Executive Summary

America’s energy future depends on whether it can commercialize the technology it invents. The United States created the solar cell, pioneered hydraulic fracturing and split the atom, but today China rivals, and according to some sources, has surpassed the U.S. in energy research and development investment. China is also deploying next-generation energy technologies faster than the U.S., where many of these technologies were invented. Policymakers must act now to allow American innovators to help meet our goals of energy affordability, energy dominance and environmental stewardship.

Energy technologies move through a pipeline of research, development and demonstration (RD&D) before reaching commercial scale. The most consequential failure point in this pipeline—the “Valley of Death”—occurs between a successful demonstration and the first privately financed commercial deployment. First-of-a-kind projects can cost more than twice as much as their mature counterparts, and private capital cannot price the long-duration policy and technology risk on its own. When American innovations cannot cross this valley at home, they may be forced to cross it abroad, taking the jobs, supply chains and standard-setting authority with them.

Federal policy cannot pick winners and it should not try. But it can match the right kind of capital to the right stage of risk, remove structural barriers to deployment and provide the durability that allows private capital to commit alongside it. The U.S. Department of Energy’s (DOE) existing programs are well-designed for this purpose, but lack the surrounding policy architecture to ensure innovative technologies are rapidly deployed. The United States has repeatedly demonstrated it can invent. The question is whether it can deploy at the speed and scale its competitors, and its own energy needs, demand.

Crossing the Valley of Death requires action on three interlocking fronts. Congress should:

- Unleash Deployment: Enact comprehensive permitting reform to deploy new technologies, simplify regulations that slow innovation and modernize the interconnection queue so that projects that survive the RD&D pipeline can actually reach the grid.

- Fix the Financing Architecture: Reauthorize expiring Energy Act of 2020 provisions, explore multi-year appropriations for core innovation programs and deploy Title XVII loan authority at scale with technology neutrality.

- Harness AI as a Cross-Cutting Accelerator: Sustain federal investment in Artificial Intelligence (AI)-enabled research infrastructure, ensure regulatory frameworks accommodate AI-based tools and build on the Genesis Mission’s model of shared infrastructure investment.

Introduction

America’s spirit of innovation is a defining piece of our nation’s identity. From Thomas Edison’s lightbulb to George P. Mitchell’s hydraulic fracturing breakthroughs, American innovations have powered our homes, improved our lives and created entire industries that all but guaranteed America’s rise as the world’s leading superpower. As our nation rapidly adopts a wide range of society-changing technologies (e.g., AI, advanced manufacturing, biomedicine, etc.) we must simultaneously accelerate the adoption of innovative energy systems to power this growth. Federal policymakers must ensure that federal policies and programs are oriented toward not just the creation, but the commercialization of technologies that can power our way of life in a cleaner, cheaper and more reliable way.

The Benefits of Innovation

Energy innovation delivers measurable results across a range of benefits, especially affordability, emissions and reliability, and these benefits compound. Each breakthrough reinforces the others, creating a virtuous cycle that strengthens America’s energy position at home and abroad. These include:

- Affordability: Breakthroughs inhorizontal drilling, hydraulic fracturing and 3-D seismic imaging doubled U.S. natural gas production from 18.6 to 37.7 trillion cubic feet between 2005 and 2024.[1] Between 2007 and 2018, the resulting abundance drove natural gas prices down 63 percent and wholesale electricity prices down 45 percent.[2] Meanwhile, installed costs for solar PV and onshore wind fell 87 percent and 55 percent respectively between 2010 and 2024.[3]

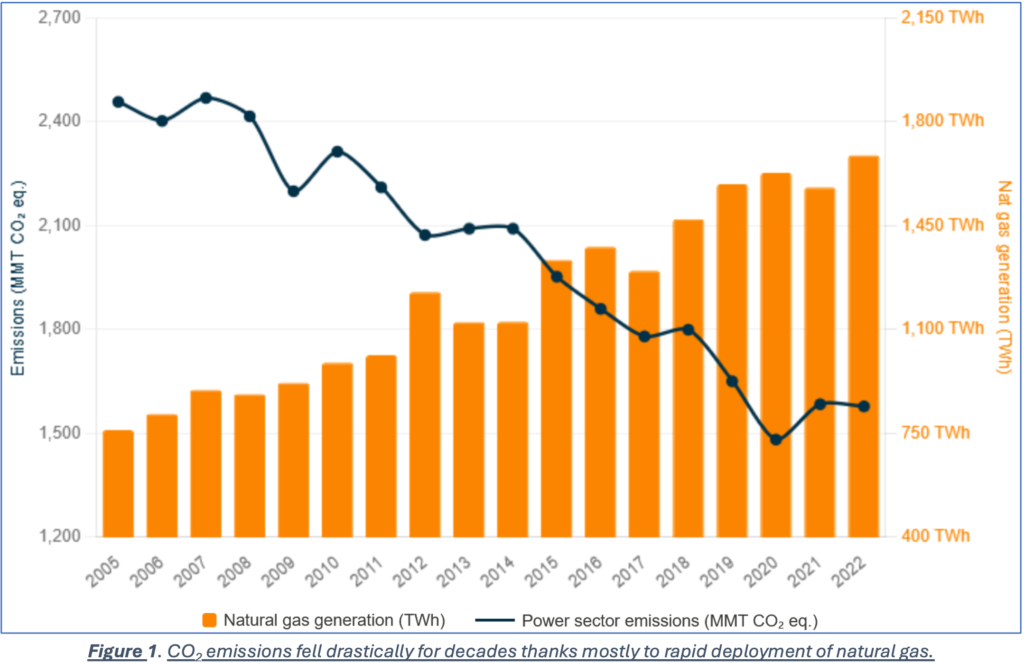

- Emissions: Since 2005, the U.S. power sector reduced carbon dioxide (CO₂) emissions by approximately 41 percent, driven primarily by the shift from coal to natural gas (Figure 1) and the rapid deployment of wind and solar, all while economic growth accelerated.[4] Sulfur dioxide, nitrogen oxides and mercury emissions have declined alongside, delivering direct public health benefits.

