Clean hydrogen is quickly emerging as a strategic tool for industrial competitiveness—and the United States is well-positioned to lead.

Clean hydrogen offers a transformative opportunity for American industrial renewal and global energy leadership. From refineries and fertilizer plants to steel mills and shipping ports, it offers a practical path to strengthen America’s manufacturing base while lowering global emissions. The United States has clear natural advantages for clean hydrogen production—abundant energy resources such as low-cost natural gas, nuclear power and other low-emissions generation assets, as well as extensive geological storage capacity, a skilled energy workforce and a thriving innovation ecosystem.

However, global competitors are moving quickly, and the United States has a narrow window to secure its edge to ensure the U.S. remains a supplier of choice in a rapidly evolving global market. Strategic early investment in clean hydrogen can help modernize legacy industries, open up new export markets for American technologies and fuels and bolster our long-term economic and energy security.

What is Clean Hydrogen?

Hydrogen is one of the most common elements on Earth, but it is rarely found on its own. It is most often bonded to other elements in molecules such as water or methane (natural gas). To obtain pure hydrogen gas, it usually must be separated from other molecules, which can be done through several methods.

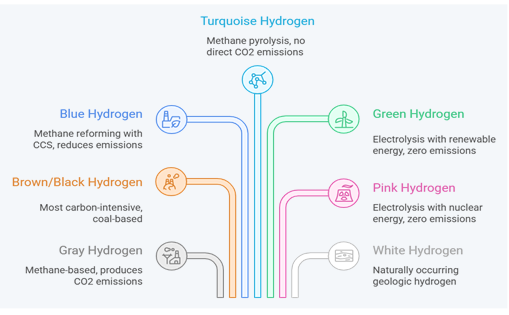

Currently, most hydrogen is derived from fossil fuels—primarily natural gas—through a process known as steam methane reforming (SMR), which releases carbon dioxide (CO2) as a byproduct. Clean hydrogen refers to hydrogen produced with lower lifecycle greenhouse gas emissions than traditional methods. This can be done either by pairing fossil-based technologies with carbon capture, or through electrolysis, which uses electricity to split water into hydrogen and oxygen. While hydrogen gas is colorless, policymakers and industry stakeholders often refer to hydrogen “colors” as a shorthand for different production methods and energy sources (Figure 1).

Figure 1. The “colors” of hydrogen (author’s illustration, created with online visualization tool).

In the United States, around 95% of hydrogen is produced via SMR (“gray” hydrogen). Globally, the share is about 62%. Approximately 21% of global hydrogen production is coal-based—with the majority of this located in China and India. Global clean hydrogen output grew by around 10% in 2024, although it still accounts for less than 1% of total production.

As with all emerging technologies, production at scale with low-carbon hydrogen production methods has not yet been achieved, which makes them more costly than traditional pathways. Many stakeholders are racing ahead to change that, however. As production scales and technologies mature, costs are expected to fall significantly, accelerating adoption.

Fueling Growth and Global Leadership

An Engine for Job Creation and Economic Growth

A robust clean hydrogen sector can stimulate economic growth and job creation, revitalize domestic industrial corridors and reassert American leadership in clean energy technologies across the globe.

Federal policy support plays a critical role in unlocking this economic potential. The Energy Futures Initiative (EFI) estimated that policies such as the bipartisan 45V clean hydrogen production tax credit and the Department of Energy (DOE) Regional Clean Hydrogen Hubs program could generate a seven-to-one return on investment in cumulative gross domestic product (GDP).

This potential is already materializing. Since the launch of the Hydrogen Hubs program in November 2021, companies have announced more than $37 billion in planned investments in clean hydrogen production and electrolyzer manufacturing.

Blue hydrogen projects alone could stimulate billions in economic output and create tens of thousands of jobs. A recent report by CRES Forum finds that by 2030 (and once operational), blue hydrogen projects currently under development could annually generate over $22.4 billion in economic output, $12.3 billion in GDP, as well as support over 62,200 jobs—many of these well-paid positions that utilize skills similar to those needed in traditional energy sectors such as oil and gas.

