteries compared to less than 30% in 2015;46 this is likely to increase prices and the cost of EV batteries and cars.47 The IRENA 1.5 Degree report, for example, estimates that EV demand will cause lithium prices to increase to 500% of present-day values.48

In recent years, lithium has experienced marked increases and swings in prices. In 2019, lithium was around 76,500 Chinese Yuan (CNY) per ton, but by November 2022 had increased to 597,500 CNY/Ton, a sevenfold increase.49 Since the November peak, lithium prices have fallen, down to roughly 300,000 CNY/ton as of early June 2023.50 Ironically, though, this fall is not because of improvements in lithium production, but because of slower than expected EV demand.51 Should EV demand increase to the levels that net-zero pathway scenarios would suggest is required, lithium prices would certainly increase in response to rising demand.

Despite overall elevated lithium prices, battery costs have fallen, with lithium-ion battery prices down 89% since 2010.53 Conventional thinking would suggest a continuation of this trend; existing net-zero emissions scenarios assume that lithium battery costs will decline. While current prices average $132 per kilowatt-hour54 (kWh), the IEA’s NZE report indicates battery costs will fall to $55-80/kWh.55 Similarly, IRENA’s report estimated EV battery costs of $85/kWh,56 and a recent report from Princeton University forecast those costs to decline to $60/kWh.57

However, historical reductions in battery prices largely reflect falling “soft costs” of battery production (i.e., production costs, staff costs, economies of scale, etc.) rather than mineral demand/availability. A recent EV teardown noted that mineral costs—owing to higher demand—are increasing as a share of overall production costs thereby delaying cost-parity with ICEVs.58 In 2022, Tesla raised the price of its vehicles by $2,500 to $6,000 depending on model, in part because of supply chain disruptions caused by the Russian invasion of Ukraine.59 Consequently, we expect higher demand of lithium, coupled with limited lithium supply, is likely to raise the price of EV batteries. This is problematic as low battery costs are essential for EVs to reach cost parity with ICEVs, given that batteries are one of the most expensive components of an EV.

The dynamics of rising lithium demand increasing EV prices could be mitigated by increased lithium production. Recent developments in the U.S. mining sector have shown that the United States may have greater potential for lithium production than initially expected.60 The benefits of this capacity in reducing the costs of EVs, though, will require the administration to approve permits for more mineral extraction, which is not always guaranteed.61

Importantly, consumers in developing nations, which are the fastest growing source of transportation emissions,62 are more price sensitive owing to lower purchasing power. One cannot buy a vehicle that they cannot afford, and the GDP per capita in developing nations compared to developed ones is roughly one fourth.63 Should mineral scarcity increase EV prices to a point where price parity between EVs and ICEVs is delayed, the high level of global EV adoption that net-zero emission scenarios are dependent upon may never be reached.

Global Vehicle Demand May Exceed Expectations of Net-Zero Scenarios

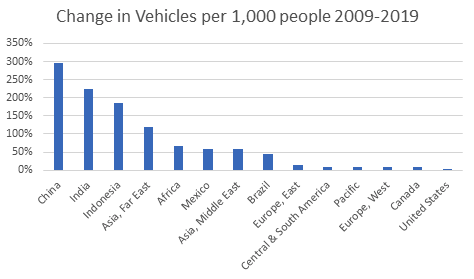

Currently, there are roughly 1.31 billion LDVs in use globally.64 This figure is projected to increase significantly over the next few decades. It should be noted that on a vehicle per capita basis, developed nations represent a predominantly higher level of vehicular usage. In 2019, the United States had 842 vehicles per 1,000 people, and Western Europe had 629 vehicles per 1,000 people.65 Africa, meanwhile, had only 41 vehicles per 1,000 people.

Vehicles per Thousand People in Selected Countries/Regions 2009 and 2019

| Country/Region | 2009 | 2019 |

| Africa | 25 | 41 |

| Asia, Far East | 58 | 126 |

| Asia, Middle East | 101 | 159 |

| Brazil | 149 | 216 |

| Canada | 621 | 669 |

| Central & South America | 170 | 185 |

| China | 46 | 183 |

| Europe, East | 364 | 418 |

| Europe, West | 583 | 629 |

| India | 14 | 47 |

| Indonesia | 36 | 103 |

| Mexico | 225 | 356 |

| Pacific | 561 | 608 |

| United States | 829 | 842 |

The IEA’s NZE and IRENA estimate that LDV demand will rise to 2 billion by 2050 whereas the Energy Information Administration (EIA) projects LDV demand by 2050 to approach 2.2 billion.68,69,70 However, these figures may underestimate future LDV demand as they largely assume stagnant vehicle ownership rates and heterogeneity in vehicle demand between developed and developing nations.71 The latter assumption is particularly relevant because the EIA estimates an 88% increase in vehicles per capita in the developing world.72 However, in rapidly developing nations, the growth of vehicle demand has been much more rapid. From 2009 to 2019, vehicles per 1,000 people grew by 295% in China, 225% in India, and 186% in Indonesia. Heterogeneity in LDV demand across markets is problematic as existing net-zero emission scenarios assume slow demand growth in developing nations—an assumption that, based on existing data, may lead to overly optimistic emissions reductions projections.

The total number of future EVs required to meet decarbonization targets is highly sensitive to overall vehicle demand. If the EIA’s estimation is even 10% too low, this would necessitate adoption of approximately 198 million more EVs to achieve net-zero emissions by 2050.74

The level of total vehicle adoption globally is dependent on several factors. These include economic confidence, mobility demand, economic growth potential, and infrastructure availability. Also important is the level of “vehicle saturation” – the point at which the market has enough vehicles to satisfy mobility demands. Developed economies have relatively stagnant growth potential for total vehicle demand; vehicles per 1,000 people in the United States are still below its 2007 peak.75 Developing economies, by contrast, are not yet at levels of saturation, which is evidenced by their projected growth in liquid fuel demand. 76 Given this uncertainty, generating definitive estimates of total global demand for automobility requires speculation that may not hold true.