- Reliability: New grid technologies are providing an unprecedented level of reliability to grid operators and consumers alike. In Texas, the addition of 7.5 gigawatts (GW) of new battery storage helped the state avoid calling on consumers to cut power usage during high-demand periods, after years of struggling with such concerns.[5] Grid-enhancing technologies have increased line capacity by 9–36 percent in deployments across multiple states.[6]

These direct consumer benefits create the conditions for broader gains in economic competitiveness and national security:

- Economic Growth: U.S. energy storage manufacturing is building an end-to-end domestic supply chain, reducing dependence on Chinese-dominated battery production, and is on track to fully meet domestic battery storage demand by 2027. The industry has committed to invest $100 billion across the country, with the potential to generate over 350,000 jobs; however, significantly more work needs to be done to ensure a secure, domestic critical mineral supply.[7]

- Energy Security: Advanced nuclear reactors can provide clean, firm power with mostly domestic supply chains. In 2025, the Tennessee Valley Authority applied for a Nuclear Regulatory Commission (NRC) construction permit to build a BWRX-300, a small modular reactor built by GE Vernova.[8] This design is currently under pre-application review at the NRC and will provide reliable, secure and clean electrons onto the grid.[9] Furthermore, advanced reactors, enhanced geothermal and battery storage all depend on critical mineral supply chains where China currently dominates processing—a vulnerability that domestic innovation can help address.

- Technology Leadership: American companies are pushing the frontiers of energy technology in ways no other nation can match. Fervo Energy’s Project Red in Nevada became the most productive enhanced geothermal system in history, delivering 24/7 carbon-free power to the grid using horizontal drilling techniques adapted from the oil and gas industry.[10] In fusion, Helion Energy’s Polaris prototype reached 150 million degrees Celsius in February 2026 and became the first privately developed machine to demonstrate measurable deuterium-tritium fusion—an important milestone on the path toward commercialization.[11]

These benefits do not stand on their own; they reinforce one another. When American innovators drive down the cost of producing energy, they simultaneously reduce emissions, strengthen grid reliability and make American products more competitive globally. The same compounding logic applies to next-generation technologies: advanced nuclear, enhanced geothermal, long-duration storage, grid-enhancing technologies and much more. Nations that lead in developing and commercializing these technologies will set the terms of the global energy market. Those that don’t will buy from those that do.

Ensuring America’s Leadership

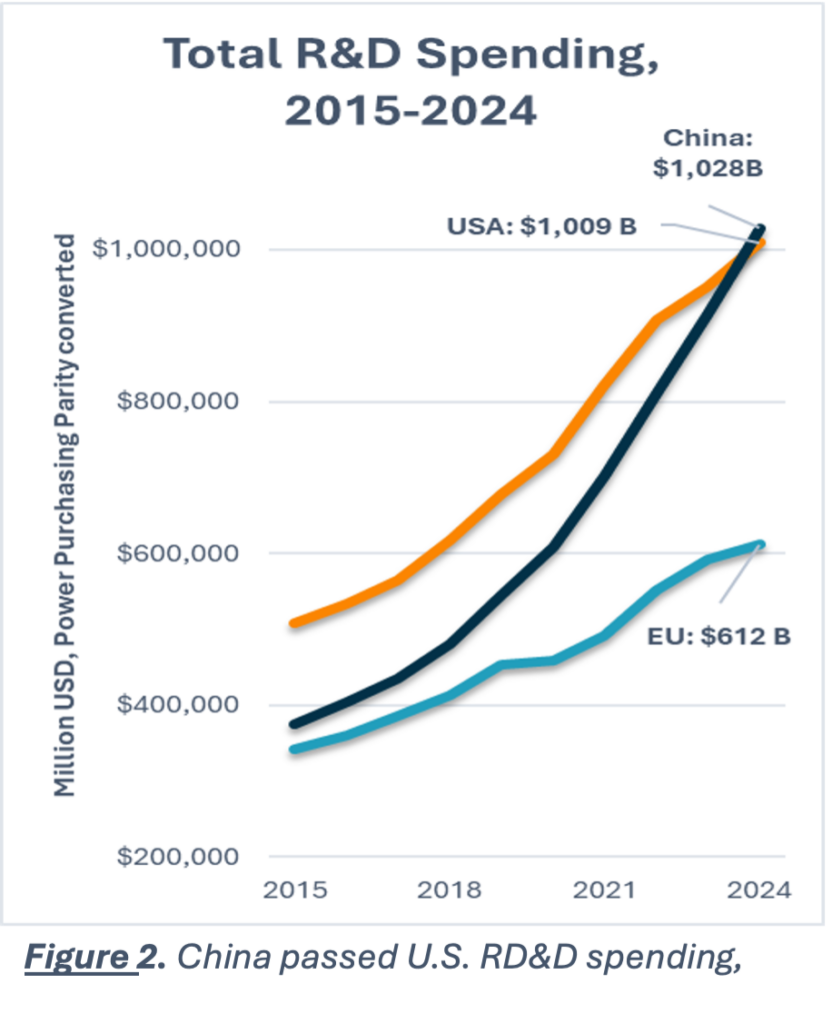

America’s energy innovation advantage is no longer guaranteed. According to data recently released by the Organisation for Economic Co-operation and Development (OECD), China passed the U.S. for total research and development (R&D) investments for the first time ever in 2024, when controlled for purchasing power parity (Figure 2).[12] When controlling for other factors, the picture gets even starker. According to the Council on Foreign Relations’ Global Energy Innovation Index, which compares 39 nations across 16 factors and controls for gross domestic product, the U.S. ranked 13th (China ranked 29th).[13]

The country that invented the solar cell, pioneered hydraulic fracturing and split the atom now falls behind both our largest competitor and smaller nations. While the U.S. still leads the world in other important metrics, such as startup ecosystem and AI development, the signal is clear: America is not the only player on the innovation stage and the gap is closing.[14]

The urgency is compounded by volatility in energy markets that no single energy source can fully insulate against.[15] Geopolitical shocks, shifting trade dynamics and supply chain disruptions have repeatedly demonstrated that energy security cannot rest on any single source, region or technology. A diversified, domestically produced energy portfolio—built on technologies that are more affordable, more reliable and increasingly cleaner—is the most durable hedge against that volatility.[16] That is not an environmental argument. It is a strategic one.