The United States has a distinct comparative advantage for blue hydrogen production, with abundant reserves of low-cost natural gas, unmatched capacity for geological CO2 storage, as well as extensive experience in industrial methane-based hydrogen production. Projects in several Hydrogen Hubs, such as the Appalachian Clean Hydrogen Hub (ARCH2) in West Virginia, Ohio, and Pennsylvania and the HyVelocity Hub in Texas and Louisiana, will produce blue and turquoise hydrogen, which will allow these regions to continue to sustainably leverage their abundant natural gas resources and boost regional economic growth for decades to come.

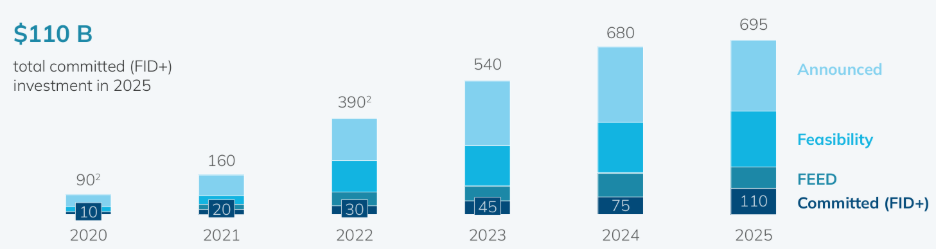

Globally, according to the Hydrogen Council, committed investments have grown around 50% annually since 2020, from $10 billion that year to $110 billion in 2025—an eleven-fold increase. When considering investment announcements across all project stages, the growth magnitude is even greater, rising from $90 billion in 2020 to $695 billion in 2025—a surge of over 670% (Figure 2).

Figure 2. Investment pipeline in clean hydrogen projects by 2030, billion USD. Source: Hydrogen Council and McKinsey & Company, Global Hydrogen Compass 2025, September 2025, p. 8.

The Global Hydrogen Landscape: Competition and Opportunity

As other countries race to develop their clean hydrogen sectors and supply chains, the emerging global market for hydrogen creates both opportunities and competition for U.S. producers. Additionally, rising international demand for hydrogen-associated low-carbon goods such as clean steel or fuels further highlights how supporting the rapid scale-up of a clean hydrogen sector can unlock new market opportunities while bolstering energy security by diversifying our energy resources. Early, proactive investment can help ensure the U.S. captures global market share and become a preferred long-term supplier.

Europe: The European Union (EU) bloc set ambitious targets for importing 10 million metric tons (MMT)—and producing another 10 MMT—of green hydrogen by 2030 under the REPowerEU strategy, which represents a lucrative potential export market for U.S. producers. Germany has outlined a particularly ambitious clean hydrogen strategy, and expects its demand to reach 1.36 to 2.73 MMT by 2030, with 50 to 70% of that to be met by imports. According to the Hydrogen Council, the EU is expected to account for 65% of global clean hydrogen demand by 2030.

Asia:

- Japan and South Korea are also promising export markets. Both nations are ramping up efforts to leverage hydrogen to decarbonize their industrial, power and transportation sectors. They are also both advancing the development of their own hydrogen hubs. Japan’s ambitious Hydrogen Strategy, which aims for 12 million tons of hydrogen and ammonia use per year, will rely primarily on imports, given the country’s limited domestic energy resources. The Hydrogen Council estimates East Asia will account for around 25% of clean hydrogen demand by 2030.

- China is aggressively expanding its electrolyzer and hydrogen fuel cell vehicle manufacturing capacity, as well as its hydrogen charging infrastructure, backed by heavy state subsidies. The country already controls around for 65% of global electrolytic production capacity, and nearly 60% of electrolyzer manufacturing capacity, followed by Europe and the United States. Hydrogen will also be featured prominently in China’s next Five-Year Plan (2026-2030). New policies are expected to better align the supply and demand of green hydrogen, green methanol, green ammonia and sustainable aviation fuel (SAF), leveraging the country’s soaring wind and solar electricity generation.

Middle East: Nations such as Saudi Arabia, Egypt, Oman and the UAE are developing a combined production capacity of clean hydrogen and ammonia of 9 MMT/year. They plan to leverage their abundant solar, wind and natural gas resources to become major exporters.