Battery Replacement

A potential source of additional stress on mineral supplies needed for EV production that is rarely considered in net-zero emission projections is the need for battery replacement. EV battery cells degrade over time, due to chemical processes that prevent or reduce battery cells from holding a charge.77 The precise mechanics of this process and how to prevent it is still being researched. However, known stressors to battery cell anodes include heat (which is involved in charging the battery),78 state of charge (how long the battery cell is holding a charge),79 repeated discharge cycles,80 and age.81 The process of battery degradation is not necessarily linear. Rapid degradation may occur early in a battery life and subsequently level off before continuous decline.82

EV use necessitates battery replacement when a battery pack is no longer able to hold a charge that promises a range envisioned or guaranteed to owners as a condition of purchase or ownership. Current estimates suggest that an EV battery pack will, subject to certain conditions, last eight years, following which a replacement may be required.83

The need for replacement batteries and the associated additional pressure on mineral stock, as well as total vehicle ownership cost, is often overlooked in current EV versus ICEV comparisons. Both the IEA NZE and the IRENA 1.5 report assume EVs to be interchangeable with ICEVs for vehicular needs, without considering if battery replacement needs could affect EV market uptake.84

The material implications of battery replacement are significant. One study estimating total lithium needs for global decarbonization assumed EV use for 15 years, which would require 95% of global lithium reserves with recycling and without battery replacement. 85 However, that number changes drastically to 238% of global lithium reserves with battery replacement and no recycling.86 The breadth of discrepancy in these figures shows that potential need for battery replacement significantly alters the dynamics of total mineral requirements, life-cycle emissions of an EV, and, invariably, the total cost of ownership.

The potential need for battery replacement would also affect EVs’ ability to reduce global emissions. EVs and ICEVs boast different emissions profiles, subject to manufacturing and use considerations. An EV has low per-mile emissions, but high manufacturing emissions. Conversely, an ICEV has low manufacturing emissions, and high per-mile emissions. The battery of a typical EV used to power an LDV represents 18% of its life-cycle emissions.87 Potentially requiring two batteries for an EV alters its emission advantage over ICEVs. Using IEA life cycle estimates, the emission advantage of an EV over an ICEV would go from 49-52% without battery replacement to 40-46% with battery replacement.88 To put this in perspective, the IEA’s NZE estimates 2 billion EV cars and light trucks deployed by 2050 with each having between 2.6 and 4 metric tons of CO2 equivalent associated with battery manufacturing.89 If the emissions associated with battery manufacturing of these vehicles was doubled (owing to an increased requisite battery requirement), this would result in an additional cumulative 5.2 to 8 billion metric tons of CO2 equivalent emitted.90 Recycling could bring this figure down significantly, although the extent to which is not yet known.91

In addition to emissions impact considerations, the cost of battery replacement also warrants scrutiny. An EV’s battery is a significant share of an EV’s cost, and a battery replacement can cost as low as $2,500 – $16,000 for a low-end EV like a BMW i3, or $15,799 – $23,443 for higher-end EVs like Teslas.92,93 Under some conditions, battery replacement may be covered under warranty at the purchase of a new EV. However, for EV owners who may be ineligible for a warranty-covered battery replacement, such as those who have purchased EVs on the secondhand market or owners who retain their vehicles beyond the warranty period, the potential for added expenditure may dissuade EV adoption.

EV battery replacement may also reduce the total lifetime of the asset. If an EV requires a battery replacement at years 10-12, but the vehicle’s envisioned total lifetime is 15 years (an ICEVs average age is about 12 years),94 then the EV may be retired from vehicle stock prematurely owing to cost of the repair. There may be several reasons why an EV owner may choose to retire the vehicle well before its expected end of life in addition to costly battery replacements. Vehicle purchase decisions are influenced heavily by the vehicle’s reliability and its ability to satisfy mobility needs. However, consumers also make purchase choices based on non-mobility needs, such as car features, cargo space, current family size, safety, etc. When vehicle replacement opportunities are presented, owners can switch adoption to vehicles that meet evolving preferences. This allows for vehicles to feed into a secondhand market, but battery replacement needs may introduce new dynamics for secondhand EVs.

Consumers in the market for used EVs may be unwilling to buy an EV in need of a battery replacement as this may, depending on battery size, significantly increase the cost of second-hand EV procurement. Conversely, first-hand EV buyers face a similar issue should battery replacement be required prior to reselling an EV. This potential loss of value from the resale of an EV due to battery replacement can affect the total cost of EV ownership and affect its overall economics compared to an ICEV.

Additionally, prominent research on the maintenance costs of vehicle ownership comparing EVs and ICEVs has not always factored in battery replacement. Research from Argonne National Laboratory estimated that when considering maintenance costs, an ICEV costs $0.10 per mile to operate, and an EV cost $0.06 per mile.95 The study did not consider battery replacements, assuming that the costs would be equal to an ICEV requiring a new powertrain later in life.96 This assumption of equivalence in repair costs seems faulty, however, as engine replacements are typically required after 200,000 miles,97 whereas an EV would only have about 135,000 miles on average after 10 years and needing a battery replacement.98 Additionally, engine replacements cost $4,000-10,000,99 whereas battery replacement can cost up to $23,000. Had Argonne considered battery replacement in their study, the cost per mile of operating an EV would be between $0.01 and $0.12 higher, likely making the EV maintenance more expensive.100 The potential for battery replacements to delay EV’s cost competitiveness compared to ICEVs has not been adequately represented in existing EV discourse and associated policy discussions.

Potential alternatives exist to battery ownership that might spare EV owners the potential cost of battery replacement. For example, Tesla in 2013 promoted a “battery swap” program that would replace EV batteries at an automated station faster than gasoline refueling.101 The hope was that this could address the issue of range anxiety for long distance travel with battery swap stations in place of “fast-charging” stations on highways. However, the economics of forfeiting outright battery ownership with a battery ‘renting’ model remains unclear and there is little publicly available data to suggest the approach is a viable solution to existing concerns surrounding battery longevity. The only attempt at such a program in the United States was Tesla’s, which was abandoned due to its high cost.102

By ignoring battery replacement requirements of EVs, policymakers may overestimate the emission benefits from EVs and underestimate the economic consequences of forced EV adoption through mandates, as well as the security impacts of increased mineral needs.