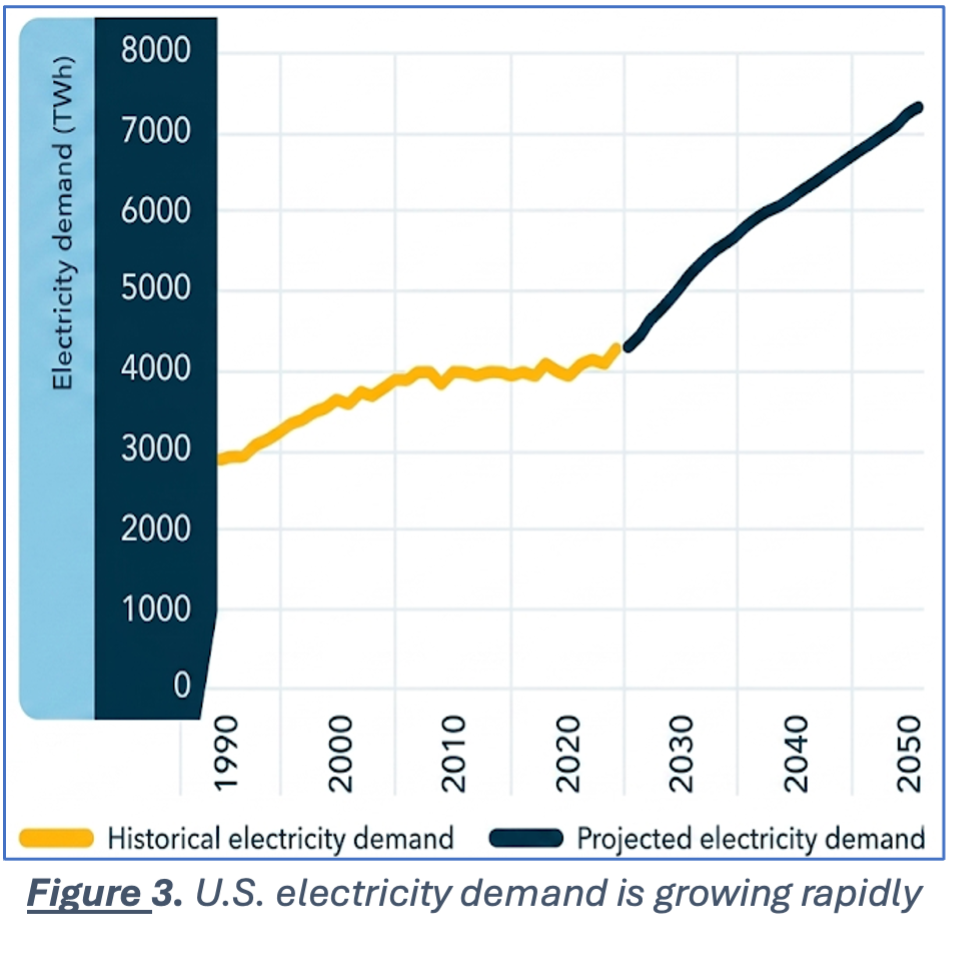

Meanwhile, demand for energy is accelerating. The rapid expansion of data center infrastructure, advanced manufacturing and electrification is driving electricity demand growth not seen in decades. According to a recent report by ICF International, U.S. electricity demand could grow up to 25 percent by 2030 and up to 78 percent by 2050 (Figure 3).[17] To meet this demand, grid operators, policymakers and investors should look to American-made energy innovations as an asset.

The private sector is already signaling where this is headed. In the fourth quarter of 2025, Americans installed 1 GW direct current of rooftop solar capacity to lower utility bills.[18] Across 2025, homeowners adopted 3.1 GW hours of new battery storage capacity to protect against outages.[19] These are market signals that clean energy technologies are maturing, that demand is real and that the commercialization race is already underway.

The question is not whether America will deploy innovative and clean energy systems. The question is whether America will lead that innovation—commercializing its own inventions, building the supply chains, setting the standards—or whether it will cede that ground to competitors who move faster and invest more.

The Innovation Lifecycle: Research, Development and Deployment

What is “RD&D”?

New technologies do not leap from a researcher’s notebook to the power grid overnight. The process of creating, testing and proving new energy technologies is arduous and costly, often taking decades to complete. Congress and federal agencies use the shorthand “RD&D”—research, development and demonstration—to describe this process, and understanding what each term means is essential to understanding how federal dollars support it.

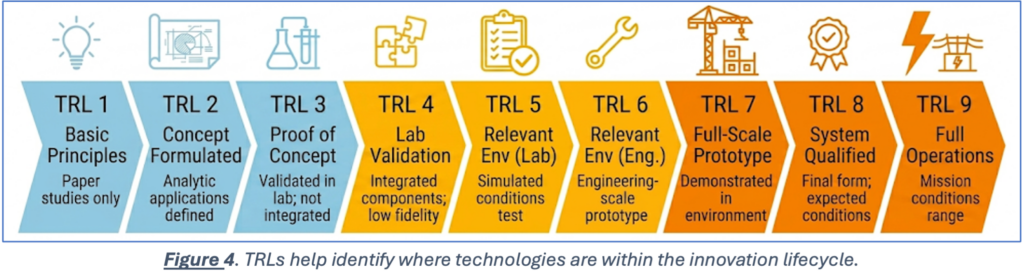

The DOE uses a more formalized version of this framework called “Technology Readiness Levels” (TRLs) to inform how it invests across these stages (Figure 4).[20] Originally developed by the National Aeronautics and Space Administration (NASA), the TRL scale runs from 1 to 9: basic research occupies the low end (TRL 1–3), development and prototyping the midrange (TRL 4–6) and demonstration through commercial deployment the high end (TRL 7–9).[21]