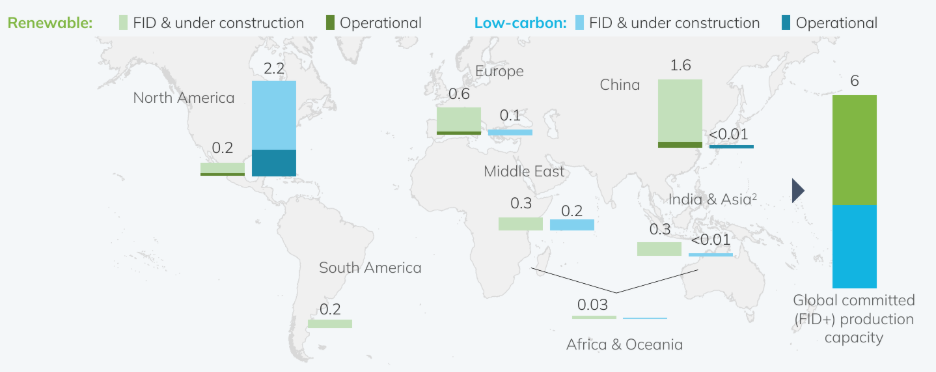

While North America currently accounts for the majority of clean hydrogen projects that are operational and under development, China vastly outpaces all other regions in renewable hydrogen capacity (Figure 3).

Figure 3. Renewable and low-carbon hydrogen production capacity by region, operational and at FID/under construction (in million tons per annum, mtpa). Source: Hydrogen Council and McKinsey & Company, Global Hydrogen Compass 2025, September 2025, p. 13.

Clean Hydrogen’s Potential in Hard-To-Abate Sectors

Clean hydrogen offers a powerful tool to reduce lifecycle emissions in sectors where hydrogen is already essential, such as oil refining or ammonia and fertilizer manufacturing. It also holds significant promise as a low-carbon alternative fuel or feedstock in emerging applications such as transportation and steel manufacturing. As other countries move to integrate clean hydrogen into their industrial supply chains, the race is on to dominate export markets in both traditional and new end-use sectors.

Refining, Fuels and Transportation

Hydrogen is essential for oil refining and shows growing potential as a clean-burning fuel. By integrating low-carbon hydrogen, the U.S. can cut emissions from today’s fuels while broadening the mix to include next-generation low-carbon alternatives. Other nations are moving forward:

- Europe: Policies like the EU Alternative Fuels Infrastructure Regulation (AFIR), ReFuelEU Aviation, and the UK SAF Mandate are creating premium markets for low-carbon hydrogen and jet fuel.

- Asia: Japan and Singapore have proposed or established Sustainable Aviation Fuel (SAF) requirements, while China and South Korea are advancing aggressive plans for hydrogen fuel cell vehicle (HFCV) development. Today, South Korea is leading in HFCV deployment.

- North America: Canada is seeking to become a leading producer and consumer of clean fuels like hydrogen and biofuels, and its Clean Fuel Regulations are driving demand for low-carbon refinery inputs and processes.

Oil Refining

Refining is the largest domestic consumer of hydrogen, primarily for hydrocracking (breaking heavy hydrocarbons into lighter, more valuable products such as gasoline, diesel, and jet fuel) and hydrodesulfurization (removing sulfur to meet quality and environmental standards for these fuels). Most of this hydrogen is currently produced on-site via SMR without carbon capture. Refining accounts for 68% of domestic hydrogen demand and 42.5% globally.

Replacing this gray hydrogen with lower-carbon alternatives presents one of the most immediate and cost-effective industrial decarbonization opportunities. Many refineries already produce and manage large hydrogen volumes on-site via SMR, so switching to low-emissions hydrogen would require relatively limited retrofitting—primarily the addition of carbon capture systems to existing SMRs.

Blue hydrogen is particularly well-positioned to supply near-term refinery demand, as demonstrated by the Air Products–Valero system in Port Arthur, Texas, which has supplied low-carbon hydrogen to the refinery since 2013 while capturing around 1 million tons of CO₂ annually.