Heterogeneity of Vehicle Consumers

The typical EV owner is a male, aged 40-55, with an annual household income above $100,000.103 For reference, only about 31% of U.S. households earn over $100,000 per year.104 Over 80% of EV (re)charging happens at home, where EV owners have set up their own chargers and many of these drivers can also fill up their batteries at their workplaces.105,106 The type of household that owns an ICEV, though, is much more diverse, with 92% of U.S. households reporting access to at least one vehicle.107 In the United States, EVs are three times more likely to be owned by homeowners rather than renters, signaling that charging convenience may play a significant role in EV purchasing decisions.108 The perceived inconvenience of recharging is cited as a reason for adopting ICEVs over EVs. Recent analysis has found that 18% of EV owners and 20% of PHEV owners revert to ICEVs, citing charging inconvenience as the primary reason for no longer using an EV or PHEV.109 A journalist traveling from New Orleans to Chicago using an EV noted that she spent more time charging the car than sleeping, referencing numerous challenges to finding adequate fast charging in rural areas.110

The perceived convenience of at-home charging infrastructure over communal and/or public alternatives has significant implications, particularly in foreign markets. In the United States, 17% of the population lives in apartments or condominiums,111 compared to 36% internationally, which underscores the challenge of global EV adoption, particularly in developing economies.112

Charging convenience is likely to play a significant role in EV purchasing decisions. Charging an EV can take between 20-30 minutes if it is rapid or up to 21 hours if it is slow, which is expected on average to take around 8 hours from zero to full.113 If public charging is needed, many potential EV consumers may be unwilling to transition due to the required time. The median range of an EV is 234 miles,114 and in the United States, weekly vehicle miles traveled averages 274 miles.115 EV owners without access to at-home charging will likely have to make special excursions for charging at least once a week, and these are likely to last around 30 minutes or longer. Even that assumption may be overly optimistic, as currently 88% of publicly available EV charging are “level 2,” which takes 4 to 10 hours.116

Better technology may reduce charging times, but also can carry a risk. Faster refueling requires more voltage, which raises temperatures. High temperatures can exacerbate battery degradation, potentially accelerating needs for battery replacement.117 Although the magnitude of battery aging owing to rapid charging is currently unclear,118 what is apparent is that widespread public EV charging is unlikely to reach similar convenience to gasoline refueling. Rapid EV charging offers a means of tempering this inconvenience but may do so at a cost to battery life.

Additionally, EV refueling reliability warrants scrutiny. A recent study found that over 20% of EV chargers in the San Francisco region of California are broken.119 It is unclear at this point if EV charging encounters a unique reliability concern compared to fuel pumps, but it should be noted that EV adoption projections typically do not consider refueling unavailability as a constraint to EV adoption.

These considerations warrant attention and appreciation by policymakers. Consumer demand and preferences are heterogeneous and influenced by various factors including, but not limited to, charging access and opportunity cost (i.e., if EV owners are giving up valuable time to charging their cars), as well as evolving vehicular needs.

EV Constraints May Not be Adequately Considered in Existing Policy Discourse.

Existing global EV adoption estimates presume an easy transition away from ICEVs, high levels of vehicle substitutability, and minimal expectations of resource constraints. For example, the IRENA 1.5 report assumes that its EV replacement of LDV estimate is viable if battery costs continue to fall as quickly as they have in the past, but the same report notes that lithium prices for batteries may increase fivefold from current levels.120 The IEA NZE report similarly assumes that given past trends, EVs will be cost-competitive with ICEVs, even though they estimate a more than 30-fold increase in demand for minerals in the future.121 Additionally the Net-Zero America Report from Princeton University also assumed that trends of EV cost declines in the past will continue, underpinning assumptions of future EV deployment.122 From a policy analysis perspective, this is problematic as EV-dependent net-zero emission scenarios rely entirely on assumptions that EVs will be equal to or lower cost than ICEVs and almost perfectly substitutable.

One effect of possibly overly optimistic energy transition analysis is that policymakers have favored EVs over alternative methods of transportation decarbonization. Currently, 45 states plus the District of Columbia offer some type of incentives for EVs and/or PHEVs.123 At the federal level, passage of the IRA extended – and for certain automakers – expanded availability of the national $7,500 EV subsidy.124 The current administration claims these subsidies will achieve the desired EV targets.125 Clearly, there is a prominent expectation among policymakers that EV adoption, when facilitated by generous incentives, will be an easy and natural path forward for reducing transportation emissions.

This outcome – specifically where the IRA is concerned – may run into difficulties for two reasons. Firstly, full subsidy realization for consumers depends on EVs meeting specific critical mineral and component requirements, the stringency of which increases over time. These requirements are so stringent that the IRA ends (rather than expands) credits for about 70% of the 72 EV models that were previously eligible. 126

More broadly, we emphasize that a policy approach that is primarily focused on EV adoption, particularly one facilitated by policies like consumer subsidies or the proposed zero emission vehicle mandate, may have unintended consequences for overall GHG emission mitigation. For example, current policies primarily subsidize electric or partially electric vehicles with no lifecycle analysis requirement. By contrast, hybrids also have emission advantages over ICEVs, estimated by the Department of Energy to be 45% lower annual emissions than gasoline-powered cars, but receive minimal policy preferences.127 Hybrids also have advantages over EVs in terms of deployment as they do not face constraints related to batteries or charging access. The policy response for vehicle decarbonization has not focused on supplanting or reducing emissions, but instead on deployment of vehicles preferred by policymakers.

The effect of the existing policy is that EV ownership is rewarded regardless of emission mitigation. While the IRA implemented some new policies to increase support for non-EV transportation emission mitigation, such as a clean fuel tax credit,128 the overall policy structure in the United States that emphasizes EV adoption, infrastructure, and ICEV bans may be unwittingly occluding competing emission mitigation opportunities from the market.