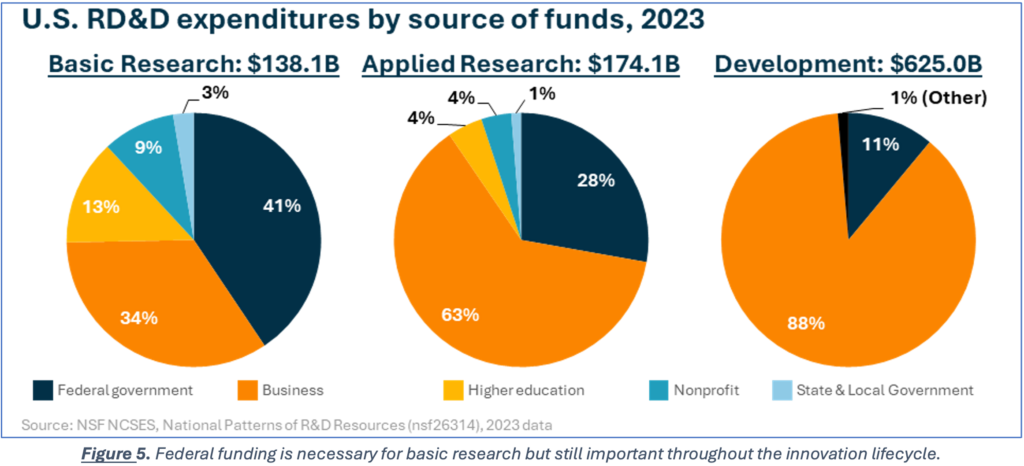

Research is basic science (TRL 1-3), the pursuit of fundamental knowledge without a specific commercial application in mind. This is the work of national laboratories and universities: discovering new materials, modeling physical processes, testing theoretical concepts. The outcomes are uncertain and the commercial payoff may be years or decades away, which is precisely why the private sector does not invest in this phase (Figure 5).

DOE’s Office of Science is the federal government’s largest vehicle for basic research.[22] In Fiscal Year 2026, Congress provided $8.4 billion to fund this office, which supports over 25,000 researchers at more than 300 institutions and all 17 national laboratories.[23] The Advanced Research Projects Agency–Energy (ARPA-E) complements the Office of Science by targeting high-risk, high-reward concepts too speculative for conventional RD&D programs.

Development is applied science and engineering (TRL 4–6), taking the knowledge generated by basic research and turning it into something that works. During this stage, engineers design prototypes, test components under real-world conditions and iterate on designs to improve performance. Development attracts more private investment than basic research because the commercial potential is becoming clearer, but the technology is still unproven and the costs of failure remain high.

DOE supports technological development via its applied program offices, such as the Office of Electricity, the Office of Nuclear Energy and the Office of Critical Minerals and Energy Innovation. Through these bodies, the DOE runs competitive grants, cooperative agreements and pilot programs across energy sectors. Two bridge mechanisms are particularly important: ARPA-E’s SCALEUP program and the Technology Commercialization Fund (TCF).

SCALEUP provides follow-on funding for technologies that need pre-commercial scaling to attract private investment.[24] The TCF is a dedicated funding stream to move national laboratory inventions and intellectual property toward the market.[25] DOE also operates lab-industry collaboration mechanisms—such as Strategic Partnership Projects, personnel exchange programs and technical assistance to small businesses—that reduce the cost and risk of development for private firms.[26]

Demonstration is the bridge between a working prototype and a commercial product (TRL 7–9). At this stage, a technology is built and operated at or near commercial scale—a pilot plant, a first-of-a-kind (FOAK) reactor, a full-size carbon capture facility—to prove that it can perform reliably and economically outside the laboratory. Demonstration projects are among the most expensive and highest-risk stages of the innovation pipeline, because they require real capital deployed against unproven economics.

The federal role for demonstration projects is to share the cost and absorb the risk of FOAK projects so that the private sector can establish the performance record, construction experience and supply chains needed to finance subsequent deployments without government support. The Advanced Reactor Demonstration Program illustrates the model: TerraPower and X-energy, two nuclear power startups, are each building FOAK reactors at a 50-50 public-private cost share, with TerraPower’s Natrium reactor receiving its NRC construction permit in early 2026—the first commercial non-light-water reactor approved in over 40 years.[27]

Each stage demands different resources, expertise and capital—and no single actor carries a technology across this entire journey alone. The pipeline depends on handoffs between institutions with fundamentally different risk tolerances and investment horizons. Basic research is funded almost exclusively by the federal government and universities. Applied development attracts a mix of public and private capital. And full-scale deployment is overwhelmingly financed by private capital—project finance, utility procurement and corporate balance sheets.

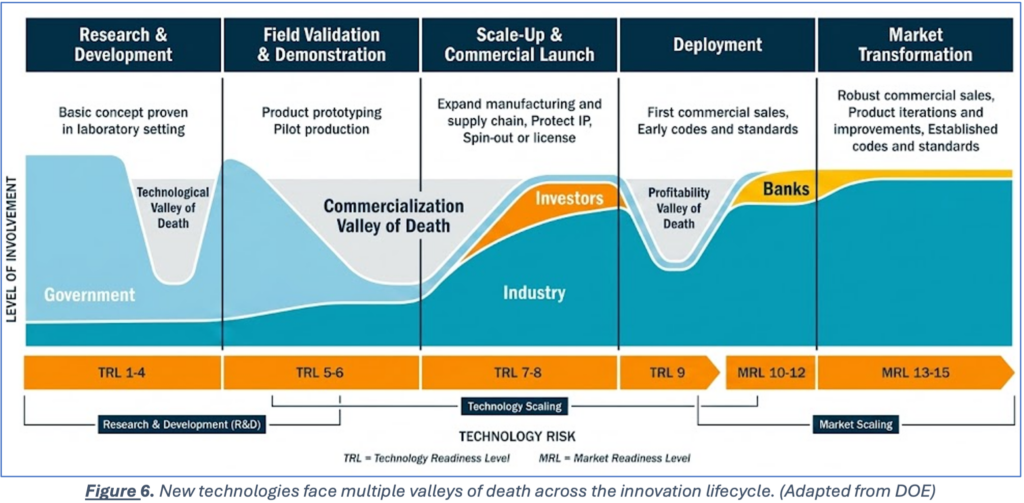

The Commercialization Valley of Death

The progression from research to development to demonstration can suggest that technologies flow naturally from one stage to the next. Unfortunately, this is not the case. Technologies face several failure points along the way—commonly referred to as “valleys of death”—where promising innovations stall out before reaching the next stage (Figure 6). The most consequential of these occurs between a successful demonstration and the first privately financed commercial deployment.[28] A technology entering this valley has proven it can work in a controlled setting, but has not demonstrated an ability to operate commercially.