Integrating low-carbon hydrogen into refining processes would also strengthen U.S. competitiveness in global fuel markets. As Europe and other regions adopt stricter lifecycle emissions standards for gasoline, diesel and jet fuel, U.S. refiners able to demonstrate lower emissions will be better positioned to protect and expand exports—especially along the Gulf Coast, already a global hub for refined product exports and home to several large-scale blue hydrogen projects.

Transportation and Clean Fuels

Beyond refining, clean hydrogen and derived fuels such as ammonia and methanol are well-suited for deployment as an alternative fuel across multiple transportation modes—from heavy-duty trucking to maritime shipping, aviation and material handling equipment. They enable low-emission operations while meeting the performance demands of both long-distance and intensive, on-site applications. Clean hydrogen offers a pathway not only to cut emissions, but also to enhance resilience by diversifying our fuel mix.

Aviation and International Maritime Shipping: among the most promising applications, as few alternatives can satisfy the high energy demands of long-distance transport.

- Maritime Transport and Shipping. Clean hydrogen and derived fuels like ammonia or methanol are emerging as promising alternatives to heavy fuel oil or diesel in shipping and harbor craft. The use of clean ammonia or methanol in maritime shipping could reduce CO2 emissions by between 60% and 95% compared to conventional fuels, depending on the lifecycle emissions of the hydrogen used. Demonstration projects are underway in coastal ports and on inland waterways in the U.S. and abroad, including hydrogen-powered tugboats, towboats, ferries and ammonia- or methanol-fueled cargo vessels.

- Aviation. Sustainable aviation fuels (SAFs) produced via hydrogen-based processes, such as synthetic kerosene, offer a near drop-in solution to lower emissions from commercial aviation. DOE estimates that SAF could reduce lifecycle greenhouse gas emissions by up to 94% compared to conventional jet fuel, depending on the feedstock and production pathway. While costs and feedstock availability remain challenges, early commercial use has begun through demonstration flights and low-percentage blends on select routes.

Hydrogen may also power short-haul or regional aircraft directly via fuel cells, producing mainly water vapor when consumed. Although currently limited to demonstration projects, some major airlines and aviation companies are investing in technology partnerships, prototype testing and conditional purchase agreements with the aim of launching hydrogen-powered aircraft within the next five years.

Long-Haul Trucking: This segment of road transportation is where hydrogen shows the greatest potential for decarbonization, whereas other technologies have become more established in passenger vehicles.

Hydrogen fuel cell vehicles (HFCVs) offer fast refueling, high energy efficiency, long range and strong payload capacity, making them well-suited for freight corridors and regional distribution networks. According to DOE, heavy-duty hydrogen vehicles can refuel in 10-15 minutes, with some prototypes achieving a range of over 600 miles.

DOE estimates that the lifecycle emissions of hydrogen-fueled trucks can be 20 to 80% lower than that of conventional internal combustion engines, depending on the hydrogen production pathway. Adoption faces some challenges, including limited public refueling infrastructure, high vehicle costs and a small number of available models, but some major companies are already testing out long-haul hydrogen trucks.

Material Handling Equipment: Hydrogen fuel cells are also a strong fit for industrial machinery such as forklifts, reach stackers or yard trucks, which operate in high-utilization, on-site environments, as well as drayage trucks that run continuous short-haul routes between ports, rail yards and warehouses. They can refuel in minutes, provide reliable power over long shifts and use localized fueling stations. Beyond operational efficiency, employing hydrogen-fueled machinery can significantly reduce local air pollution, making it particularly valuable in indoor or localized working environments such as warehouses and ports.

Fuel cell forklifts, in particular, are already deployed at scale in the United States, proving that hydrogen-powered vehicles can be a commercially viable solution for industrial fleets. Around 70,000 forklifts are already in operation at warehouses, manufacturing plants and distribution centers across the country. Hydrogen-powered drayage trucks, which run continuous short-haul routes between ports, rail yards and warehouses, are also a strong fit for warehouse and port-adjacent environments, with small-scale and pilot projects in development.