In effect, what we see in policy is a high preference for EV subsidy and mandate, which is likely due to the considerable focus electrification receives in policy analysis, and only minimal policy support or interest in alternative transportation decarbonization opportunities. This dynamic is evident when comparing policies of EVs and hybrid vehicles. While hybrid vehicles do not conform to energy transition scenarios due to their higher emissions compared to EVs, their opportunities for immediate reductions in transportation emissions are largely ignored.

U.S. Geopolitical and National Security Concerns

Although a distant memory for many Americans, U.S. crude import dependence created significant vulnerabilities that harmed consumers and compromised the country’s freedom to conduct foreign policy.129 In 1973, the Organization of Petroleum Exporting Countries (OPEC) – a coalition composed largely of small economies – imposed an embargo on the United States because of Washington’s support for Israel during the Yom Kippur war, quadrupling the price of oil and creating long gas lines and shortages at home.130

The oil crises of the 1970s continue to influence domestic U.S. energy policy, owing to continued reliance on petroleum fuels, and the fact that oil is a globally traded commodity (meaning events that disrupt foreign supply still impact domestic prices). As part of bipartisan policy beginning with the Nixon administration and lasting through the beginning of the Obama administration, the United States has sought to reduce its oil imports and the influence of foreign oil producers on domestic prices. Increased domestic production of oil was a major priority of past administrations, and recently the United States has gone from being a net importer of petroleum products to a net exporter, reducing the vulnerability of domestic energy markets to the influence of OPEC and other foreign suppliers.131

While U.S. energy security risks have been lessened, policymakers are increasingly concerned about the country’s broader supply chain vulnerabilities, particularly as they pertain to China, and how those could impact national interests, including the future of U.S. energy security. At the time of the 1973 embargo, OPEC nations accounted for 85% of U.S. crude oil imports.132 Today, China supplies 80% of U.S. rare earth imports133 and is the dominant supplier for 21 of the recognized critical minerals in the United States.134 Domestic EV mandates – with current technology requirements dependent on Chinese supply chains – would rely on Beijing’s state-owned enterprises to supply lithium and cobalt,135 setting up a potential scenario that could be similar to previous U.S. oil dependence on the roughly dozen OPEC members.

These concerns are not without cause. China has expressed its willingness to use its control of these related supply chains to punish rivals – as its government has in the past embargoed exports of rare earth elements (REEs) to Japan to gain leverage in international disputes.136 Should the United States and its allies adopt EV mandates, supply chain vulnerabilities would create further opportunities for China to exploit as part of its strategic efforts to expand its own influence and power.137 Despite their increasing acknowledgment of this risk, nonetheless, many U.S. policymakers are pushing to restrict the sale of new ICEVs—ostensibly to increase U.S. national security and reduce GHG emissions.138

A policy that restricts ICEVs to improve energy security makes sense in some major economies, particularly in the case of the European Union and Japan – both of which import close to 100% of their crude oil.139 In those cases, their high dependence on foreign energy suppliers means a transition to EVs significantly improves energy security and lessens the influence of OPEC, Russia, Iran and other oil producers. However, U.S. policymakers should appreciate that while promotion of EVs improves energy security in Europe and Japan, these policies have less if any energy security benefit in the United States, owing to it being a large domestic producer of petroleum fuels and reliant on foreign producers for minerals needed for EV production. Additionally, because the United States is a major oil producer, it is in a strong position to use its energy resources to not only improve global economic security but to reduce global GHG emissions related to transportation.

U.S. policymakers should recognize that most low-income countries, particularly ones that lack power generation infrastructure, are not in the same position to electrify transportation. Related emissions reduction strategies that are typically discussed in developed economies are not replicable at the same scale in developing economies. Thus, cleaner, more efficient fossil fuels that take advantage of existing vehicle fleets and energy infrastructure in developing markets can play an important role in achieving more immediate emissions avoidances and reductions. Essentially, if the United States is able to reduce the lifecycle emission profile of its oil production, then U.S. petroleum products could be exported to regions where vehicle electrification may not be an option, creating an opportunity to lower transportation emission intensity at a lower economic cost.

U.S. policymakers should also expect that some developed countries with aggressive EV plans may temper their policies as they encounter potential constraints to supply and deployment. Foreign governments are unlikely to maintain policies that would worsen their own economic and energy security. If China commits aggressive acts against Taiwan, for example, policymakers should expect to see countries shift away from pathways that heavily rely on Chinese supply chains, including EVs and the solar power sector, which may result in even countries committed to decarbonizing their transportation sectors continuing to consume petroleum fuels. While renewable and EV technologies are unlikely to be abandoned, we should expect that countries valuing energy security would probably pursue a variety of energy diversification and emission mitigation opportunities in transportation.

Non-EV Opportunities to Reduce Emissions

While emission reduction policies have predominantly focused on EVs, there are substantial opportunities to achieve the same outcome using pathways that are less dependent on EV uptake and may yield similar, if not superior, emissions benefits. This is particularly relevant for developing nations where constraints on EV adoption include, but are not limited to, charging infrastructure limitations, vehicle costs, electricity reliability, and more. Currently, 759 million people are still without access to electricity globally.140 This constraint alone suggests that global EV adoption as envisioned in contemporary transition analysis is challenging. Consequently, it would be pragmatic for policymakers to consider policies that allow for an array of potential transportation decarbonization opportunities that do not face the same constraints as EV adoption.

Importantly, public policy initiatives, that focus on subsidies and mandates that are specific to EVs or PHEVs, are themselves ironic barriers to the advancement of alternative emission abatement opportunities. Because such a policy structure rewards EV adoption rather than realized emission mitigation, innovators would be directed to focus on EV-related innovation and may ignore alternate emission reductions opportunities that either exclude EVs or necessitate a different EV adoption approach.

Below are examples of non-EV related opportunities to reduce transportation emissions that are not often considered in analysis and policy design.