The problem is as much about finances, permitting and regulations as it is about scientific or engineering challenges. Energy projects using known technologies, often referred to as “Nth of a Kind” (NOAKs) projects, cost millions, if not billions, of dollars to construct. Deploying FOAK technologies brings significant risks that drive up capital costs.[29] Factors such as engineering costs, supply chain uncertainties, learning curves and financing risks all push the costs of financing FOAK projects well above that of NOAK projects.[30]

According to the U.S. Energy Information Administration, the capacity-weighted average cost to construct an NOAK power plant in 2023 was $1,459 per kilowatt (kW) of installed nameplate capacity.[31] According to a 2023 study by Idaho National Labs on advanced nuclear reactor cost estimates, FOAK power plants (in this case nuclear reactors) could be more than double the cost of NOAK projects (Figure 7).[32] While this study was limited to just nuclear reactors, it’s useful for setting expectations: grid planners, investors and policymakers could expect FOAK energy projects to cost up to $2,900 per kW, an astounding and uncompetitive figure across most of the U.S.

The consequence is not just that good technologies fail. It is that American-invented technologies get commercialized elsewhere. When the United States cannot deploy its own innovations at scale, there is a risk that other countries, including our competitors, with more aggressive government-backed financing, guaranteed off-take agreements and faster permitting timelines step in. The U.S. has repeatedly demonstrated that it can invent. The question is whether it can deploy at the speed and scale that its competitors—and its own energy needs—demand.

Closing this gap requires federal tools that do for commercialization what grants and cooperative agreements do for research and development: match the right kind of capital to the right stage of risk. DOE’s Office of Energy Dominance Financing (EDF), formerly the Loan Programs Office, provides federal loan guarantees for projects that use innovative technologies but cannot yet secure purely private financing.[33] EDF has over $289 billion in loan authority and a current portfolio of nearly $125 billion.[34] EDF deploys capital at a fraction of the taxpayer cost of equivalent grant programs, allowing private lenders to finance FOAK projects that would otherwise not be investable via the market on its own.

Beyond financing, DOE operates commercialization and ecosystem tools that span multiple TRLs, serving as connective tissue between lab discoveries and markets. Entrepreneurial fellowships, lab-embedded startup programs and technology-to-market initiatives (i.e., TCF) help researchers understand market needs, connect startups to national laboratory capabilities and prepare technologies for the due diligence that investors and lenders require. These cross-cutting tools do not replace grants, loans or demonstrations—they link them, ensuring that when a technology graduates from DOE’s research and demonstration programs, there is a viable path to private investment and repeat deployment.

Beyond the Valley: Additional Commercialization Challenges

Having the right tools is necessary but not sufficient. Several systemic challenges curb the impact of DOE’s innovation programs, reducing the return and efficiency of taxpayer dollars. These are not critiques of DOE—they are structural conditions that determine whether DOE-backed innovations can scale fast enough to matter. In each case, there is either a market failure that private capital cannot resolve on its own or a problem caused by federal action or regulation in the first place. Either way, these challenges limit the impact of taxpayer dollars to achieve the desired ends of accelerating America’s competitive edge through innovative technologies.

Sluggish Deployment: Permitting, Regulatory and Interconnection Barriers

Even technologies that successfully navigate the RD&D pipeline face a second gauntlet at the deployment stage: a permitting, regulatory and interconnection system that was not designed for the pace or diversity of modern energy innovation.

A Broken Federal Permitting System

America’s broken permitting system creates delays that no private actor can engineer around. Energy projects take an average of 4.5 years to review, with infrastructure projects taking an average of 6.5 years.[35] Major infrastructure including transmission lines and pipelines, nuclear facilities and industrial-scale carbon capture projects regularly face timelines exceeding a decade.[36] Over 1,000 projects worth an estimated $1.5 trillion are waiting for permitting approval today, and the dysfunction carries a measurable price tag—up to $140 billion in lost annual revenue and construction cost increases of as much as 30 percent.[37]

These are not the costs of environmental protection; they are the costs of duplicative reviews, overlapping federal, state and local jurisdictions, and indefinite litigation windows that delay projects regardless of their merit. Delayed permitting is often delayed benefit. For energy innovation specifically, the damage compounds upstream. If developers cannot see a realistic path from demonstration to permitted, operating facility, the commercial signal that pulls private investment into earlier-stage R&D weakens. Private capital cannot fix a broken regulatory system; policymakers in Washington must fix what is broken.

Regulation Slowing Innovation

The problem runs deeper than timelines. Many existing, overly complex regulatory frameworks are prescriptive rather than performance-based—written around specific technologies rather than desired outcomes. When statutes and regulations specify the method rather than the result, they inadvertently lock out superior technologies as they emerge. An oil and gas monitoring requirement written around one type of sensor forecloses adoption of better sensors.[38] A definition of geothermal energy written around water as a heat transfer fluid excludes next-generation systems that may use other fluids, like supercritical CO₂, that may significantly outperform it.[39] Fixing this is inherently a legislative and regulatory function—and when Congress and agencies fail to modernize those frameworks, the cost falls on every innovator trying to cross the Valley of Death and ultimately consumers including American families and businesses.

Grid Interconnection Delays

Even projects that clear permitting and meet regulatory requirements face a third barrier: getting onto the grid. The electric interconnection queue—the process by which new power generation projects apply for and receive grid access—has become a severe bottleneck in its own right. As of 2026, over 2,400 GW of generation capacity and storage were waiting in interconnection queues across the country, the vast majority of which will never reach commercial operation.[40] The wait time for an interconnection request is over four years, the cost and timeline uncertainty of which has become a primary reason developers abandon otherwise viable projects.[41] For innovative energy technologies entering the market for the first time, this interconnection uncertainty is particularly acute. Grid operators and utilities have limited experience underwriting novel generation profiles, adding another layer of risk on top of an already capital-intensive process.

A Fragmented Financing Architecture

Private capital is necessary to commercialize energy technologies at scale, but the current financing environment creates structural gaps that markets alone cannot close—particularly for first-of-a-kind projects.

Uncertain Authorizations and Appropriations

Energy innovation operates on long timelines. A FOAK nuclear reactor takes a decade or more from award to operation under DOE’s Advanced Reactor Demonstration Program. Hub-style programs—whether the Regional Clean Hydrogen Hubs, the Industrial Demonstrations program at the Office of Clean Energy Demonstrations, or long-running research centers at the national labs—require sustained coordination across federal agencies, industry partners and academic institutions that cannot be switched on and off. Yet the annual federal appropriations process imposes annual uncertainty on inherently multi-year commitments.

Expired authorizations, lapsed appropriations, continuing resolutions and large year-to-year funding swings stall projects mid-pipeline, strand private investment committed on the expectation of stable federal support and erode the trust that industry partners need to commit capital. ARPA-E’s competitive, milestone-based funding model depends on this kind of predictability; so does EDF’s ability to underwrite multi-billion-dollar project guarantees.