Steelmaking

Clean hydrogen could play a critical role in supporting the decarbonization of most steel production pathways. Globally, the majority of emissions in the sector stem from the reliance of most countries on traditional coal-based blast furnaces. These emissions are hard to abate due to the high temperatures and chemical reactions involved. China and India, the world’s top two steel producers, remain heavily reliant on this method.

In the U.S., most steel—over 70%—is made in electric arc furnaces (EAFs), which recycle scrap steel using electricity. EAFs are significantly less carbon-intensive than blast furnaces but are not emissions-free. In EAF steelmaking, Direct Reduced Iron (DRI)—produced by using natural gas (or, in some regions, coal) as a reducing agent to remove oxygen from iron ore—is often blended into EAF feedstock to improve steel quality. Rising demand for high-quality steel and limited scrap availability mean more primary iron production will still be needed, with global steel demand expected to grow 32% by 2050.

Hydrogen can be a decarbonizing asset for both production methods, either as a source of high-temperature heat, or as an alternate reducing agent:

- In traditional blast furnaces, which rely on coal and coke as both a fuel and reducing agent, hydrogen can partially substitute coal. This can significantly reduce process emissions, with one Nippon Steel pilot project reporting a 42% reduction in CO2 emissions through hydrogen use.

- In EAF-based steelmaking paired with Direct Reduced Iron, hydrogen can be used as an alternate reducing agent in the DRI process. According to DOE, this could reduce process emissions by 40 to 70%. Hydrogen use in this pathway is considered one of the most promising approaches for emissions reduction in steelmaking. While near-term uptake is constrained by cost, scaling up clean hydrogen production would lower costs and help drive broader adoption.

Leveraging hydrogen in steel production can help the U.S. meet growing global demand for clean construction materials and vehicle components while reinforcing domestic competitiveness and leadership in clean manufacturing. A global market for low-carbon steel is beginning to emerge—and if America does not act quickly, competitors will seize the opportunity.

- Europe: Regulatory changes such as the EU’s CBAM and rising demand from the automotive, offshore wind, and construction sectors are fostering a premium market for low-carbon steel. Some projects have been delayed by high electricity costs—nearly double those in the U.S.—and by competition from cheaper, higher-emission imports from China. Yet major European steel manufacturers remain committed to long-term decarbonization, and as policy and demand signals strengthen, Europe could become a lucrative export market for North American low-carbon steel.

- East Asia: Japan is also making major investments in clean steel manufacturing. In May 2025, Nippon Steel committed around $5.7 billion, supported by $1.65 billion in government funds, to deploy clean hydrogen in both blast furnaces and in the production of DRI for use in EAFs.

- Latin America: Brazil is positioning itself as an early mover, with plans to export clean hydrogen to steelmakers in Europe. In January 2025, Brazil announced the selection of 12 hydrogen hubs to support the decarbonization of its industry.

Ammonia and Fertilizers

Fertilizer manufacturing is one of the largest existing uses of hydrogen worldwide. About 21% of domestic hydrogen production is used to make ammonia, the key ingredient in most fertilizers. And 88% of that ammonia is destined for fertilizer production. Globally, roughly 36% of hydrogen production is used to make ammonia and fertilizer production accounts for nearly 70% of ammonia demand.

Ammonia and fertilizer production are emissions-intensive. China leads global ammonia output, accounting for 31% of production—with 85% of this relying on coal—followed by India (10%), the United States and Russia (9% each).

Using low-carbon hydrogen in ammonia production represents one of the fastest and most scalable ways to reduce emissions in agriculture. According to DOE, using clean hydrogen for ammonia and methanol manufacturing could cut their lifecycle emissions by over 90%. It also creates opportunities for cleaner fertilizer exports, as other regions consider the ammonia and fertilizer industry in their decarbonization strategies. The EU’s CBAM, for example, is tightening carbon accounting for fertilizer imports, creating a premium market for producers that can demonstrate lower lifecycle emissions.