Reform Subsidies to Focus on Vehicle Utilization

Recent research on EV adoption has found that emission abatement potential is highly sensitive to the vehicle’s overall utilization and substitution of ICEV travel.141 If an EV is purchased but relegated to non-primary vehicle use, it yields a lower emissions benefit. Research on EV utilization has found that many EV owners use their EVs as secondary vehicles.142 By consequence, these vehicles are driven less than the primary vehicle, namely an ICEV. As a result, the expected emission benefits of the EV are exaggerated since they may not be replacing enough ICEV miles to have a life-cycle emission advantage over an ICEV.

Research on EV utilization found that, for a typical household, an EV as a primary new vehicle would need to be driven at least 28,069 miles to have an emission benefit over an ICEV, and as a secondary vehicle replacing an ICEV would need to be driven at least 68,160 miles.143 Furthermore, total emission benefit is relative to the full number of miles replaced, so an EV that is driven only barely above 28,069 miles still delivers far less emission benefit than one that fully substitutes for an ICEV’s lifetime mileage (around 170,000 miles).144

These findings warrant consideration. Simply subsidizing EV purchases does not in and of itself produce any emissions benefit. Rather, policymakers concerned about emissions reductions via subsidies should reform programs so that only vehicles that adequately substitute ICEV miles driven should be eligible for public support. A taxi powered by an electrified powertrain, for example, would deliver far more benefit than a wealthy household’s second vehicle being an EV. Similarly, a highly utilized hybrid substituting for an ICEV can deliver greater emission abatement than a less-utilized EV that only partially substitutes ICEV use.

Consequently, any subsidy policy that is implemented should emphasize measurable emissions mitigation targets instead of focusing solely on vehicle sales. Only EVs or PHEVs that are adequately utilized should—given limited government resources—be eligible for subsidy. Such a system could also acknowledge the benefits that other vehicle types, such as hybrids, have over conventional vehicles in abating emissions.

Consider the Innovation Needs of Advanced Fuels

Significant emission abatement in land transportation—absent reliance on EVs—may also be realized using “drop-in” replacement fuels and/or other advanced liquids. These are synthetic combustible fuels close enough in chemical composition to existing fuels that allow them to often operate in existing engines, or at least with engines producible with existing technology. Drop-in replacement and other liquid fuels can utilize existing infrastructure and do not require behavioral transitions in mobility to the same extent that EVs would. There are several potential ways of producing drop-in replacements that have been demonstrated to date, most of which are not produced at large scale currently, with the exception of renewable fuels.

The most common type of drop-in replacement fuels available today are renewable, such as ethanol, biodiesel, and renewable diesel. Conventional ethanol, which is produced from distilling corn into alcohol, comprises about 10% of fuel pump sales145 and has been blended with conventional gasoline in significant volumes since the Energy Independence and Security Act of 2007.146 Typical vehicles are not designed to utilize high blends of ethanol, although “flex-fuel” vehicles can use fuels that are up to 85% ethanol.

Conventional corn-based ethanol has limitations though. Ethanol’s life-cycle emissions is still being debated, and Argonne National Laboratory estimates ethanol to have an advantage over conventional gasoline by 40%,147 while a 2022 study found the opposite – a 24% higher life-cycle emissions greater than gasoline.148 A major source of discrepancy in these estimates is consideration of alternative land-use if not utilized for crops, with some analysts disputing estimates that ethanol would be higher emissions than gasoline for having unrealistic expectations of alternative land use.149 Emissions from conventional ethanol, nevertheless, could be significantly reduced through the utilization of carbon capture and storage (CCS) technology. It is estimated that CCS could reduce life-cycle emissions from ethanol by 40%.150 Improvements to the life-cycle emissions of ethanol could be impactful for transportation emissions, especially abroad where alternative fuels may not be readily available; the U.S. exports significant volumes of ethanol with a record of 1.7 billion gallons in 2018.151

A challenge to ethanol scalability, however, is that a significant volume of corn is required for production, demanding 40.5% of U.S. corn grain production and 25% of production acreage in 2011, though efficiency is improving, and acreage needs are expected to fall to 11-19% by 2026.152 Even though there is potential for emission abatement, policies that impose mandates for ethanol consumption—such as the renewable fuel standard—have adverse effects on food prices due to the increased consumption of cropland for transportation fuel.153

Lower emissions than ethanol, however, are other biofuels and renewable diesel. It is estimated that renewable diesel (produced from soybean oil, canola oil, animal fats, vegetable oils, etc.) is up to 86% lower GHG emissions than petroleum diesel.154 Renewable diesel functions well as a drop-in replacement fuel because it is chemically identical to petroleum diesel; no new vehicles or technology is needed for it to achieve immediate emission abatement.155 Current renewable diesel production capacity in the United States is growing rapidly, already having reached 1.9 billion gallons per year156 and expected to reach up to 5.1 billion gallons per year by the end of 2024.157

A major impediment to the scalability of biofuels to meet global transportation needs, nonetheless, is their reliance on food products as well as their land intensity.158 Some fuels, like renewable diesel, can be produced from waste products, but a potentially more impactful source of biofuel would be from products that have no competing uses at all. “Advanced biofuels,” which are biofuels made from inedible plant matter, have been of interest for their potential scalability. Cellulosic biofuel, for example, is estimated to have 88-108% lower emissions than gasoline.159 But, despite their emission advantages advanced biofuels have been slow to scale, stymied by high production costs and scarcity of feedstocks.160

There is still optimism though that advanced biofuels can be a plentiful source of liquid transportation fuel in the future.161 The potential scalability of advanced biofuels is highly uncertain, nonetheless, and IRENA’s estimated potential energy content of non-food energy crops by 2050 is between 0 and 700 exajoules, while the Intergovernmental Panel on Climate Change estimates the potential to be at least 100 exajoules by 2050.162 For context, the EIA projects global transportation energy demand in 2050 to be 156 quadrillion Btu,163 which is roughly 165 exajoules. In theory, advanced biofuels could satisfy global transportation needs, but it should be noted that in practice advanced biofuels have not succeeded in the market as hoped,164 and it is not clear how cost-competitive advanced biofuels would be with EVs.