From Challenges to Solutions

These structural challenges—slow deployment, fragmented financing and the policy uncertainty that compounds both—are not necessarily permanent features of the American energy or innovation systems. They are the product of specific choices made in Washington, which means they can be addressed by different choices in Washington. Congress and policymakers throughout government don’t have to be experts in technology, science or energy to address these challenges, but they must use system-level thinking rather than focus on one technology or another. To be truly competitive, America must lead across a wide range of energy technologies and systems, even those that haven’t been invented yet.

Policy Recommendations

Federal policymakers can compress and bridge the Valley of Death not by picking technological winners, but by removing the structural barriers that prevent proven technologies from reaching commercial scale. The recommendations below fall into three interlocking categories: unleashing deployment, stabilizing the financing architecture and harnessing AI as a cross-cutting accelerator.

Unleash Deployment: Fix Permitting, Modernize Regulation and Reform Interconnection

Enact comprehensive permitting reform

Predictable timelines and judicial certainty are a prerequisite for the private capital that moves technologies through the Valley of Death. Our permitting process should not be a red light process, but instead a green light process with adequate protections. Congress should:

- Reform judicial review to curb frivolous litigation and accelerate adjudication.

- Expand categorical exclusions for low-impact projects, including geothermal exploration and interconnection upgrades.

- Set enforceable review deadlines, including strict timelines and default-approval mechanisms when agencies miss statutory timelines.

- Lengthen permit durations to reduce reapplication burdens and ease agency backlogs.

- Modernize interagency processes through digital tools, shared datasets and concurrent—not sequential—reviews.

- Review all permitting statutes and remove the inefficiencies that unnecessarily delay deployment.

Simplify and modernize regulations to unleash innovation

Prescriptive technology mandates lock regulators into yesterday’s engineering assumptions and penalize genuine innovation. Outcome-based frameworks—defining what a technology must achieve on emissions, safety and reliability without dictating how—allow new entrants to compete on their merits. Congress and regulators should:

- Streamline and reduce duplicative or outdated federal regulations that raise compliance costs without improving outcomes, particularly those that advantage incumbent technologies over newer entrants.

- Shift from prescriptive technology mandates to performance-based standards that specify the desired outcome and leave the engineering decisions to innovators.

- Ensure regulatory frameworks can accommodate technologies whose performance profiles were not contemplated when existing rules were written.

Reform interconnection to match project timelines

Clearing the permitting path is insufficient if projects then wait years for a grid connection. Congress and FERC should:

- Accelerate interconnection study timelines and evaluate projects in clusters rather than serial queues.

- Prioritize by readiness and deployment speed, not queue position.

- Support advanced transmission technologies that unlock latent capacity on existing infrastructure (e.g., grid-enhancing technologies, high-capacity reconductoring, dynamic line rating, etc.).

- Expand extra-high-voltage transmission corridors to accommodate the load growth from data centers, advanced manufacturing and electrification.

Fix the Financing Architecture

FOAK projects cannot attract purely private financing at reasonable rates—not because they are bad investments, but because the risks don’t fit cleanly into existing capital markets. Federal policy can change that calculus without creating permanent subsidies or picking winners. Three tools deserve sustained attention.

Stabilize core innovation programs via reauthorization and multi-year appropriations

Most provisions of the Energy Act of 2020—a law signed by President Trump that underpins core innovation programs—have already expired or will soon. Also, many of DOE’s core innovation programs are misaligned with the long-term nature of the financing of many energy projects due to the nature of the annual appropriations cycle. Congress should:

- Update and reauthorize the expiring provisions of the Energy Act of 2020 to preserve the legal foundation for core RD&D programs.

- Explore multi-year authorization and appropriations structures for the national laboratories, ARPA-E and applied program offices that translate research into deployment.

- Strengthen oversight of multi-year commitments through clear milestones and performance metrics, ensuring taxpayer dollars continue to deliver results.

Deploy federal loan authority at scale

DOE’s Title XVII loan authority, expanded under the One Big Beautiful Bill Act, can bridge early-stage financing gaps without distorting markets. Recent projects—the Palisades nuclear restart and American Electric Power’s 5,000-mile reconductoring initiative—demonstrate the tool’s potential when applied effectively. Congress and DOE should:

- Maintain technology neutrality across both Section 1703 (innovation and emissions reduction) and Section 1706 (energy security and reliability), ensuring the full statutory range of national energy priorities is served.

- Structure funding and financing decisions to be performance-based and regionally flexible, prioritizing affordability, reliability and domestic supply chain strength.

- Use conditional commitments and loan guarantees to accelerate private investment, not replace it.

AI as a Cross-Cutting Accelerator

Permitting reform and financing architecture address the structural barriers to deployment. A third force is beginning to compress the innovation pipeline itself—and federal policy should accelerate its adoption.

AI is already shortening timelines across every stage of the RD&D lifecycle. Microsoft and DOE’s Pacific Northwest National Laboratory used AI and high-performance computing to screen over 32 million battery material candidates in a fraction of the time conventional methods require.[42] Zanskar, a geothermal startup, uses AI models trained on decades of subsurface data to identify the first commercially viable blind geothermal system discovered in the United States in over 30 years—at a fraction of conventional exploration cost.[43] DOE’s own permitting support tools are beginning to apply AI to streamline environmental review, reducing the staff-hours required to prepare and process applications.[44]

In November 2025, President Trump signed Executive Order 21665 launching the Genesis Mission—directing DOE to unite its 17 national laboratories, industry and academia around an integrated AI platform explicitly aimed at securing American energy dominance.[45] With $293 million in initial funding, the Mission illustrates the federal model this paper advocates: targeted investment in shared infrastructure that no single private actor would build, accelerating energy innovation across the entire pipeline rather than at any single stage.[46]

Congress and the administration should build on this foundation:

- Sustain and expand federal investment in AI-enabled research infrastructure at the national labs and ARPA-E.

- Ensure technology-neutral regulatory frameworks allow AI-based monitoring and assessment tools to qualify for compliance pathways.

- Equip DOE’s commercialization programs to evaluate and support AI-integrated energy technologies as they move toward deployment.

AI can compress timelines, reduce exploration risk and streamline regulatory review. What it cannot do is close the financing gap that opens when a technology is too mature for research grants but too unproven for commercial lenders. The structural tools above remain necessary. AI makes them more effective by accelerating what happens on either side of the Valley of Death, but it does not eliminate the valley itself.