Today, clean ammonia is the largest target end use for announced U.S. clean hydrogen production projects. Some US companies have already begun production of low-carbon ammonia, such as the CF Industries facility in Donaldsonville, Louisiana, which has been retrofitted with carbon capture technology and began producing “blue ammonia” in July 2025. The company is also planning the construction of a second large-scale blue ammonia plant at the complex.

Methanol, Plastics, and Resins

Around 11% of domestic hydrogen is used to produce chemicals such as methanol. Globally, methanol accounts for around 16% of total hydrogen demand. In addition to its potential as a marine fuel, it is a fundamental intermediary building block for a wide range of plastics (polyethylene, polypropylene, PVC) and formaldehyde-based resins that are important for the manufacturing of products like particleboard, coatings, paints and adhesives. The use of low-carbon methanol would reduce the lifecycle emissions across these products.

Policy Recommendations

As with any emerging technology, business certainty breeds faster deployment. Stable, predictable incentives and clear regulatory signals help provide investors and developers with the confidence needed to move forward with large-scale clean hydrogen projects.

1. Section 45V Clean Hydrogen Production Tax Credit

The 45V tax credit is the United States’ premier incentive for clean hydrogen deployment. It provides a tiered production-based incentive tied to lifecycle emissions, with the highest credit level awarded to production with the lowest emissions. It will help reduce capital costs for first-of-a-kind projects and accelerate initial deployment.

The scale of private investment announced since the establishment of both the Hubs program and the 45V credit underscores how quickly deployment can accelerate when strong incentives are in place. The decision to keep the 45V tax credit in place through 2027 was a result of key Republican Congressional support. Through preservation of this incentive, Congress is providing vital policy stability needed to scale this emerging energy sector. Continued focus on speedy and efficient implementation will be key to accelerating deployment in this strategic sector.

2. Leverage DOE’s Hydrogen Hubs to Scale the Hydrogen Economy

DOE’s Regional Clean Hydrogen Hubs program is central to building a robust domestic hydrogen economy. By pooling risk and resources, the hubs aim to enable economies of scale that would be difficult for individual investors or developers to achieve on their own. Additionally, the deliberate focus on geographic and technological diversity ensures the U.S. avoids reliance on any single production pathway, strengthening resilience and energy independence. Industrial clusters have already started forming in each hydrogen hub location, which leverage the unique advantages of each region’s energy mix.

Hubs also strengthen U.S. international competitiveness, especially as other regions and countries advance similar hub strategies—including the EU, Japan, Brazil and Australia. Continued federal support for hydrogen hubs at this stage is vital to achieve scale-up and ensure we remain competitive vis-a-vis global competitors such as China and the EU.

3. Continued Federal Support Across R&D, Demonstration and Commercialization

Sustained federal engagement across the innovation chain—from early-stage R&D to first-of-a-kind demonstrations and commercial deployment—plays a critical role in building a competitive hydrogen economy. Continued support and funding for DOE programs that advance clean hydrogen technologies will be key to accelerating deployment and securing America’s technological edge in this emerging sector.

4. Streamline Permitting for Associated Infrastructure

Comprehensive permitting reform can create predictable, efficient processes that will accelerate the buildout of new energy assets—including those associated with clean hydrogen. Under the current permitting structure, supportive infrastructure such as hydrogen and CO2 pipelines face ambiguous or patchwork governance regimes—with no single federal agency having clear siting authority—that are often scattered across different agencies and that can vary significantly from state to state.

5. Position the United States as a Global Supplier of Choice

The opportunity is ripe for coordination between policymakers and U.S. businesses to position the United States to compete effectively as a leading supplier of clean hydrogen and hydrogen-derived products in international markets. Through supportive policies such as the 45V tax credit and the Clean Hydrogen Hubs program, policymakers can facilitate the scale-up of the domestic clean hydrogen sector that, combined with effective trade relationships, will enable US producers to successfully compete in the global market and reinforce America’s role as a dominant energy supplier.

Conclusion

Clean hydrogen is a strategic lever for American economic growth, industrial revitalization and global competitiveness. With the right mix of policy, private investment and innovation, America can secure leadership in this emerging market, protect and expand export advantages and open new opportunities for American technologies and jobs.