In net-zero analyses renewable fuels often play a minimal role. The IEA’s NZE considers them as mostly relevant for heavy duty transportation, owing to their greater energy density than electricity.165 The IRNEA 1.5 report favors EVs over renewable fuels due to an expectation that renewable fuels will be too expensive compared to alternatives166—though as we noted above the IRENA and IEA studies did not consider many constraints that could impede EV cost reduction. Currently, utilized renewable fuels are roughly comparable in price to fossil fuels,167 although if used for broader decarbonization their price would be affected by suppliers’ ability to meet demand, which is unclear at this point.

Aside from renewable fuels, a potential drop-in replacement fuel is the potential for net-zero carbon liquid fuels from processes like “power-to-liquid” (PtL), which is a process whereby CO2 can be captured from the atmosphere and then electrolyzed into liquid fuel. When powered with zero emission electricity, this process yields net-zero CO2 liquid fuels that are typically called “e-fuels.”168 The scalability of e-fuels, nonetheless, remains unaffirmed as is their cost-competitiveness.169 However, some researchers believe that utilizing more concentrated sources of CO2—such as from carbon capture—as well as better electrolyzing processes could significantly improve the potential of e-fuel production.170 Porsche commenced operation of a new e-fuel facility in late-2022, hoping that by pioneering the fuel they can show how conventional vehicles can become nearly carbon-neutral.171

The primary argument against e-fuels is that the energy intensity of their production is much higher than conventional electricity, requiring close to five times as much energy as the electricity for an EV.172 But it should be noted that transferring energy from electricity to a liquid fuel is a form of energy storage, and producing e-fuels when electricity is cheap means that a less efficient energy transfer can be advantageous if the energy storage and infrastructure is more economical than battery and charging infrastructure. Given that renewable energy curtailments are rising173 (when production is higher than consumption and must be wasted), the energy intensity of e-fuel production is less important than the economic viability of it as an energy storage for transportation vis-à-vis lithium-ion batteries. Ultimately, the scalability of e-fuels depends on their economic utility to consumers, raising another point for why competition among transportation decarbonization methods is important for policy.

Solar fuels also warrant attention as a potential source of liquid fuels. Here, artificial photosynthesis is utilized to produce fuels for use in transportation and industry. In 2020, the Department of Energy awarded $100 million in grants for research on energy production from artificial photosynthesis.174 The technology is still in its infancy, but the hope is that artificial leaves can be used to convert carbon dioxide and sunlight into formic acid, which is an energy-dense liquid that could be used for transportation via fuel-cell vehicles.175 The hope is that if artificial photosynthesis can be achieved using chemicals that are already produced at scale and easily available, carbon neutral liquid fuels could be produced at low cost and in high quantities.176

Another recent innovation has been the potential for carbon capture fuel cell vehicles (CCFCV), where a solid oxide fuel cell is used with minimally reformulated hydrocarbon or ethanol fuel and captured CO2 from combustion is stored onboard.177 The higher efficiency of the fuel cell helps to improve the cost-competitiveness of the CCFCV, and could be pragmatic for larger vehicles for which conventional battery and electrification is impractical (larger batteries require more energy to move thus reducing efficiency).178 However, it is not yet clear if such technology would be lower or higher cost than offsetting the pollution through technological direct air capture technology.179 Additionally, there has also been advancement of “onboard” carbon capture technology for vehicles, such as a carbon capture system for heavy trucks that captures emissions directly from the exhaust stream.180

The key takeaway is that there are non-EV approaches to reducing transportation emissions, which typically have received less policy attention and ironically could be stymied by EV mandates. Given challenges associated with widespread EV adoption, a future in which nearly all light-duty transportation emissions are eliminated may come from an amalgamation of different technologies, with on-road vehicles being a mixture of EVs and highly efficient ICEVs or hybrids that are powered by low-carbon fuels. It is also probable that in situations where EVs are impractical, such as harsh climates that may affect battery reliability, low-carbon liquid fuels may be preferred by customers.

Opportunities for Enhanced Oil Recovery

While much of the focus on abating transportation emissions is on replacing fossil fuel consumption with alternative forms of energy, there is also the possibility of making existing fossil fuel production less carbon intensive, which could significantly cut lifecycle transportation fuel emissions without requiring new vehicle types.

Enhanced oil recovery (EOR) is a process of extracting oil through the injection of carbon dioxide into a well. An oil well is like a straw, and it can only extract the oil that it can reach in the reservoir. Injecting a gas—usually CO2—into the well displaces remaining oil in the reservoir, thereby allowing more oil to be extracted. This process also traps the gas underground. EOR is already a proven technology and is used to produce about 300,000 barrels of oil per day in the United States.181 However, most of the carbon dioxide used for EOR is from natural resources, resulting in no sequestration of anthropogenic CO2.182

Transitioning to EOR utilizing anthropogenic carbon dioxide may significantly reduce the net emissions from petroleum products. The net emissions from a barrel of oil produced through EOR is not uniform, with the potential to have net negative emissions for oil produced early in the process, and then rising emissions later in the process (though still below conventionally extracted oil).183 It is estimated that a barrel of oil produced through EOR could have 63% lower emissions than a conventional barrel.184