Conclusion

America’s spirit of innovation has always been the engine of its rise—from Edison’s lightbulb to the shale revolution, from the first solar cell to the first enhanced geothermal system. That spirit is not in question. What is in question is whether the country that still invents can also deploy, commercialize and scale at the pace demanded in today’s competitive global markets.

The Valley of Death is not a permanent feature of the American innovation system. It is the product of specific choices: permitting frameworks that slow deployment, regulatory structures that lock out innovation, financing architectures that cannot support new projects throughout deployment. Each of these choices can be remade. None requires federal policymakers to be experts in geothermal drilling, reactor physics or battery chemistry. They require system-level thinking, sustained attention and the political will to build policy that outlasts any single administration.

The spirit of innovation is still here. The valley still has to be crossed. The question is whether America will build the bridge.

Appendix

[1] Wang, Z., & Krupnick, A. (2013, May). U.S. shale gas development: What led to the boom? Resources for the Future. https://media.rff.org/documents/RFF-IB-13-04.pdf; Natural Gas [Data set]. (n.d.). U.S. Energy Information Administration. https://www.eia.gov/dnav/ng/hist/n9070us2A.htm

[2] The Council of Economic Advisers. (2019, October). The value of U.S. energy innovation and policies supporting the shale revolution. https://trumpwhitehouse.archives.gov/wp-content/uploads/2019/10/The-Value-of-U.S.-Energy-Innovation-and-Policies-Supporting-the-Shale-Revolution.pdf

[3] International Renewable Energy Agency. (2025, July). Renewable power generation costs in 2024. https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2025/Jul/IRENA_TEC_RPGC_in_2024_2025.pdf

[4] Center for Climate and Energy Solutions. (n.d.). U.S. emissions. https://www.c2es.org/content/u-s-emissions/

[5] North American Electric Reliability Corporation. (2025, May 14). 2025 summer reliability assessment. https://www.nerc.com/globalassets/programs/rapa/ra/nerc_sra_2025.pdf

[6] Idaho National Laboratory. (2022, December). A guide to case studies of grid enhancing technologies. https://inl.gov/content/uploads/2023/03/A-Guide-to-Case-Studies-for-Grid-Enhancing-Technologies.pdf

[7] Energy Storage Coalition. (2026, March). Energy storage powers American manufacturing. https://www.energystorage.org/resources/energy-storage-powers-american-manufacturing-one-pager

[8] GE Vernova. (2025, May 20). Tennessee Valley Authority submits application for construction of first BWRX-300 small modular reactor in the U.S. [Press release]. https://www.gevernova.com/news/press-releases/tennessee-valley-authority-submits-application-construction-first-bwrx-300-small-modular-reactor-in-us

[9] U.S. Nuclear Regulatory Commission. (n.d.). GVH BWRX-300. https://www.nrc.gov/reactors/new-reactors/advanced/who-were-working-with/pre-application-activities/bwrx-300

[10] Fervo Energy. (2023, July 18). Fervo Energy announces technology breakthrough in next-generation geothermal [Press release]. https://fervoenergy.com/fervo-energy-announces-technology-breakthrough-in-next-generation-geothermal/

[11] Helion Energy. (2026, February 13). Helion achieves new industry-first fusion energy milestones, accelerating path to commercial fusion [Press release]. https://www.helionenergy.com/articles/helion-achieves-new-fusion-energy-milestones/

[12] Organisation for Economic Co-operation and Development. (n.d.). Main science and technology indicators (MSTI database) [Data set]. OECD Data Explorer. https://data-viewer.oecd.org/?chartId=2859a6ca-a9b5-4f1f-a51b-20fd60c6bfdf

[13] Hart, D., Cunliff, C., Beams, M., & Subrahmanian, A. (2025, November). Global energy innovation index. Council on Foreign Relations. https://www.cfr.org/reports/global-energy-innovation-index

[14] David, E. (n.d.). Ranking the startup ecosystems of 1,000 cities and 100 countries. Crunchbase. https://about.crunchbase.com/blog/ranking-the-startup-ecosystems-of-1000-cities-and-100-countries; Stanford Institute for Human-Centered Artificial Intelligence. (2025). The 2025 AI Index Report. https://hai.stanford.edu/ai-index/2025-ai-index-report

[15] International Energy Agency. (2025, November 12). World energy outlook 2025. https://www.iea.org/reports/world-energy-outlook-2025

[16] J.P. Morgan. (2026, April 9). Energy outlook 2026: Mitigating volatility with a diverse energy mix. https://www.jpmorgan.com/insights/global-research/outlook/energy-outlook

[17] ICF International. (2025, June 9). Fast forward: Electricity demand expected to grow 25% by 2030. https://www.icf.com/insights/energy/electricity-demand-expected-to-grow

[18] Solar Energy Industries Association & Wood Mackenzie. (2025, December 8). Solar market insight report Q4 2025. https://seia.org/research-resources/solar-market-insight-report-q4-2025/; Tran, B. (2026, April 8). Home battery storage market: How many households are adopting solar + storage? PatentPC. https://patentpc.com/blog/home-battery-storage-market-how-many-households-are-adopting-solar-storage

[19] Solar Energy Industries Association. (2026, February 23). U.S. adds 58 GWh of new energy storage capacity in 2025, largest single year of new battery capacity on record. https://seia.org/news/united-states-installs-58-gwh-of-new-energy-storage-in-2025/

[20] U.S. Department of Energy, Office of Clean Manufacturing and Energy Innovation. (n.d.). Technology-to-market. https://www.energy.gov/cmei/buildings/technology-market

[21] Manning, C. G. (2023, September 27). Technology readiness levels. National Aeronautics and Space Administration. https://www.nasa.gov/directorates/somd/space-communications-navigation-program/technology-readiness-levels/

[22] U.S. Department of Energy, Office of Science. (n.d.). National laboratories. https://www.energy.gov/science/office-science-national-laboratories

[23] Holt, M., & Normand, A. E. (2026, March 25). Energy and water development: FY2026 appropriations (CRS Report No. R48599). Congressional Research Service. https://www.congress.gov/crs-product/R48599

[24] U.S. Department of Energy, Advanced Research Projects Agency–Energy. (n.d.). SCALEUP program. https://arpa-e.energy.gov/programs-and-initiatives/SCALEUP-program