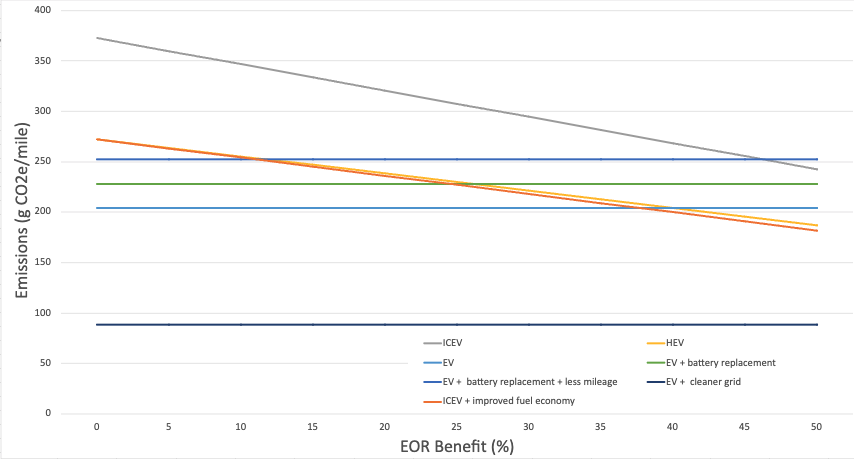

EOR – when coupled with improvements in fuel economy – offers particularly significant emissions reductions for future ICEVs and hybrids that make these vehicles attractive counterparts to EVs. For example, an ICEV with a fuel economy of 34 miles per gallon (mpg) emits 373 gCO2 per mile compared to an EV of comparable internal volume and range which emits 204 gCO2 per mile. However, under finalized CAFE standards, LDVs must achieve a fuel economy of 49 miles per gallon (mpg). Doing so reduces – given the interdependencies between fuel economy and emissions – an ICEV’s per-mile emissions from 373 to 272g CO2.

For reference, if EOR resulted in 38% lower life-cycle fuel emissions, the 68g CO2/mile difference between a current EV and a future ICEV would be negated, meaning that EOR could allow for ICEVs that are cleaner than current EVs. Accounting for battery replacements further facilitates achieving emissions parity between EV and ICEV. As a caveat, though, even with 50% lower lifecycle emissions from fuel thanks to EOR, an EV running on a low-carbon grid would still be cleaner, though the relative emission profiles of vehicles narrow.

EOR is admittedly limited, however, through lack of existing infrastructure and adoption for carbon capture technologies. This may change in the future as novel power plant designs such as the Allam Cycle are able to utilize carbon dioxide produced from natural gas combustion as a working fluid to spin a turbine in a closed loop system.186 A power plant utilizing the Allam Cycle could use affordable and widely available natural gas to produce zero emission electricity, and then send CO2 via pipeline to oil wells for use in EOR. The Allam Cycle has only been demonstrated for the first time in 2018,187 so such potential is novel at this stage, but the company readily points to potential for EOR as something that improves the economics of the power plant.188 With currently high oil prices and protracted demand, opportunities to significantly increase oil production through EOR may gain increased attention.

Perhaps the most significant long-term challenge to EOR, though, is that there is a finite potential of geologic formations that are conducive to EOR recovery. The IEA estimates the current theoretical potential of EOR is to unlock 300 billion barrels of oil.189 That figure is significant, but still far lower than the production potential of conventional oil. That said, some proponents of carbon capture for climate purposes believe that more EOR adoption is essential to seed carbon capture industries that would be needed to meet global net-zero emission targets.190

From a transportation emissions perspective, however, EOR has opportunities for immediate emission abatement that are applicable to anywhere in the world that liquid petroleum fuels are already being utilized. Even if EOR is unlikely to end up becoming an entirety of a climate solution, it holds unexplored potential, especially for exporting lower-carbon fuels to foreign economies that may not be able or willing to adopt EV mandates.

Allow GHG Capture and Sequestration to Count for Transportation Emission Abatement

One opportunity to cut transportation emissions is to allow for vehicle fuel purchases to fund other emission abatement. Current accounting systems are focused primarily on emission sources, but due to the high cost of abating transportation emissions, there may be an opportunity for broader lifecycle accounting to allow for “carbon neutral” fuel where fuel purchases pay for carbon capture or sequestration that equally offsets the carbon dioxide emissions from fuel combustion.

The principal challenge in abating transportation emissions is that the economic impact of the GHG emission almost always falls below the short run willingness of individuals to pay. From 2021-2022, gasoline prices more than doubled (an increase of $2.63 per gallon).191 Because consumers are willing to pay almost any price for transportation, petroleum fuels are only replaced when government mandates or economically viable alternatives induce change. However, the ease of substitutability warrants greater consideration by policymakers. As much as there is a political desire to reduce emissions from combustion engines, that desire does not override the physical constraints that limit current access to viable alternatives.

If eliminating emissions in their entirety is unfeasible, offsetting emissions productions is a mitigation pathway that may warrant some consideration. GHG sequestration or carbon dioxide removal (CDR) are other policies that offer opportunity but come with challenges. Utilization of carbon capture technology carries an additional cost that can vary significantly by industry.192 With few examples of CCS at use at scale today, it is still a nascent technology.

Over time however, improvements to GHG sequestration offer a means of permanent removal from the atmosphere.193 Some examples of such technologies include saline aquifer storage,194 biomass carbon removal and storage,195 carbon mineralization,196 oceanic carbon dioxide removal,197 and direct air capture.198 These technologies are in the early stages of development but hold promise, with tech companies already investing $925 million in such technologies.199 The ability to remove carbon dioxide either from a source of emission or directly from the atmosphere and transfer it to a non-reactive state is of immense value. Its measure, more precisely, can be thought of as the difference between the willingness of firms to pay for such action and the costs of otherwise avoiding GHG emissions.

Current “carbon offsets” are usually temporary in nature or entail some accelerated emission avoidance. Consequently, not all “carbon offsets” fully offset the GHG emissions they claim.200 Permanent CDR, though, more readily addresses concerns of emission mitigation. While carbon offsets are low-cost, often around $15 per metric ton, CDR is comparatively more expensive at up to $300 dollars per ton.201 Over time though, these technologies may reach a cost of around $100 per metric ton.202 At that price point, in transportation, CDR could make some vehicle-use cases more economic to offset their environmental impact rather than transition to EVs or alternative vehicle types.

With the 2026 fuel economy target, 203 a car being driven the average 14,263 miles per year would consume 291 gallons of gasoline and emit 2.6 metric tons of CO2. At a price of $100 per metric ton to sequester carbon dioxide, the annual cost to fully negate the GHG impact of that driving would be $260, or about 89 cents per gallon. For many drivers, especially in areas where EV charging may not be readily available, it may be a more economic or utilitarian to pay for emission sequestration rather than transition to an alternative vehicle type.

Current policies focused on reducing transportation-related emissions emphasize mandates for alternative fuel adoption or improvements in fuel economy. Policies that allow for investment in negative GHG emission purchases to count towards compliance should be considered. There will be some cases where it is more economical to negate non-transportation related emissions than transportation related ones, resulting in a greater overall level of GHG emission abatement. This works due to what is essentially an expansion of competition in decarbonization, where the array of options is expanded, and the central-planning tendency of policymakers is mitigated.

Array of Vehicle and Fuel Alternatives

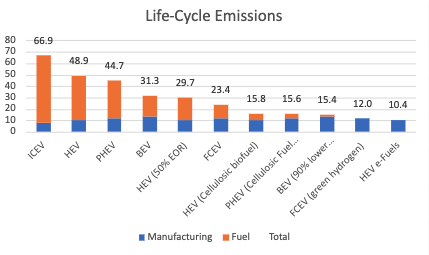

Existing analysis emphasizes comparisons of EVs to ICEVs, but this is a false dichotomy which ignores the variability of potential transportation solutions. Below is a back-of-the-envelope estimate of life-cycle emissions based on MIT estimates but adjusted to also consider improved fuel economy and adoption of EOR, advanced biofuels, and e-fuels. Importantly, battery replacement is not considered.

The above chart shows that while EVs can have significantly better emission profiles than ICEVs and even highly efficient HEVs, this advantage narrows significantly when one considers the potential for ICEVs or HEVs to be fueled by either EOR-derived petroleum fuels (assuming 50% offset from sequestration) or advanced biofuels, which can have 86% lower emissions.206 The GHG emissions profile of an ICEV using advanced biofuels or e-fuels is roughly as low or lower than an EV.

This simple analysis shows that a conventional battery-only EV (BEV) can have 53% lower emissions than a conventional ICEV with a 34 mile per gallon fuel efficiency, or 38% lower emissions than a 52 mile per gallon hybrid. However, the analysis becomes more interesting when considering future vehicle and fuel types. For example, a BEV operating on electricity that is 90% lower emissions than today’s grid is only 4% lower emissions than a 50 mile per gallon hybrid powered by advanced biofuels. Fuel cell vehicles using green hydrogen or hybrids using e-Fuels, which are both carbon neutral, are cleaner than EVs, owing to their lower manufacturing emissions. A 52 mile per gallon hybrid powered by EOR-derived petroleum fuels, assuming 50% offset emissions from sequestration, would be cleaner than the BEVs of today.

The above analysis suggests that policies which favor one vehicle type through the restriction of another, such as EV mandates, may inadvertently obstruct more-efficient emission abatement opportunities from reaching the market. There is an array of potential transportation emission mitigation opportunities that can offer comparable emission abatement to EVs, and even in cases where their emission abatement is not as good as EVs, they may be more applicable to markets where EV adoption is constrained.

Policy Recommendations

Policymakers should consider the plethora of available policy levers that both meaningfully reduce transportation emissions and facilitate market conditions that support the emergence of innovation that can reduce transportation emissions at lower cost than the status quo. Policy proposals, such as EV mandates, are more vulnerable to constraints that could delay the achievement of GHG emission reductions as well as increase the costs of transportation in the United States. While this paper does not offer detailed proposals, in the section below, we lay out several recommendations for policy formulation that would reduce GHG emissions at lower costs than alternative, command-and-control style policies.

Reform EV Subsidies to Focus on Outcomes

From an emission reduction standpoint, the current structure of EV subsidies is ineffective as it rewards consumers solely for purchasing EVs, rather than replacing ICEVs with EVs or substituting ICEV travel. Instead of awarding subsidies for EV purchases alone, many of which may be under-utilized secondary vehicles, existing subsidies should be reformed to be only awarded to vehicle owners based on utilization.207 For example, we can estimate at what number of miles a new EV begins to have lower life-cycle emissions than an ICEV, and EV owners should only be able to claim subsidies after they have reached that point. Further, the value of the subsidy should reflect the overall utilization, with vehicles that are utilized more—and thus more likely to be substituting for ICEV travel—claiming a subsidy (or a larger magnitude of subsidy). This would encourage EV utilization and replacement of ICEVs, rather than purchase of EVs as supplemental vehicles that may not be utilized enough to offset their manufacturing emissions.

Additionally, such a policy could apply to an array of vehicles based on the difference in per-mile emissions between vehicle type and a standard ICEV. HEVs, for example, could become eligible for a lower value subsidy than EVs, but this may reduce emissions to a larger extent given consumer willingness to choose hybrids over EVs. Vehicles powered by biofuels or fuel cells could also be eligible under a similar subsidy structure, and the subsidy would only be awarded for vehicles that are expected to be contributing to emission reduction.

Focusing subsidy structure on ICEV substitution would incentivize vehicle purchasers to find ways to conventionally adopt EVs or other alternative vehicle types, which consequently would encourage producers and market participants to invest in capabilities that facilitate EV use (e.g., charging access and convenience, vehicle reliability, etc.). This approach also has the advantage of transitioning the subsidy structure to be more focused on life-cycle emissions, where market participants that are more responsible for reducing emissions can claim a larger subsidy than ones that do less.

Broaden Compliance Mechanisms for GHG Emission Policies

In comparing policies to reduce GHG emissions, the Congressional Budget Office noted that the economic burdens of climate policy vary widely depending on whether the policies are market-based or command-and-control based.208 Policies that afford consumers the flexibility to choose the best of various options deliver greater efficiency than policies that empower politicians to decide upon one option and force it broadly on the economy. With respect to GHG emissions reductions from LDVs specifically, because there are few perceived emissions reductions options available, policymakers tend to overestimate the certainty that EVs will be the only viable decarbonization option. Public policies imply a lack of appreciation for the potential that EV-focused approaches like mandates could block other more cost-effective options from emerging.