[25] U.S. Department of Energy. (n.d.). Technology commercialization fund. https://www.energy.gov/technologycommercialization/technology-commercialization-fund

[26] U.S. Department of Energy. (n.d.). Laboratory partnering. https://www.energy.gov/gc/laboratory-partnering

[27] U.S. Department of Energy, Office of Nuclear Energy. (n.d.). Advanced reactor demonstration projects. https://www.energy.gov/ne/advanced-reactor-demonstration-projects; TerraPower. (2026, March 4). NRC approves Natrium reactor construction permit [Press release]. https://www.terrapower.com/NRC-Approves-Natrium-Reactor-Construction-Permit

[28] Murphy, L. M., & Edwards, P. L. (2003). Bridging the valley of death: Transitioning from public to private sector financing. National Renewable Energy Laboratory. https://docs.nrel.gov/docs/gen/fy03/34036.pdf

[29] U.S. Department of Energy, Office of Clean Energy Demonstrations. (2024, November). Portfolio insights: Learning from case studies: Financing and development approaches from recent first-of-a-kind projects. https://www.energy.gov/sites/default/files/2024-11/FOAK%20Financing%20and%20Development%20Approaches_112024_vf.pdf;

[30] Boldon, L. M., & Sabharwall, P. (2014). Small modular reactor: First-of-a-kind (FOAK) and Nth-of-a-kind (NOAK) economic analysis. Idaho National Laboratory. https://inldigitallibrary.inl.gov/sites/sti/sti/6293982.pdf; Third Way. (2024, February 6). Why FOAK nuclear reactors are so expensive—and worth the cost. https://www.thirdway.org/blog/why-foak-nuclear-reactors-are-so-expensive-and-worth-the-cost

[31] U.S. Energy Information Administration. (2025, July 28). Construction cost data for electric generators installed in 2023 [Data set]. https://www.eia.gov/electricity/generatorcosts/

[32] Abou-Jaoude, A., Lin, L., Bolisetti, C., Worsham, E., Larsen, L. M., & Epiney, A. (2023, October). Literature review of advanced reactor cost estimates. Idaho National Laboratory, Integrated Energy Systems. https://gain.inl.gov/content/uploads/4/2024/11/INL-RPT-23-72972-Literature-Review-of-Adv-Reactor-Cost-Estimates.pdf

[33] U.S. Department of Energy. (n.d.). Office of Energy Dominance Financing. https://www.energy.gov/EDF

[34] U.S. Department of Energy. (2026, January 22). Energy department reins in over $83 billion in Biden-era loans and conditional commitments [Press release]. https://www.energy.gov/articles/energy-department-reins-over-83-billion-biden-era-loans-and-conditional-commitments; U.S. Department of Energy, Office of Energy Dominance Financing. (2026, March 31). EDF portfolio performance. https://www.energy.gov/edf/edf-portfolio-performance

[35] American Clean Power Association. (2024, April). U.S. permitting delays hold back economy, cost jobs. https://cleanpower.org/wp-content/uploads/gateway/2024/04/ACP-Pass-Permitting-Reform_Fact-Sheet.pdf

[36] American Clean Power Association. (2024, April). U.S. permitting delays hold back economy, cost jobs. https://cleanpower.org/wp-content/uploads/gateway/2024/04/ACP-Pass-Permitting-Reform_Fact-Sheet.pdf

[37] Federal Permitting Improvement Steering Council. (n.d.). FAST-41 projects by project status [Data set]. Permitting Dashboard. https://data.permits.performance.gov/Permitting-Project/FAST-41-Projects-by-Project-Status/t5tq-789w; Sternfels, B., & Kumar, A. (2025, July 28). Unlocking US federal permitting: A sustainable growth imperative. McKinsey & Company. https://www.mckinsey.com/industries/public-sector/our-insights/unlocking-us-federal-permitting-a-sustainable-growth-imperative

[38] Natural Gas Innovation Network. (n.d.). Measuring our way to differentiation. https://www.natgasinnovation.com/measurement-technology

[39] Cabeza, L. F., de Gracia, A., Fernández, A. I., & Farid, M. M. (2017). Supercritical CO2 as heat transfer fluid: a review. Applied Thermal Engineering, 125, 799–810. https://doi.org/10.1016/j.applthermaleng.2017.07.049

[40] Rand, J., Manderlink, N., Zhang, S., Talley, C., Gorman, W., Wiser, R., Seel, J., Mulvaney Kemp, J., Jeong, S., & Kahrl, F. (2025, December). Queued up: 2025 edition, characteristics of power plants seeking transmission interconnection as of the end of 2024. Lawrence Berkeley National Laboratory. https://emp.lbl.gov/publications/queued-2025-edition-characteristics

[41] Rand, J., Manderlink, N., Zhang, S., Talley, C., Gorman, W., Wiser, R., Seel, J., Mulvaney Kemp, J., Jeong, S., & Kahrl, F. (2025, December). Queued up: 2025 edition, characteristics of power plants seeking transmission interconnection as of the end of 2024. Lawrence Berkeley National Laboratory. https://emp.lbl.gov/publications/queued-2025-edition-characteristics

[42] Bolgar, C. (2024, January 9). Discoveries in weeks, not years: How AI and high-performance computing are speeding up scientific discovery. Microsoft. https://news.microsoft.com/source/features/sustainability/how-ai-and-hpc-are-speeding-up-scientific-discovery/

[43] Zanskar Geothermal. (2025, December 4). Zanskar reveals ‘Big Blind’ – the discovery of the first blind geothermal system in the U.S. by industry in over 30 years [Press release]. https://zanskargeothermal.substack.com/p/zanskar-reveals-big-blind-the-discovery

[44] U.S. Department of Energy, Office of Policy. (2025, July 10). Faster, better permitting with PermitAI. https://www.energy.gov/policy/articles/faster-better-permitting-permitai

[45] The White House. (2025, November 24). Launching the Genesis Mission [Presidential action]. https://www.whitehouse.gov/presidential-actions/2025/11/launching-the-genesis-mission/

[46] U.S. Department of Energy. (2026, March 17). Energy department announces $293 million in funding to support Genesis Mission national science and technology challenges [Press release]. https://www.energy.gov/articles/energy-department-announces-293-million-funding-support-genesis-mission-national-science